You are probably dealing with one of two situations right now.

Either your condo association has a reserve account that feels vaguely inadequate, and no one can tell you with confidence whether it is enough. Or you already know it is not enough, but the board has been avoiding the conversation because nobody wants to be the person who recommends higher dues.

That delay is how communities end up cornered. The roof fails, the elevator needs a major overhaul, balconies need structural work, pavement deteriorates, and the board suddenly has to explain why the association was technically “compliant” yet still unprepared.

Why Your Condo's Financial Health Is at Risk

A reserve crisis rarely starts with one bad decision. It starts with years of smaller ones. Keep dues low. Skip the study update. Push off a contribution increase. Treat the lender minimum as if it were a sound funding strategy.

That last mistake is the most dangerous one.

Lenders such as FHA and Fannie Mae require only 10% of the annual operating budget in reserves, but a 2021 study found that 99.85% of condo associations need more than that to properly fund future replacements (hoa reserve funding article from ReserveStudy.com). If your board is treating the 10% rule as the target, not the bare minimum, you are setting up owners for future special assessments.

Compliance is not the same as financial health

A lender minimum exists to screen for basic loan eligibility. It does not tell you what your building needs.

Your roof does not care what a lender accepts. Your plumbing stack does not care what looks acceptable on a resale questionnaire. Your concrete, balconies, siding, elevators, and drainage systems age on their own schedule.

Boards that anchor their budgeting to the lender floor usually create three problems:

- They underfund predictable repairs: Major components wear out whether the association saved for them or not.

- They trigger owner backlash later: Owners are far more upset by sudden special assessments than by a steady, well-explained reserve plan.

- They put property values at risk: Buyers, lenders, and inspectors all react poorly when a community looks financially fragile.

Board president takeaway: If your community is proud of meeting the 10% lender minimum, you may still be nowhere near a healthy reserve position.

The core job of a condo board

Your job is not to produce the lowest monthly dues. Your job is to protect the building and the people who live in it.

For Georgia condo boards, that means treating reserve planning as an ownership protection issue, not an accounting exercise. Owners bought into a shared property. The board’s responsibility is to keep that property physically sound and financially stable.

A weak reserve fund makes every future repair more expensive politically and financially. A strong reserve fund gives the board options, credibility, and time.

If you want to avoid the ugly cycle of deferred maintenance, emergency meetings, homeowner anger, and lender trouble, stop asking whether your reserve contribution clears the minimum. Ask whether it matches the property you have to maintain.

Understanding Your Association's Reserve Fund

Most new board presidents need one simple mental model.

Your operating account is your community’s checking account. Your reserve fund is its long-term savings account.

If you mix those up, the budget gets distorted fast.

What reserves are for

Reserve money exists for major repair and replacement of common elements. Think long-life, high-cost items that the association knows will need work over time.

Typical reserve-funded items include:

- Roof systems: Replacement is predictable even if the exact date is not.

- Elevators and mechanical systems: These components age, require major modernization, and can become safety concerns.

- Paving and concrete surfaces: Parking areas, sidewalks, and structural slabs do not last forever.

- Building envelope items: Balconies, siding, waterproofing, windows in some communities, and other exterior systems often belong in the reserve plan.

- Plumbing or infrastructure components: Depending on governing documents and common element responsibilities, major system replacements may belong here.

Reserve spending should follow the long-term capital plan for the property. It is not a slush fund for whatever the board wants to handle this month.

What reserves are not for

Operating money covers recurring, routine expenses.

That usually means things like:

- Landscaping and grounds care

- Utilities for common areas

- Cleaning and janitorial work

- Management fees

- Routine maintenance and service contracts

- Insurance and administrative costs

If your association repeatedly uses reserve money to patch operating shortfalls, the board is not solving a budget problem. It is hiding one.

What healthy funding looks like

Healthy condo associations often allocate a significant portion of total assessments to reserves. For an average monthly assessment, this could amount to a substantial per-unit contribution each month. A reserve fund is generally considered healthy when it is 70% to 100% funded based on a professional reserve study (Associa’s overview of condo reserve funding benchmarks).

Those figures are not a universal budget template. A high-rise with elevators, pools, balconies, and parking structures will not look like a simple garden-style community. The point is broader and more important. Healthy communities commit real money to reserves. They do not fund them with leftovers.

Why owners should care

Homeowners sometimes hear “reserve contribution” and think “money sitting idle.”

That is the wrong frame.

A reserve fund does three jobs for owners:

- It spreads major repair costs over time instead of dropping them on whoever owns at the moment of failure.

- It protects the physical condition of the property.

- It supports lender confidence and marketability.

Practical rule: Boards should explain reserve contributions as planned ownership costs, not optional savings.

When a board underfunds reserves to keep dues artificially low, it is not saving owners money. It is shifting costs into the future and concentrating them into a painful event.

A well-run reserve fund is one of the clearest signs that a board understands its duty. It shows the community is thinking beyond this month’s bill cycle and planning for the full life of the property.

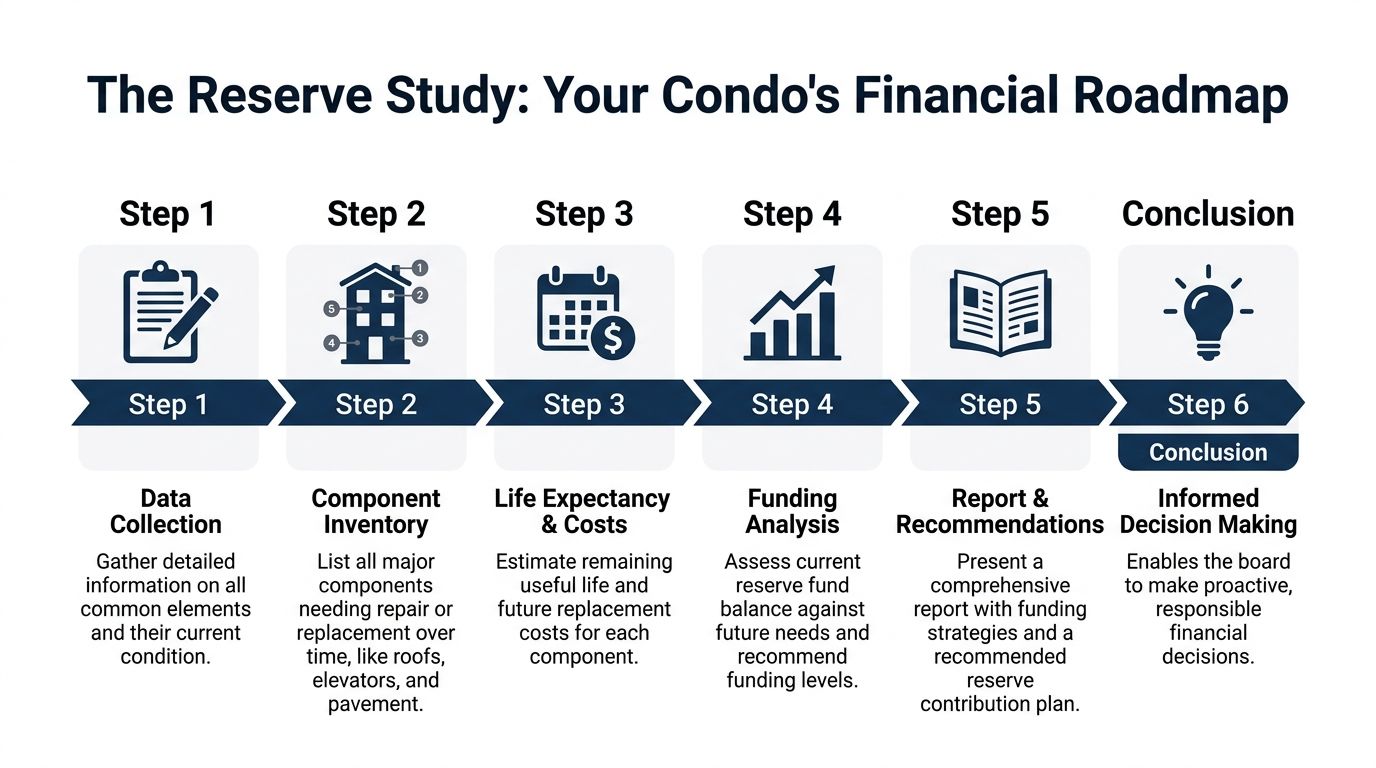

The Reserve Study Your Financial Roadmap

A new board president usually sees the problem too late. The roof bid lands on the agenda, the pavement is failing, owners are already angry about dues, and the reserve balance is nowhere near what the community needs.

That is what a reserve study prevents.

A reserve study gives the board a documented plan for major repair and replacement costs. It replaces opinion with an inventory, timing, and a funding schedule tied to the property itself. For Georgia associations, that matters because lender minimums are not a financial strategy. A community can satisfy a basic lending threshold and still be on a direct path to underfunding, deferred repairs, and a condominium special assessment.

The physical side of the study

The first job is physical analysis.

That means identifying the common elements the association must maintain, evaluating their condition, estimating remaining useful life, and flagging which components belong in reserves. California DRE reserve study guidance describes this as a detailed inventory that can cover a long list of common-area components, not just obvious items like roofs.

A competent physical analysis answers a few direct questions:

- What common elements does the association own and maintain?

- What condition is each component in right now?

- How much useful life is realistically left?

- Which items are close enough to failure that the board needs to plan now?

- Which costs are large enough that operating cash should never be carrying them?

Boards get into trouble when they rely on memory, contractor chatter, or last year's repair list. That is not planning. It is guessing with owner money.

If the study skips components, the funding plan will come up short. Every time.

The financial side of the study

The second job is financial analysis.

Here, the study turns the component list into a long-range funding plan. It projects future repair and replacement costs, tests whether current reserve contributions are adequate, and shows the board what happens if it keeps dues artificially low.

Many boards make the wrong comparison at this point. They ask whether they meet a lender minimum. They should ask whether the reserve account is healthy enough to carry the association through predictable capital expenses without panic. Ten percent may clear a basic lending screen. It does not put a condominium in a strong position. Healthy funding is much higher, and the reserve study shows how far the association is from that mark.

A useful financial analysis should show:

- Current reserve balance

- Projected major repair and replacement costs

- Recommended annual reserve contributions

- Cash flow over time

- Funding options and the tradeoffs behind each one

That is the board's roadmap. It connects the condition of the property to the budget owners have to support.

Update the study before conditions force your hand

A reserve study is not a one-time project.

Costs change. Components fail early. Projects get delayed. Inflation rewrites old assumptions fast. A study that looked reasonable a few years ago can become misleading if the board never updates it and never compares the report to actual site conditions.

Boards should review the study regularly and order formal updates on a disciplined cycle. That is how you catch a shortening roof life, rising concrete costs, or a mechanical system that is aging faster than expected. Waiting until the annual budget meeting is too late.

What boards miss when they treat the study like a file, not a tool

An outdated reserve study creates false confidence. The balance may look acceptable on paper while the actual funding gap keeps widening.

That gap is the danger. A board that aims for bare-minimum compliance can still be badly underprepared for the property's actual expense curve. Then the community gets hit twice. First with deferred maintenance. Then with sudden owner charges when the work can no longer wait.

The reserve study does not create those costs. It exposes them early enough for the board to spread them fairly and manage them responsibly.

What a board president should demand

Use the study actively. Do not let it sit in a board packet until the next crisis.

Ask these questions:

- Which components create the largest reserve pressure over the next few years?

- Which assumptions in the study need to be tested against current contractor pricing?

- Are reserve contributions based on actual replacement needs or political pressure to keep dues low?

- How far is the association from a healthy funding level?

- What projects could trigger a special assessment if the board stays on the current path?

A good reserve study should make decisions clearer. If it is stale, vague, or disconnected from what you see on the property, fix that immediately. Boards protect property values by funding reality, not by chasing the lowest number owners will tolerate.

Navigating Legal and Lender Requirements in Georgia

A new board president in Georgia often hears some version of this: “We meet the lender test, so reserves are fine.” That thinking gets associations into trouble.

Meeting a lender minimum is not the same as being financially healthy. It is a basic screening threshold. Your building still has roofs, pavement, elevators, siding, and drainage systems that wear out on schedule, not on the lender's schedule.

What Georgia boards have to handle

Georgia law does not hand boards a clean reserve percentage and call it done. That does not reduce your responsibility. It increases it.

Your job is to maintain the common elements, budget with integrity, and avoid preventable financial shocks to the membership. A board that keeps dues artificially low while major components age is making a choice. The likely result is deferred work, declining property condition, and a sudden bill to owners later.

This is the key Georgia issue. The absence of a statutory percentage does not protect the board from bad planning.

The dangerous gap boards miss

The biggest mistake I see is treating the lender minimum as a target.

For many condominium loan programs, a common benchmark is setting aside at least 10% of the annual budget for reserves. Boards love that number because it looks official and feels manageable. In practice, it can be badly disconnected from the property's actual replacement needs.

A community can satisfy that 10% test and still sit far below a healthy funding position. If your association is nowhere near the 70% or higher range for reserve adequacy, you are still exposed. That gap is where special assessments are born.

Owners do not care that the budget checked a financing box if they get hit with a five-figure project bill. They care that the board saw predictable deterioration coming and failed to fund for it. If your current path points toward a condominium special assessment for major repairs, the reserve plan is too weak.

What lender standards really mean for your association

Lender standards matter because they affect buyer financing, sales velocity, and marketability. They do not tell you whether reserves match the property.

Use them as one constraint, not the standard that drives the budget. A board focused on long-term stability should ask a harder question: are contributions based on actual component costs and timing, or just on the lowest number that keeps financing available?

That answer affects more than accounting. It affects owner confidence and resale value.

A practical standard for Georgia associations

If you lead a Georgia condo board, use this checklist:

- Read the governing documents closely: Confirm who maintains each common element and whether reserve funding is addressed directly.

- Budget from the reserve study, not from habit: Annual contributions should reflect the property’s repair and replacement schedule.

- Treat 10% as a floor: If the study supports higher contributions, fund higher contributions.

- Aim for healthy funding, not technical compliance: Boards should work toward a reserve position that reduces the chance of owner shock.

- Record the board’s reasoning in the minutes: Good documentation shows that decisions were informed and responsible.

- Explain the funding plan to owners early: Owners accept increases more readily when the board ties them to real projects and real timelines.

Georgia boards do not need a statute to tell them what prudent looks like. Fund the property based on what it will cost to maintain it, not on the lowest standard a lender will tolerate.

How to Calculate Your Association's Funding Needs

Board members do not need to become reserve specialists. They do need to read a funding report without getting lost in jargon.

The most useful number in the entire discussion is Percent Funded.

Start with Percent Funded

Percent Funded is calculated as Current Reserve Balance ÷ Fully Funded Balance (Rimkus explanation of percent funded and reserve benchmarks).

That ratio tells you how your current reserve position compares to what should have been accumulated for the components you are responsible for maintaining.

The same reserve benchmark guidance classifies the result this way:

| Percent Funded range | What it means |

|---|---|

| 0% to 30% | Weak. High risk of special assessments. |

| 30% to 70% | Fair. Better than crisis mode, but not strong. |

| 70% to 100% | Strong. This is the healthier range for reserve adequacy. |

That is the number I want every board president to know before approving a budget.

If your association sits in the weak range, you are not making a conservative financial choice. You are running a higher-risk operation.

Quick guidance: Ask your manager and reserve professional to show Percent Funded in plain language, not buried deep in the report.

What Fully Funded Balance means

The Fully Funded Balance is the amount the association should have set aside, based on the deterioration and aging of major common elements. It is not a random target. It is the reserve benchmark tied to the life cycle of the actual property.

That matters because many boards focus only on the cash they have, not the obligations that cash is supposed to cover.

A reserve account can look large in isolation and still be inadequate. The right question is always relative. Adequate compared to what future repair burden?

Comparison of Reserve Funding Models

Most boards will encounter two broad funding approaches when reviewing a reserve study.

| Funding Model | Goal | Pros | Cons |

|---|---|---|---|

| Full funding | Build reserves toward the fully funded balance over time | Stronger financial position, clearer alignment with component deterioration, more protection against surprises | Higher contribution demands can be politically difficult |

| Threshold funding | Keep reserves above a chosen minimum threshold rather than fully funding every component | More flexibility in contribution planning, can reduce short-term pressure on assessments | Less margin for error, more sensitive to cost increases, delays, and unexpected repairs |

Neither approach excuses wishful thinking. If your board adopts threshold funding, it still needs a realistic margin and disciplined follow-through.

How to use the numbers in practice

When reviewing the study, your board should ask:

- Where are we now on Percent Funded?

- What contribution level moves us toward a healthier position?

- Which upcoming projects create the most pressure on cash?

- Are we choosing a funding model because it fits the property, or because it feels easier politically?

This is also where your systems matter. If your accounting is messy, reserve decisions become harder than they should be. Boards that use better reporting tools and cleaner financial workflows can monitor reserve performance with less confusion. If you are reviewing software options, this guide to best HOA accounting software is a useful place to start.

What I recommend

For most condo boards, the strongest position is clear. Know your Percent Funded, aim for the strong range, and stop defending contribution levels that only look acceptable because the board has not compared them to the fully funded balance.

The numbers are not there to make the board uncomfortable. They are there to keep the community out of trouble.

Reserve Fund Governance and Common Pitfalls to Avoid

A reserve plan can be technically sound and still fail because of poor governance.

Boards get into trouble when they know what should happen but lack the discipline to do it. Reserve management is not just about spreadsheets. It is about judgment, policy, and the board’s willingness to say no when short-term pressure collides with long-term responsibility.

What good governance looks like

Strong boards protect reserves through process, not personality.

That usually means a few practical habits:

- Keep reserves segregated: Reserve funds should stay separate from operating cash so the board can track them clearly and avoid casual misuse.

- Review reserve performance regularly: Do not wait for annual budget season to ask whether contributions and project timing still make sense.

- Tie decisions to the study and the budget: If the board departs from the reserve plan, the reasons should be documented.

- Invest conservatively: Reserve money should be protected, liquid enough for planned projects, and governed by a written policy.

- Communicate in plain English: Owners deserve to understand what is being funded and why.

The board’s authority carries an obligation to use structure, not instinct. If roles and responsibilities need clarification, this overview of HOA board responsibilities is a practical reference.

The mistakes that keep repeating

Most reserve failures come from a short list of board behaviors.

Keeping dues low for applause

This is the classic error.

A board freezes or trims contributions because owners are sensitive to monthly costs. That may win a quiet budget meeting. It also increases the chance that owners will face a much worse financial hit later.

Low dues are not evidence of strong leadership if they are built on weak reserves.

Borrowing from reserves to fix operations

If the operating budget is short, fix the operating budget.

Using reserves to cover recurring expenses is one of the fastest ways to destroy the integrity of the funding plan. It also confuses owners about what reserve money is supposed to do.

Treating reserve projects as optional

Boards sometimes delay known capital work because the component has not completely failed yet.

That can be reasonable in limited cases. It becomes reckless when delays are driven by denial instead of condition data. Deferring a project without revising the plan is not strategy. It is wishful budgeting.

Hiding the problem from owners

Some boards avoid transparent reserve conversations because they fear backlash.

That is backwards. Owners become angrier when they discover the board knew there was a problem and chose silence. Transparent boards earn more credibility even when the message is unwelcome.

Leadership rule: Owners can handle difficult news better than they can handle surprise bills.

Do this instead

Reserve governance improves when the board adopts a few standing practices.

- Build reserve review into the annual calendar. Make it a routine agenda item, not an emergency topic.

- Document major capital assumptions. If the board changes timing or scope, capture the reason in the minutes.

- Use professional input. Managers, accountants, engineers, and reserve specialists all have a role. Use them.

- Train incoming board members. A new director should understand the reserve philosophy before voting on the budget.

- Explain the owner benefit. Owners support reserve funding more readily when they see the direct connection to building condition and resale stability.

Reserve funds fail when boards treat them as abstract. They succeed when boards defend them as one of the community’s core assets.

Answers to Your Board's Toughest Reserve Fund Questions

We are already underfunded. What should we do first

Get current information and stop pretending the old numbers are good enough.

Order or update the reserve study, identify the most urgent capital obligations, and build a phased recovery plan into the budget. Do not promise owners that the board can fix years of underfunding painlessly. It usually cannot.

Your first job is clarity. Your second job is a credible timetable.

How do we tell owners dues need to increase

Lead with facts about the property, not abstract finance.

Explain which common elements the association must maintain, what the reserve study shows, and why the current funding level is not enough. Tie the message to fairness. Regular contributions spread costs across time and ownership. Surprise assessments punish whoever happens to own at the wrong moment.

Keep the tone calm and direct. Owners do not need spin. They need an honest explanation and a plan.

Can we just rely on special assessments when big projects happen

You can. It is a poor way to run a condominium.

Special assessments create stress, owner conflict, collection problems, and resale complications. They also signal that the board failed to match known long-term obligations with a long-term funding strategy.

An occasional assessment for a true surprise is one thing. Building your financial model around future special assessments is something else entirely.

What if owners push back hard

Expect pushback. Then stay disciplined.

Some owners will always prefer lower dues today, even when that choice creates larger costs later. The board still has to govern for the whole community. That means making decisions that protect the building and reduce avoidable financial shocks.

Use owner meetings, budget notes, and plain-language summaries of the reserve plan. Repeat the same core message. Planned funding is better than forced funding.

How often should the board revisit reserve decisions

Regularly, and not only when the budget is due.

Boards should revisit reserve assumptions whenever major projects change, costs shift materially, or property conditions change. Reserve planning works best when it is part of ongoing governance rather than a once-a-year scramble.

What is the biggest mistake a new board president makes

Confusing peace with stability.

A quiet meeting and a flat dues increase can feel like success. They are not success if the association is drifting toward a reserve shortfall. The strongest board presidents are willing to absorb short-term discomfort to prevent long-term damage.

What should a Georgia condo board focus on right now

Three things.

First, confirm what the association is responsible for maintaining. Second, make sure the reserve study and budget reflect those obligations. Third, communicate early and clearly with owners before capital needs become emergencies.

That approach is not flashy. It works.

If your board needs help turning reserve confusion into a workable plan, Access Management Group can help your condominium association build stronger financial processes, clearer board communication, and more disciplined long-term planning for the community you are responsible for protecting.