A lot of new board members have the same first insurance moment. The renewal packet lands in their inbox, it is dense, full of exclusions, endorsements, deductibles, and coverage forms, and it reads like something written for underwriters instead of volunteers.

That reaction is normal. It is also dangerous if the board stops there.

A master insurance policy for homeowners association is not just another annual expense to approve and move on from. It is the financial backstop for the buildings, the common areas, the association’s liability, and in many cases the board itself. If it is poorly structured, the community can end up with claim disputes, owner frustration, financing problems, and special assessments that could have been reduced or avoided.

Many boards underestimate the risks involved. In a recent two-year period, average HOA master insurance premiums increased 90.4%, and insurance consumed over 34% of a typical association’s operating budget, according to the Minnesota HOA Insurance Survey Results. Georgia boards are feeling the same pressure from a harder insurance market, higher rebuilding costs, and more scrutiny from carriers.

That is why insurance review belongs in the category of fiduciary duty, not clerical work. A board does not need to become an insurance adjuster or attorney. It does need to understand what it is buying, what it is not buying, and what that means for homeowners when a storm, fire, water loss, or liability claim hits the community.

Your Introduction to the HOA Master Policy

The board packet rarely explains the core issue. It shows a premium, a deductible, and maybe a one-page summary. What it usually does not show is the practical question every director should ask first.

What exactly are we protecting, and who is exposed if we get this wrong?

For most associations, the answer starts with the community’s shared assets. Roof systems, exterior walls, stairwells, clubhouses, pools, signage, parking areas, and other common elements represent a major concentration of value. If a serious loss happens and the policy is outdated or misaligned with the governing documents, the association may have to fund part of the repair itself.

That is where boards often learn an uncomfortable lesson. The cheapest renewal is not always the least expensive decision. A lower premium can come with a narrower property form, a larger deductible, weaker liability terms, or policy wording that shifts more post-loss cost back onto owners.

Practical takeaway: When a board reviews insurance, the first job is not to ask, “How do we lower this bill?” The first job is to ask, “If we have a major claim next month, how will this policy respond?”

In Georgia, this matters even more in condominium and townhome communities where the association insures structures that multiple families depend on at the same time. One bad claim can affect owner habitability, lender requirements, reserve planning, and resale activity all at once.

A sound master policy gives the board a defensible position. It helps the association rebuild. It helps owners understand where their own policy begins. It helps avoid unnecessary disputes. Most of all, it shows the board acted prudently with a community asset that now takes up a much larger share of the budget than it did only a short time ago.

The Foundation of Your Community's Protection

Think of the master policy as the insurance equivalent of a building-wide shield. It protects the property and exposures the association owns or controls. It does not replace the insurance an individual owner needs for personal belongings, interior finishes beyond the policy scope, or personal liability within a unit.

That distinction is easier to understand with a simple comparison. If an apartment owner insures the entire building and each tenant buys renters insurance for personal property, the HOA model is similar. The association covers the shared structure and common risks. The owner covers the private side of ownership.

What the master policy is really for

A proper master policy is designed to protect the collective interests of all owners. It generally addresses two broad categories first.

- Shared property risk: Buildings, exteriors, common systems, and amenities the association is obligated to maintain.

- Association liability risk: Claims that arise from common area conditions, board decisions, or association operations.

For boards, that means the policy is not optional in any practical sense. Even if the governing documents create the direct obligation, the market enforces it too. Lenders, buyers, owners, and carriers all expect the association to maintain appropriate coverage.

Why financing rules matter to the board

One of the biggest mistakes boards make is treating insurance as an issue only for claim season. It also affects routine sales and refinances.

Fannie Mae requires community associations to carry master property insurance that settles claims on a replacement cost basis. Policies written on an actual cash value basis are unacceptable and can interfere with a homeowner’s ability to obtain or refinance a mortgage, as stated in the Fannie Mae Selling Guide master property insurance requirements.

That point gets overlooked because the board may never see the failed loan application. The owner, buyer, lender, and closing attorney see it first. But the root problem often traces back to the association’s insurance structure.

What boards should remember

A master insurance policy for homeowners association is not just there to satisfy a line item in the budget. It supports:

- Physical recovery after a loss

- Financial stability for the association

- Mortgage eligibility for owners and buyers

- Market confidence in the community

When boards treat the policy as part of asset preservation, they make better decisions. They ask harder questions. They document their reasoning. That protects homeowners as much as the policy itself does.

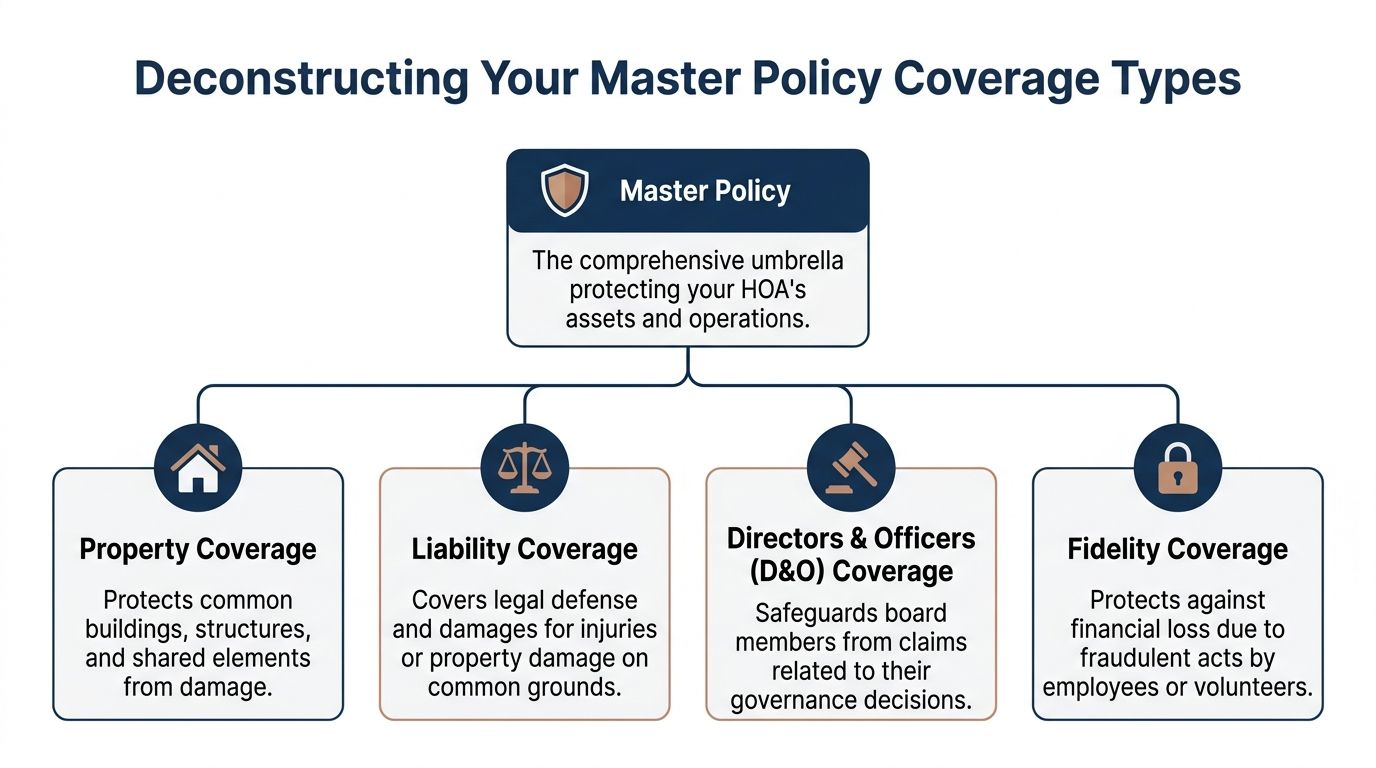

Deconstructing Your Master Policy Coverage Types

Boards often talk about “the insurance policy” as if it is a single product. In practice, a strong master program is a package of protections aimed at different types of risk. If one part is weak, the whole community can still be exposed.

Property coverage

This is the core of the master policy. Property coverage addresses direct damage to insured buildings and common elements after a covered event.

If a storm tears roofing materials off a clubhouse, if a fire damages a corridor, or if a plumbing failure affects shared walls and ceilings, this is the part of the policy the board will turn to first. It is also the coverage most likely to drive premium volatility because carriers are looking closely at roof age, prior losses, maintenance history, and replacement values.

Boards should focus on three practical questions here:

- What property is scheduled and insured

- Whether the valuation reflects current rebuilding conditions

- How the deductible applies to likely claims such as water, wind, or hail

A board can have property coverage and still be underprotected if the insured values are stale or the deductible is so high that a mid-sized loss creates immediate financial strain.

General liability coverage

Property losses get attention because they are visible. Liability claims are often quieter and more expensive to defend.

General liability coverage is what protects the association when someone alleges the HOA caused bodily injury or property damage in a common area. Typical scenarios include a trip on broken pavement, an injury at the pool, a falling tree limb in a common space, or damage tied to association maintenance work.

This coverage matters because the legal defense itself can be costly, even when the board believes the association acted appropriately. The value is not only in paying a settlement if needed. It is in giving the community a defense framework when a claim is made.

Board lens: Liability insurance is less about expecting to lose a lawsuit and more about making sure one claim does not force the association to defend itself out of operating cash.

Directors and officers coverage

Volunteer directors make decisions that affect budgets, rules enforcement, contracts, architectural review, records access, and collections. Those decisions can draw complaints even when the board acts in good faith.

Directors and Officers liability, usually called D&O, is designed to protect board members and the association against claims arising from governance decisions. This is the policy that may respond when an owner alleges selective enforcement, improper procedure, breach of governing authority, or wrongful acts tied to board conduct.

A lot of new board members assume the general liability policy protects them personally in these situations. Usually it does not. Slip-and-fall coverage and governance liability are different issues. Disciplined board process matters here. D&O carriers want to see that the board follows the documents, uses counsel when needed, keeps minutes, and makes decisions through a documented process instead of informal side conversations.

Fidelity and crime coverage

Associations handle dues, reserve funds, vendor payments, and access to operating accounts. Any organization that handles money has theft risk. HOAs are no exception.

Fidelity or crime coverage is meant to protect the association if funds are stolen or misused by someone with access, whether that involves an employee, volunteer, or another party in the financial chain depending on the form and endorsements. Boards should confirm who is covered, what triggers the coverage, and whether management company handling is contemplated if applicable.

This is one of the least discussed parts of the package until there is a problem. Then it becomes urgent.

Why all four matter together

A board that buys only for visible building damage misses the larger risk profile of the community. The stronger approach is to look at the full operating environment.

| Coverage area | Main risk it addresses | Common board mistake |

|—|—|

| Property | Damage to insured structures and common elements | Focusing only on premium, not valuation and deductibles |

| General liability | Injury or damage claims tied to common areas | Assuming “we are careful” means claims are unlikely |

| D&O | Challenges to board decisions and governance actions | Believing volunteers are automatically protected |

| Fidelity/crime | Theft or misuse of association funds | Treating internal controls as a substitute for insurance |

Reading these forms is difficult even for experienced directors. A useful homeowner-facing primer on policy language is how to read your homeowner or business insurance policy. It helps explain why declarations pages alone never tell the whole story.

What works and what does not

What works is a board that reviews the full package annually with a broker who understands community associations, then documents why it selected the structure it did.

What does not work is approving renewal based on a summary page, assuming prior boards already handled the hard parts, and discovering after a claim that one of the four pillars was missing or too thin.

The Critical Link Between Master and Owner Policies

The most common insurance conflict in a condominium or attached-home community is not whether there is coverage at all. It is whether the claim belongs to the association’s policy, the owner’s policy, or both.

That line gets tested hard during water losses.

The pipe leak example boards deal with all the time

Take a burst pipe inside a shared wall that affects three units. Water damages drywall, flooring, cabinetry, and paint. Hallway materials outside the units are affected too.

The answer to “who pays for what” depends first on how the master policy is written and what the governing documents require.

All-in coverage

Under an all-in or single entity structure, the master policy generally reaches farther into the unit. It often covers original interior components that were part of the initial build, subject to policy wording and exclusions.

That usually produces a cleaner claim path for original finishes. It does not mean every interior item is automatically covered. Owner upgrades and betterments can still fall back to the owner’s policy.

Walls-out coverage

Under a walls-out or bare walls structure, the master policy usually stops with the building shell and common elements. Drywall, fixtures, flooring, cabinets, and similar interior components generally become the owner’s insurance issue.

That shift sounds simple in theory. In real claims, it creates friction. Associations with walls-out policies see 40% more assessment disputes after a claim, according to All Property Management’s discussion of HOA master insurance policy structures.

Why homeowners need an HO-6 policy

An owner policy, often called an HO-6, fills the gap between private ownership and association coverage. In practical terms, it can help with:

- Interior repairs that the master policy does not cover

- Personal belongings

- Personal liability inside the unit

- Certain assessments passed through from the association

Owners often do not realize how important the last point is until they receive an invoice tied to the master deductible or an uninsured portion of a community loss.

For water-related questions, homeowners often benefit from plain-English claim examples such as this condo owner's guide to water damage insurance coverage, especially when they are trying to understand where building damage ends and personal-unit responsibility begins.

Loss assessment coverage is the missing conversation

Many boards do a decent job telling owners to “carry HO-6 insurance.” Far fewer explain loss assessment coverage, which is the part of the owner policy that may help pay the owner’s share of a covered assessment from the association.

This matters when the HOA has a large deductible or a claim allocation under the documents. The board may be allowed to assess owners for their share. If the owner’s policy has weak loss assessment coverage, the owner may have to pay the difference personally.

Best practice: Boards should not assume owners understand their side of the insurance equation. Annual owner reminders about HO-6, interior improvements, and loss assessment coverage prevent confusion later.

The governing documents decide more than people expect

Policy language matters, but the declaration matters too. Many claim disputes come from a mismatch between what the policy says and what the governing documents assign to the association.

That is why boards should review the community’s insurance obligations in the declaration and bylaws before each renewal. If your board needs a starting point for document review, the association’s governing documents for HOA interpretation and responsibilities should always be part of the renewal conversation.

The board’s job is not only to buy insurance. It is to make sure the master policy and owner expectations line up with the legal structure of the community.

A Board's Guide to Choosing and Managing Insurance

Insurance decisions become much easier when the board uses a repeatable process. Without one, renewal season turns into a rushed conversation about price and the community absorbs whatever hidden trade-offs came with the quote.

Start with the documents

Before the board talks to a broker, it should review the declaration, bylaws, and any insurance resolutions already in place. These documents often answer key questions:

- What property the association must insure

- Whether the community is intended to be all-in or bare walls

- How deductibles can be allocated

- Whether there are minimum coverage standards

Skipping this step is one of the fastest ways to buy a policy that looks acceptable but conflicts with the association’s legal obligations.

Use a community-association broker, not a generalist

The broker matters. A broker who handles community associations regularly will ask different questions than a generalist who mainly writes small business or personal lines coverage.

The right broker should be able to explain:

- How the property form matches the governing documents

- How deductibles apply in multi-unit claims

- What exclusions deserve board attention

- What owner communication issues are likely after a loss

Boards should expect clear comparisons, not just a recommendation.

Compare more than premium

A disciplined board review usually includes side-by-side comparison of at least these factors:

| Review point | What the board should ask |

|---|---|

| Coverage form | Does the policy structure align with the documents and owner expectations? |

| Deductibles | Could the association realistically absorb or assess this amount after a claim? |

| Property valuation | Do the insured values appear current for the buildings and common assets? |

| Liability and D&O terms | Are governance and premises exposures both addressed? |

| Carrier responsiveness | Will this insurer handle a difficult claim efficiently? |

The lowest premium is sometimes appropriate. It is not automatically prudent.

Document the decision like a fiduciary

Once the board selects a policy, it should record the rationale in meeting minutes. That does not require pages of legal analysis. It does require enough detail to show that the board reviewed options, discussed deductibles, understood coverage structure, and acted deliberately.

That kind of record helps in two ways. It supports continuity for future boards, and it shows owners that the board used a reasoned process.

Good board practice: If owners challenge the renewal later, the board should be able to show how it evaluated risk, not just that it voted yes.

Review annually, educate annually

Insurance should be revisited every year, not only when there is a big claim. Buildings age. amenities change. roof conditions evolve. market terms harden. owner confusion never solves itself.

Boards that want a stronger governance framework should also review broader HOA board responsibilities because insurance oversight sits squarely inside that fiduciary role.

What works is consistency. Review the documents, review the market, review owner exposure, then communicate clearly. What fails is treating renewal as a signature exercise.

Navigating the Claims Process Like an Expert

When a major incident hits, the board’s first decisions shape the claim. Strong claims handling is not about sounding technical. It is about moving in the right order.

First hour priorities

Safety comes first. If the event involves active water intrusion, fire, structural concerns, electrical hazard, or injury, the board and manager should focus on emergency response and mitigation before debating insurance details.

That usually means securing the area, limiting further damage, and coordinating emergency vendors as allowed by the association’s procedures.

Report early and document everything

The carrier should be notified promptly once the situation is stabilized. Delays create problems. So does incomplete reporting.

The board or manager should gather:

- Photos and video from multiple angles

- Date and time of discovery

- Location details

- Initial incident notes from witnesses or staff

- Emergency mitigation invoices and vendor reports

- Any owner reports from affected units

Good documentation helps the adjuster understand the loss quickly. It also helps the board keep a clean record if coverage questions come up later.

Make the adjuster visit productive

When the adjuster arrives, the board should have one point of contact. In most communities, that is the manager or another designated representative. Too many voices create confusion.

Useful claim meetings are organized around facts:

- what happened

- what was damaged

- what emergency work has already been done

- what access is needed next

If there is uncertainty about whether damage belongs under the master policy or an owner policy, the board should avoid making off-the-cuff promises. Confirm facts first, then communicate based on policy position and document obligations.

Keep owners informed without speculating

Claims fail socially before they fail technically. Rumors spread fast in common-interest communities.

A clear board communication should tell owners:

- What occurred

- What immediate action the association took

- Whether owners should contact their own carrier

- How updates will be shared

- What is still under review

Communication rule: Tell owners what the board knows, what the board is doing next, and what owners should do now. Do not guess about coverage before the investigation is complete.

Boards that stay organized through the first several days usually reduce conflict, speed repairs, and preserve confidence in the association’s leadership.

Special Insurance Considerations for Georgia HOAs

Georgia boards should be cautious about relying on generic national insurance advice. The legal structure of the community and the regional loss profile both matter.

A condominium association in Georgia may have different insurance obligations than a homeowners association with detached homes and shared amenities. The declaration, plats, maintenance matrix, and applicable statutory framework all shape what the association is expected to insure. A board that assumes every HOA should buy the same package often ends up either overinsuring the wrong things or leaving a gap where the documents assign responsibility to the association.

Regional weather risk also changes the conversation. Georgia communities may face tornado activity, hail, severe thunderstorms, and in some areas hurricane-related wind and water impacts. Those exposures affect deductibles, underwriting questions, and endorsements. A board should evaluate coverage with those perils in mind rather than using a template from a market with very different conditions.

This local focus also matters financially. If a community experiences a significant uninsured or underinsured loss, the board may have to use reserves or levy a special assessment. For many owners, that is where insurance strategy becomes personal. Boards that want to understand the owner impact of those funding decisions should also consider the practical realities behind a condominium special assessment and how insurance gaps often lead to one.

The strongest Georgia boards match the policy to three things at once: the governing documents, the property’s actual construction and maintenance obligations, and the storm patterns carriers are underwriting in this state. Anything less is guesswork.

Answering Your Most Pressing Insurance Questions

What is a loss assessment coverage gap

A loss assessment coverage gap happens when the association passes along an assessment tied to a covered loss, but the owner’s HO-6 policy does not carry enough loss assessment protection to absorb it.

That is not a theoretical issue. A 2026 study cited by Pro Insurance Group reported that after California wildfires, 35% of condo owners exhausted their HO-6 limits and faced average out-of-pocket costs of $22,000 for special assessments, as discussed in what is an HOA master insurance policy. A major Georgia storm could create similar owner stress where deductibles and shared rebuilding costs are substantial.

Our premium jumped even though we had no claim. What can we do

Boards should resist the urge to react only by increasing deductibles or cutting coverage. A better response is to review the full risk profile.

Focus on:

- Loss prevention, especially roof maintenance, water intrusion control, and site safety

- Valuation review, so the board understands whether the increase is driven by replacement cost changes

- Market testing, using a broker who knows association coverage

- Owner education, because owner-caused losses and delayed reporting often worsen claim outcomes

Some cost pressure is outside the board’s control. The board can still control how cleanly the property is maintained and how intelligently the policy is structured.

We received a non-renewal notice. What now

Act immediately. Non-renewal is not something to set aside for the next board meeting.

The board should gather the current policy, claims history, property details, and governing document insurance requirements, then engage a qualified association broker to remarket the account. At the same time, the board should identify any property conditions the outgoing carrier flagged. Sometimes the issue is loss history. Sometimes it is deferred maintenance. Sometimes it is broader carrier retrenchment.

A calm, documented response works far better than rushing into the first replacement quote that appears.

If your board wants experienced guidance on insurance review, claims coordination, governing document alignment, and the broader operational demands of community governance, Access Management Group brings decades of Georgia community association management experience to that work. Their team has long focused on helping associations protect, preserve, and enhance real estate investments while supporting boards, presidents, and homeowners with practical, high-level management expertise.