You open the mail, see a notice about unpaid assessments, and your stomach drops. If you're a homeowner, your first thought is usually personal and immediate. How bad is this, what happens next, and can this put my home at risk?

If you're a new board member, the same notice feels different. You know your association needs assessment income to pay for landscaping, insurance, utilities, repairs, and reserve obligations, but you're also talking about your neighbors. That tension is real in every Georgia community.

Homeowners association liens sit right in the middle of those two concerns. They are a collection tool, but they also protect the shared financial foundation of the community. This isn't a niche issue either. Approximately 6.7 million HOA member first mortgages in the U.S. are affected by outstanding liens, with unpaid principal balances estimated at around $11.8 billion, according to Equifax's report on the hidden threat of HOA liens.

A good lien process should never feel mysterious. Homeowners need to understand what a notice means, what rights they have, and what they can still do to fix the problem. Boards need to understand when to act, how to follow Georgia law and governing documents, and how to collect fairly without making the situation worse.

Navigating Your First HOA Delinquency Notice

Sarah, a homeowner in a Georgia subdivision, misses a payment after an unexpected expense. She means to catch up next month. Then a letter arrives from the association about a delinquent balance. She reads the words "late fees," "collection," and "lien," and suddenly a manageable problem feels like a legal crisis.

That reaction is common. Most owners don't deal with homeowners association liens until they're already under stress. They may assume the board is targeting them personally, when the board is often following a collection policy it adopted because the community depends on regular assessments to function.

From the board's side, the issue looks different. If one owner doesn't pay, the shortfall doesn't disappear. The association still has to maintain common areas, pay vendors, and meet budget obligations. Volunteer board members have a duty to act for the benefit of the whole association, not just the owners who are current on their accounts.

A delinquency notice is serious, but it usually isn't the end of your options. In many cases, it's the best time to act because the matter is still easier and cheaper to resolve.

For both sides, the first notice should trigger communication, not panic.

What the notice usually means

A first delinquency letter often means:

- The account is behind: The association believes assessments, charges, or other amounts allowed by the governing documents remain unpaid.

- The clock has started: If the balance isn't resolved, the account may move into a more formal collection stage.

- Records matter now: Payment history, ledger entries, notice dates, and governing document provisions become important.

What each side should do first

| Person | Best first move |

|---|---|

| Homeowner | Review the amount, compare it to your records, and contact the association or manager quickly |

| Board member | Confirm the account is accurate and make sure the collection process follows the governing documents and counsel's direction |

A calm response early often prevents a much harder fight later. In Georgia communities, that practical approach protects both the owner's home and the association's financial stability.

What Exactly Is a Homeowners Association Lien

An HOA lien is easiest to understand if you think of it as a reserved spot for a debt on your property's legal record. The association claims an interest tied to the home because money owed to the community hasn't been paid.

That doesn't mean the HOA suddenly owns the home. It means the debt is no longer just a personal bill. The property itself becomes security for what is owed.

Why the association has this power

An HOA doesn't invent lien authority out of thin air. The power usually comes from the community's recorded covenants and other governing documents that bind every owner when they buy into the association. If you want a useful refresher on where those powers generally come from, review your community's governing documents for an HOA.

In plain language, the documents usually say something like this: every owner must pay assessments, and if they don't, the association may use collection remedies that include a lien.

What debt can be secured

The exact categories depend on the governing documents and applicable law, but the lien usually relates to amounts the association is authorized to charge, such as:

- Regular assessments: Monthly, quarterly, or annual dues.

- Special assessments: Extra charges approved for major repairs or unexpected community costs.

- Other authorized charges: In some communities, that can include late fees, interest, collection costs, or certain fines if the documents and law allow it.

Why a lien matters more than a late bill

A late utility bill is unsecured. The company may try to collect, but it doesn't usually attach that debt to your real estate title. A homeowners association lien is different because it follows the property.

That creates practical pressure in ways many owners don't expect:

- You may have trouble selling until the balance is resolved.

- A refinance can stall because title has to be cleared.

- Legal costs can grow if the account moves deeper into collection.

Practical rule: A lien doesn't just say, "you owe money." It says, "this debt is tied to the house."

That distinction is what gives homeowners association liens their power. It also explains why boards must use them carefully and why owners should never ignore early notices.

The Legal Mechanics of HOA Liens in Georgia

Georgia owners and board members often get tripped up by one question first. Does the HOA jump ahead of the mortgage? In most cases, no. That's the starting point for understanding lien priority here.

Georgia and lien priority

Georgia is generally understood as a non-super lien state in this context. In super lien states, an HOA foreclosure can wipe out a first mortgage. In non-super lien states, the HOA lien is generally subordinate to the first mortgage, while still taking priority over second mortgages and other junior liens, as described in First American's discussion of getting the most from HOA lien data.

For a Georgia homeowner, that means the first mortgage lender usually remains ahead of the association. For a board member, it means the HOA still has a powerful collection tool, but not the same influence that exists in a super lien jurisdiction.

Automatic attachment and recording

Another point that confuses people is the difference between a lien existing and a lien being recorded.

In most jurisdictions, HOA liens attach automatically upon delinquency. State laws vary. Some, like Oregon, don't require recording for the lien to be valid, while others require formal recording to perfect the lien and provide public notice, which matters for title searches, as explained in Nolo's overview of HOA liens and foreclosures.

In Georgia practice, homeowners and boards should treat recording as a major step because it's the point where the claim becomes much more visible in the public record and much harder to ignore in any sale or refinance setting.

The usual Georgia sequence

The legal path often looks something like this:

- Assessments become delinquent: The owner misses payment under the schedule required by the governing documents.

- The association sends notice: The owner receives a delinquency notice or demand.

- Opportunity to cure: The owner may have a chance to pay, dispute the account, or request a plan.

- Claim of lien is prepared and recorded: If the account remains unresolved, association counsel may record the lien in county records.

- Collection escalates if needed: That can include further demand, litigation, or in some cases foreclosure steps, depending on the documents, facts, and legal advice.

Why boards must be precise

A lien isn't just paperwork. It's a legal claim against real property. Boards need exact ledgers, proper authorization, and consistent procedures. A sloppy process can create unnecessary disputes and, in some situations, weaken enforcement.

That's one reason contract principles matter so much. If a board is enforcing payment duties that arise from recorded covenants, it helps to understand the legal framework behind obligations and breach. Homeowners and board members who want a plain-language legal primer may find this explanation of elements for breach of contract useful when thinking about promises created by governing documents.

The strongest collection file is usually the least dramatic one. Clear records, proper notice, and consistent treatment carry more weight than angry emails or improvised deadlines.

Your Rights and Obligations as Homeowner or Board Member

Most lien disputes get worse when one side focuses only on power and ignores responsibility. In a healthy Georgia association, both matter. Owners have payment duties, but they also have rights. Boards have collection authority, but they also have limits.

For the homeowner

Your first obligation is simple. Pay assessments on time under the governing documents, even if you're frustrated about another issue in the community. In most associations, disputes about maintenance, rules, or neighbor conduct don't automatically erase the duty to pay.

That said, you still have practical rights worth using early.

Rights worth exercising quickly

- Notice rights: You should receive clear notice that the account is delinquent before the matter advances further.

- Account review: Ask for a current ledger or statement so you can see what the association says you owe.

- Dispute rights: If you believe charges are wrong, raise the issue in writing and keep copies.

- Opportunity to resolve: Many disputes can be settled before a recorded lien or foreclosure process if the owner responds promptly.

A smart homeowner response is organized, not emotional. Gather proof of payments, bank confirmations, correspondence, and any governing document language that supports your position.

Mistakes owners make

| Mistake | Why it hurts |

|---|---|

| Ignoring letters | The file moves forward while costs may increase |

| Paying informally without documentation | You may struggle to prove what was paid and when |

| Fighting unrelated issues at the same time | It distracts from the core account problem |

| Assuming the board will "understand" without a written request | Unwritten understandings are hard to enforce |

For the board

Board members don't serve as debt collectors for personal reasons. They serve as fiduciaries for the association. If assessments aren't collected, the board may fail the owners who do pay on time.

A board's duty includes adopting and following a fair process. If you're new to governance, a practical overview of HOA board member responsibilities can help frame how collections fit into the larger job.

Core obligations for boards

- Act consistently: Similar delinquencies should be handled under the same policy, not based on friendships or pressure.

- Follow the documents: Collection steps must line up with the declaration, bylaws, rules, and legal counsel's advice.

- Keep clean records: Ledgers, notices, dates, votes, and attorney communications should be accurate and organized.

- Use good faith judgment: The board should protect the association without escalating casually.

What boards should remember about priority

In super lien states, an HOA foreclosure can extinguish a first mortgage entirely. In non-super lien states, the HOA lien is subordinate to the first mortgage, but still takes priority over second mortgages and other junior liens, according to First American's explanation summarized earlier in this article. For Georgia boards, that means collection strategy must reflect the limits and realities of a non-super lien framework.

Board members should think like stewards, not punishers. The goal is to collect what the community needs while preserving fairness and trust.

Shared responsibilities

Owners and boards need the same thing more often than they realize:

- Accurate numbers

- Prompt communication

- Written agreements

- Predictable procedures

When those four pieces are in place, homeowners association liens become easier to avoid, easier to resolve, and less likely to turn into neighborhood conflict.

The Consequences of an Unresolved HOA Lien

Upon hearing "lien," many think only about foreclosure. That's understandable, but it's not the first consequence most owners feel. The first damage is often practical. The property becomes harder to finance, harder to transfer, and harder to market.

What happens to the owner

A recorded lien can block ordinary life events.

- Selling gets complicated: Buyers, lenders, and title companies want clear title. A lien usually has to be addressed before closing.

- Refinancing can stall: A lender reviewing title may require the lien to be resolved first.

- Costs may keep growing: The longer the issue remains open, the more difficult it can become to unwind.

Even when foreclosure isn't imminent, the pressure is real because the debt is attached to the property itself.

What happens to the community

An unresolved lien problem doesn't stay private for long. When multiple accounts become seriously delinquent, buyers and lenders may begin to view the community as unstable.

That community-level risk deserves more attention than it usually gets. It's known that liens can deter lenders and lower home values, but there is little guidance on the threshold at which lien concentration causes lender pullback. Spectrum notes that this creates a strategic challenge for boards trying to manage collections while protecting the community's marketability and lender relationships in its discussion of how HOA board members handle liens.

Why this changes board strategy

That uncertainty puts boards in a difficult position. If they collect too slowly, unpaid accounts can pile up and strain the budget. If they collect harshly and without communication, they may increase conflict and damage owner confidence.

A thoughtful board usually asks questions like these:

- Are we giving owners a real chance to cure before legal escalation?

- Are our records strong enough to support each account decision?

- Are we protecting the association's income without creating unnecessary market stigma?

A lien is never just one owner's problem for very long. In a shared-interest community, financial distress tends to spread through budgets, buyer perception, and lending decisions.

That is why homeowners association liens should be treated as both an individual account issue and a community health issue. Boards need a process that enforces obligations. Owners need to understand that fast action protects more than just their own file.

A Practical Guide to Preventing and Resolving Liens

The best lien file is the one that never needs to be recorded. In real communities, that usually comes down to fast communication, clear documentation, and realistic solutions before the account hardens into a legal matter.

If you're a homeowner

Start as soon as you know payment may be a problem. Don't wait until you can pay in full if that delay means silence.

Contact the association or manager early

Say what's happening and ask what options exist. A short, respectful email is better than no response at all.Request a written ledger

Make sure you understand the full balance being claimed. Small misunderstandings grow fast once legal fees enter the picture.Ask for a payment plan if you need one

Don't promise an amount you can't maintain. A smaller plan you can complete is more useful than an ambitious plan that fails immediately.Dispute in writing if you believe the account is wrong

Identify the charge, the date, and the reason you dispute it. Attach proof.Keep every document

Save notices, screenshots, emails, payment confirmations, and any agreement you reach.

If the account has advanced toward foreclosure, timing becomes even more important. Homeowners trying to understand the last stages of that process may benefit from reading about when it's too late to stop foreclosure, especially so they know when delay becomes dangerous.

If you're on the board

Boards prevent many lien disputes by building a predictable collection system before trouble starts.

A workable board playbook

- Use a written collections policy: Owners should know what happens after a missed payment, what notices go out, and when legal counsel gets involved.

- Offer structured payment plans when appropriate: Flexibility can improve collections if the terms are clear and consistently applied.

- Separate hardship from hostility: An owner in temporary trouble needs a different tone than an owner who refuses to engage.

- Escalate deliberately: Recording a lien should follow failed notice and cure efforts, not replace them.

A short decision guide

| Situation | Better first response |

|---|---|

| Owner missed one payment and communicates quickly | Send ledger, discuss cure terms |

| Owner disputes a special charge | Review documents and account entries before escalating |

| Owner ignores repeated notices | Move according to policy and legal advice |

| Account involves a large project charge | Communicate carefully, especially if the balance includes a special assessment |

Special assessments often trigger the most emotional disputes because owners may agree they owe regular dues but object to a large one-time charge. When boards need a plain-language explanation for owners, this overview of a condominium special assessment helps clarify why those charges can arise.

This is also where management systems matter. Some associations use management partners to automate late notices, track balances, and coordinate with legal counsel. Access Management Group, for example, provides assessment invoicing, collection monitoring, and real-time account access as part of community association financial management.

What resolution usually looks like

Most successful resolutions are surprisingly ordinary:

- The owner pays in full.

- The parties agree on a written plan.

- A disputed charge gets corrected.

- Counsel records a satisfaction or release after payment.

What rarely works is avoidance. Homeowners association liens become more expensive and more stressful when nobody takes the first reasonable step.

Understanding Lien Timelines and Official Notices

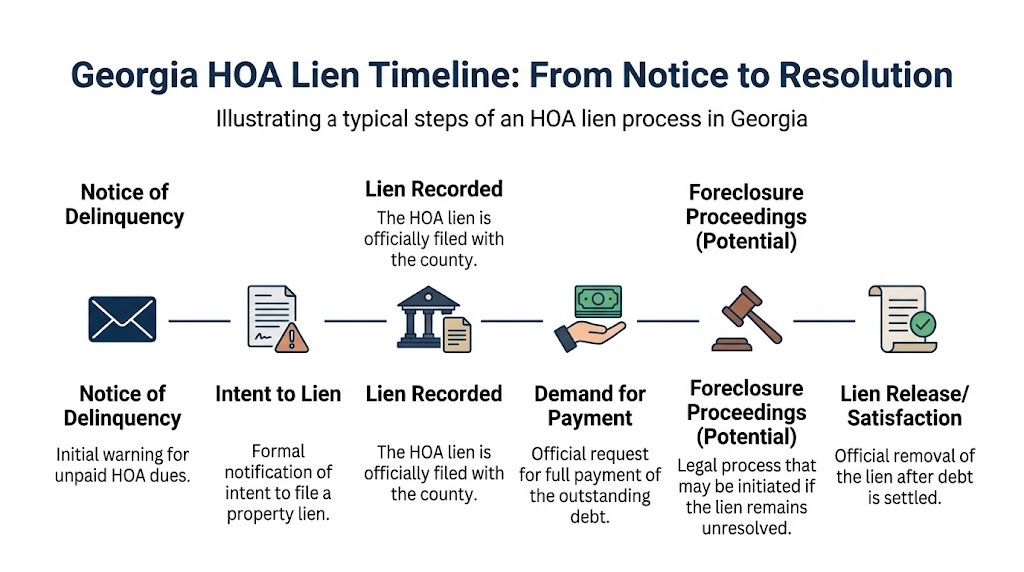

Legal notices look intimidating because they are supposed to get your attention. Still, most of them are easier to understand once you know their job. Each document marks a stage in the association's collection process.

What the notices usually mean

A typical Georgia file may include documents like these:

- Notice of delinquency: The first formal warning that the account is behind.

- Intent to lien: A more serious notice that tells the owner the association may file a lien if the debt isn't cured.

- Claim of lien: The document recorded in county records asserting the association's claim against the property.

- Demand for payment: A request for payment of the stated balance, often after the matter has escalated.

- Foreclosure notice: The most serious notice. It signals that the association may pursue sale remedies if the debt remains unresolved.

- Lien release or satisfaction: Confirmation that the lien has been cleared after payment or resolution.

A practical timeline

The exact dates depend on the governing documents, account history, and legal advice, but the flow usually follows this pattern:

| Stage | What the owner should do |

|---|---|

| First missed payment | Check your records and pay or ask questions immediately |

| Initial notice arrives | Request a ledger and clarify the amount claimed |

| Intent to lien arrives | Treat the matter as urgent and seek a written resolution |

| Lien is recorded | Understand that title issues are now more likely |

| Foreclosure steps begin | Get legal advice fast and review all cure options |

| Balance is resolved | Confirm the lien release is processed and documented |

How boards should use notices

Boards should treat notices as compliance tools, not pressure tactics. Every notice should be accurate, timely, and supported by the account file. If the association can't explain the balance clearly, it isn't ready to escalate.

Official notices are not just warnings. They create the paper trail that courts, closing attorneys, and title professionals may later rely on.

For homeowners, the most important takeaway is simple. The earlier the notice, the more options you usually have. For boards, the same timeline sends a different message. Precision early prevents expensive disputes later.

Frequently Asked Questions About HOA Liens

Can an owner sell a home if there's an HOA lien

Yes, sometimes. But the lien usually has to be addressed during the sale. In practice, the closing process often requires the balance to be paid, settled, or otherwise cleared so title can transfer cleanly.

Does bankruptcy make the lien disappear

Bankruptcy can affect collection efforts, but it doesn't automatically make every issue vanish. Owners and boards should get legal advice quickly because bankruptcy changes what actions can continue and what must pause.

Who pays the legal fees tied to the lien

That depends on the governing documents, the account history, and applicable law. Many communities have document provisions allowing certain collection costs to be charged back to the delinquent owner, but no one should assume. Check the declaration, bylaws, collection policy, and counsel's guidance.

How long can an HOA lien remain a problem

Long enough to interfere with a sale, refinance, or broader dispute if it isn't resolved properly. The better question is not how long it can sit there, but whether the parties have confirmed the amount, the authority behind it, and the path to release it.

Can a homeowner dispute the amount even after notices have started

Yes. In fact, owners should raise legitimate disputes as soon as possible and in writing. Waiting until the account is at the courthouse is usually the most expensive point to start sorting out a ledger issue.

What should a new board member ask first

Ask for the governing document provisions on assessments and collections, the written collection policy, and a sample delinquency timeline used by counsel or management. A board member who understands those three things will make better decisions and avoid inconsistent enforcement.

Is every delinquent account supposed to end in a lien

No. Many don't. Some are cured after the first notice. Others are resolved through a payment plan or account correction. A lien is a tool for unresolved cases, not the preferred outcome in every case.

If your community needs help handling assessments, notices, owner communication, and the practical side of collections with care, Access Management Group works with Georgia associations to support boards, homeowners, and community presidents in protecting the association's financial health while keeping processes clear and organized.