If you’ve just joined an HOA or COA board in Georgia, reserve talk can feel abstract until the first major repair lands on your agenda. Then it becomes very real. The roof is aging. The pool surface is failing. The pavement is breaking down. Owners want answers, and they want to know whether the board planned ahead.

That’s why understanding reserve and reserve fund issues matters so much. For a new board member, this isn’t just an accounting topic. It’s one of the clearest tests of fiduciary judgment. You’re deciding whether your community will handle predictable long-term expenses calmly, or force homeowners into financial stress when those expenses arrive.

Why Your Community's Future Depends on Its Reserve Fund

Two boards can face the same repair and have completely different outcomes.

In one community, the board learns that a major common-area roof has reached the end of its life. The contractor’s proposal sparks panic. Owners ask whether dues are going up immediately. Some can pay. Some can’t. Tempers rise, collections become a concern, and the board starts discussing a special assessment with little room to maneuver.

In the other community, the same type of repair shows up as a planned reserve project. The board already knew the roof was aging. The cost had been anticipated. Money had been set aside over time. The repair is still expensive, but it doesn’t become a crisis.

That difference is what a reserve fund does. It turns a predictable major expense into a managed event instead of a community-wide shock.

What boards are really protecting

A reserve fund protects more than a bank balance.

- Homeowner stability: Owners are less likely to face sudden large bills when the board plans ahead.

- Property condition: The association can repair or replace shared assets when needed instead of delaying work.

- Board credibility: Homeowners trust boards that act early, communicate clearly, and avoid preventable emergencies.

- Community harmony: Fewer financial surprises usually means fewer angry meetings.

A broad analysis of association funding found that only 35% of homeowners associations are well-funded, meaning they have 71% or more of the reserves they need, while 23% are poorly funded at 0% to 30% funded, which puts them at high risk of special assessments for major projects, according to this reserve fund comparison analysis.

Practical rule: Reserve funding isn’t about saving for unlikely events. It’s about preparing for costs the board already knows are coming.

Why this matters to a Georgia board member

Georgia boards often feel pressure to keep dues low. That pressure is real. Owners notice every increase.

But low dues can hide a deeper problem if the association isn’t adequately contributing to reserves. When that happens, the board hasn’t made costs disappear. It has only delayed them, often until they return in a more painful form. If you need a plain-language explanation of that owner impact, this overview of special assessments is useful context.

A strong reserve fund is the financial bedrock behind steady dues, timely maintenance, and protected property values.

Understanding the Difference Between Reserve and Reserve Fund

New board members often hear these terms used as if they mean the same thing. They’re related, but they’re not identical.

A reserve is the financial concept. It means money the association sets aside for future major repair and replacement costs tied to common elements.

A reserve fund is the actual pool of money. It’s the account, or accounts, where those dollars are held and tracked.

A simple way to think about it

Use a personal finance example.

Your retirement goal is the plan. Your retirement account is where the money sits.

That’s the same distinction here.

- Reserve: the budgeting purpose

- Reserve fund: the money itself

- Operating fund: separate money for recurring, day-to-day expenses

Boards get into trouble when those lines blur.

Why the distinction matters in practice

If the board says, “We have reserves,” that should mean more than a line item in a budget. It should mean the association has accumulated and protected funds for long-term obligations.

That separation matters for accounting, transparency, and owner trust. It also matters because reserve money should not feel like spare cash available for unrelated shortfalls.

If you want a broader nonprofit-style framework for understanding restricted funds, that concept helps many board members grasp why reserve dollars need disciplined handling.

Reserve money should be treated as designated for a defined purpose, not as a convenient backup for ordinary overspending.

The banking analogy helps

There’s a useful parallel in the banking world. Historically, the Federal Reserve required banks to hold reserves to support stability. Reserve requirement ratios were later set to 0% effective March 26, 2020, but the core idea remains the same: holding funds against future obligations supports financial stability, as explained by the Federal Reserve reserve requirement history.

For community associations, the principle is similar. The board holds funds against future liabilities tied to shared property.

Common points of confusion

Reserve fund is not the operating account

The operating account pays for recurring expenses such as utilities, groundskeeping service, management fees, and routine repairs. The reserve fund exists for major repair and replacement work that doesn’t happen every month.

Reserve contributions are not optional just because the expense is in the future

Boards sometimes think, “The roof still has time.” That logic is what creates underfunding. The useful life of a component is exactly why the association should contribute over time.

A healthy reserve process requires separate thinking

Board members should ask different questions about each bucket of money.

| Fund type | Main purpose | Typical board question |

|---|---|---|

| Operating fund | Recurring expenses | Can we cover this year’s routine bills? |

| Reserve fund | Major future repairs and replacements | Will money be there when key components wear out? |

When homeowners understand this difference, discussions about dues become more productive. They can see that reserve funding isn’t arbitrary. It’s part of responsible stewardship.

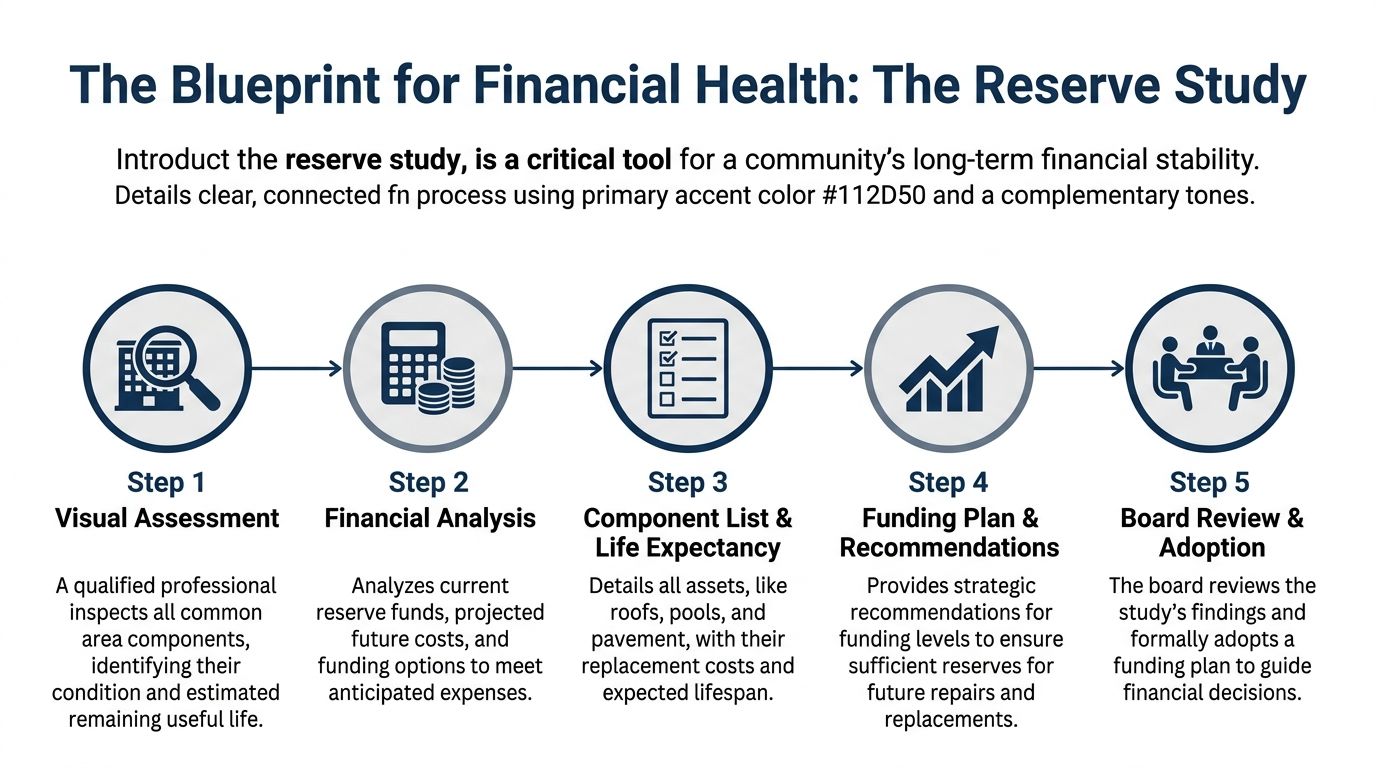

The Blueprint for Financial Health The Reserve Study

A reserve study is the board’s planning blueprint. Without it, reserve decisions often become guesswork, and guesswork is a weak defense when owners ask why dues are changing or why the association fell short.

A proper reserve study tells the board what it owns, how those assets are aging, what replacement or major repair may cost, and how the association can fund those future obligations over time.

What a reserve study actually does

The study combines two kinds of analysis.

Physical analysis

Someone qualified evaluates the common components the association is responsible for. That usually includes items such as roofing, pavement, clubhouse systems, fencing, pool equipment, elevators, or other shared assets.

The goal isn’t just to create a list. The goal is to estimate condition, useful life, and remaining life.

Financial analysis

The second part looks at money. It compares projected future costs with current reserve balances and annual contributions. Then it develops a funding plan the board can use.

That makes the study far more than an engineering snapshot. It becomes a budgeting document and a governance tool.

The Fully Funded Balance matters

One of the most important concepts in reserve planning is the Fully Funded Balance, often shortened to FFB.

The formula is:

FFB = Current Replacement Cost × (Effective Age ÷ Remaining Useful Life)

That formula helps the board understand how much money should theoretically have been accumulated for a component based on wear and use. The health of the reserve fund is often measured against that benchmark, and the Community Associations Institute recommends a reserve study every 3 years to keep that calculation current and reduce underfunding risk, according to First Citizens’ explanation of reserve fund management.

Why boards need regular updates

A reserve study is not something the board orders once and then files away forever.

Costs change. Components age. Storms happen. Materials and labor move. Communities add amenities, defer projects, or discover hidden deterioration. That’s why regular updates matter so much.

For many Georgia boards, the study also creates a defensible paper trail. If owners challenge a dues increase, the board can point to a professional analysis rather than saying, “We thought this felt right.”

If you want a practical overview of what the process involves, this guide to what is an HOA reserve study gives a good board-level summary.

A reserve study gives the board something every good decision needs: a documented basis.

What a sample component schedule can look like

Below is a simple example of how boards should think about component planning. The values are illustrative in structure, and the FFB example follows the formula discussed above.

| Component | Useful Life (Years) | Remaining Life (Years) | Current Replacement Cost | Fully Funded Balance Needed |

|---|---|---|---|---|

| Roof section | 10 | 6 | $10,000 | $4,000 |

| Pool furniture | To be determined by study | To be determined by study | To be determined by study | To be determined by study |

| Asphalt paving | To be determined by study | To be determined by study | To be determined by study | To be determined by study |

| Elevator controls | To be determined by study | To be determined by study | To be determined by study | To be determined by study |

That first row reflects the example tied to the FFB formula. The rest show the categories a real study would complete for your association.

Who should prepare the study

Boards should use qualified professionals with reserve study experience, engineering knowledge, or both. The key point is credibility.

A strong study should include:

- A component inventory: Shared assets the association must maintain, repair, or replace.

- Condition observations: What’s wearing out, what’s stable, and what needs closer monitoring.

- Estimated timing: Remaining useful life for major components.

- Funding recommendations: A practical path for annual reserve contributions.

Questions a Georgia board should ask before adopting it

Not every board discussion needs to be technical. These are the questions that matter most:

- Does the study reflect our governing documents? The board should confirm that only association-responsible components are included.

- Are recent projects incorporated? If the community already replaced or repaired a major asset, the study should reflect that.

- Can we explain the funding plan to owners? If the board can’t explain it in plain language, homeowners won’t trust it.

- Do we need phased changes? Some boards can’t move to ideal funding in one budget cycle, but they still need a clear direction.

The best reserve study doesn’t eliminate hard decisions. It makes those decisions more informed, more consistent, and easier to defend.

Smart Funding Strategies for Your Reserve Account

Once the board has a reserve study, the next question is practical: how aggressively should the community fund the reserve account?

Boards often disagree on the funding approach. One group wants the safest path. Another worries about owner affordability right now. A good board weighs both, but it doesn’t pretend that delaying funding has no cost.

The three main funding approaches

Reserve professionals commonly discuss three broad strategies.

Full funding

This approach aims to keep reserves aligned with deterioration over time. It is the most conservative option and usually the easiest to defend from a fiduciary perspective because it tracks the community’s actual long-term obligations closely.

For many boards, this is the cleanest message to owners: each membership group contributes toward the wear that occurs during its period of ownership.

Threshold funding

This approach targets a defined cushion rather than full parity with deterioration at every moment. It can be a reasonable middle ground when the board wants a meaningful safety margin without aiming for the highest possible reserve level.

Many boards find this attractive because it balances stability and affordability, provided the threshold is grounded in the reserve study.

Baseline funding

This approach aims to keep the reserve cash balance above zero. It’s the leanest strategy and the riskiest. The board may avoid higher dues in the near term, but it also leaves less margin for timing surprises, cost spikes, or component failure earlier than expected.

Comparing the risk side by side

| Funding approach | General board posture | Risk level |

|---|---|---|

| Full funding | Most conservative | Lower |

| Threshold funding | Balanced but still protective | Moderate |

| Baseline funding | Minimal cushion | Higher |

For most communities, boards should lean toward a conservative path. A funding target in the 70% to 100% range is widely treated as healthier than bare-minimum funding in the reserve planning discussion reflected in the verified material above.

Why older assumptions no longer work

Boards can’t rely on stale numbers. Post-2024 inflation and supply chain disruption have made reserve study updates more important, and a 2021 study found that 99.85% of condos needed to allocate more than 10% of their budget to reserves, with the source noting that the needed figure is likely higher now because of rising material and labor costs, as discussed in this CAMS article on insufficient reserve funds.

That has a direct board-level implication. If your contribution policy was built around an old “good enough” number, it may no longer match the actual replacement environment your community faces.

How boards should decide

A smart board doesn’t ask only, “What can owners tolerate this year?”

It also asks:

- What projects are moving closer to replacement?

- How much timing risk can the association reasonably absorb?

- Would a small increase now prevent a much larger owner burden later?

- What message are we sending buyers and lenders about financial stability?

Don’t choose a funding strategy based only on this year’s pressure. Choose one the next board can still defend.

The reserve account investment rule

Reserve money shouldn’t chase high returns. The board’s job is to protect community assets, not to speculate.

A practical reserve investment policy usually rests on three priorities:

Safety

Protect principal first. Reserve dollars are earmarked for future obligations. If the association takes excessive investment risk and loses money, owners absorb the damage.

Liquidity

The board needs access to cash when projects come due. Locking too much money away for too long can create unnecessary strain.

Yield

A reasonable return matters, but only after safety and liquidity are addressed. Earning something on reserve balances is helpful. Taking outsized risk to stretch yield usually isn’t.

A useful way to frame annual contribution decisions

When boards debate reserve contributions, the discussion often becomes emotional. It helps to bring it back to three concrete questions.

- What does the reserve study recommend?

- What would happen if a major project came sooner than expected?

- Would we rather increase dues gradually or rely on abrupt owner charges later?

Those questions usually expose the tradeoff. Underfunding can make this year’s budget look easier, but it often makes the community’s future much harder.

Your Fiduciary Duty and Reserve Funds in Georgia

Many Georgia board members ask a fair question: if state law doesn’t impose a universal reserve requirement on every association, how strong is the board’s obligation to fund reserves?

The answer is still serious. Board members owe a fiduciary duty to act in the best interests of the association. In reserve matters, that means protecting the community’s financial health, preserving common property, and following the governing documents.

Why this matters even without a universal state mandate

Nationally, 72% of HOA reserves are underfunded, and in states such as Georgia, where there is no statutory reserve requirement, responsibility falls heavily on the board’s fiduciary duty and the association’s governing documents. That stands in contrast to California, which mandates triennial reserve studies, according to this overview from FirstService Residential.

For a Georgia board, that means “the law doesn’t specifically force us” is not a safe operating philosophy.

Your governing documents may be more demanding than state law

Covenants, bylaws, declarations, and board-adopted policies often create specific duties around maintenance, budgeting, and common-area care. Even when those documents don’t spell out the exact reserve contribution amount, they usually make the board responsible for preserving the association’s assets.

That’s the practical legal standard many boards overlook.

A board can’t ignore foreseeable obligations

A failing roof, aging private road, or deteriorating pool surface is not a surprise in the legal sense just because the exact invoice date is unknown. These are foreseeable obligations tied to assets the association is obligated to maintain.

When the board chronically postpones reserve funding to avoid unpopular budget decisions, it increases the chance of owner harm.

Where breach of duty concerns can arise

Boards don’t need to become lawyers, but they do need to recognize the warning signs. This plain-language explanation of what constitutes a breach of fiduciary duty can help board members understand the underlying concept.

Common reserve-related risk points include:

- Ignoring professional advice: Ordering a reserve study and then disregarding it without a sound reason.

- Failing to follow governing documents: Budgeting in a way that conflicts with maintenance obligations.

- Using poor records: Making major funding decisions with no documented rationale.

- Treating reserve money casually: Weak controls can undermine trust and expose the board to challenge.

What good governance looks like

A strong board doesn’t promise homeowners that dues will never rise. It promises to make informed, documented, fair decisions.

That usually includes:

- Reading the documents carefully: Confirm what the association must maintain and how funds are to be handled.

- Using current professional data: Base funding decisions on an updated reserve study, not assumptions.

- Recording the rationale: Board minutes should show why funding decisions were made.

- Communicating with owners early: Owners react better to planned changes than emergency announcements.

If you want a more focused discussion of condominium-specific expectations, this resource on condo reserve fund requirements is a helpful reference point.

The board’s duty is not to make every budget popular. It is to make the budget responsible.

For new board members, that mindset matters. Reserve funding is one of the clearest places where short-term politics and long-term stewardship collide. Your job is to keep the community from paying a far higher price later for a decision that felt easier today.

How to Talk to Homeowners About Reserve Funding

Many boards get the math right and the message wrong.

Homeowners don’t live inside reserve studies, depreciation schedules, or funding models. They live with monthly assessments, household budgets, and concern about whether the board is spending wisely. If you want owner support, you have to explain reserve funding in language that connects to their daily reality.

Start with purpose, not jargon

Most owners don’t need a technical lecture first. They need a simple answer to one question: why are we putting money into this account?

A good opening sounds like this:

Reserve funding helps the association repair and replace major shared assets without forcing owners into sudden large charges.

That message is easier to understand than a discussion about funding percentages alone.

Three communication habits that work

Show people what reserves pay for

Be concrete. Name the common elements involved. Roofs, pavement, gate systems, elevators, pool equipment, siding, retaining walls, or clubhouse systems are easier to understand than “future capital expenditures.”

Connect reserve funding to owner outcomes

Owners care about predictability, property condition, and resale strength. Tie your message to those concerns.

Repeat the message all year

Don’t wait for the annual meeting. Reserve education works better when it appears in budget notes, newsletters, owner portals, and meeting packets.

Helpful phrases for difficult conversations

When boards expect resistance, they often become defensive. That usually backfires. Calm, direct language works better.

Try language like:

- On dues increases: “This adjustment is tied to long-term repair planning, so the community can meet known obligations responsibly.”

- On reserve contributions: “We’re collecting gradually now so owners aren’t hit with abrupt charges later.”

- On fairness: “Regular contributions spread the cost of wear over time instead of shifting it to whichever owners happen to be here when a project comes due.”

What not to say

Some board phrases create immediate mistrust.

Avoid statements like:

- “We probably won’t need it.” Owners hear uncertainty.

- “The management company told us to do it.” The board must own the decision.

- “This is just how associations work.” That sounds dismissive.

- “We can deal with it later.” Owners hear risk, not reassurance.

Use visuals and plain summaries

A board packet can include the full financial detail, but homeowner communication should also include a short summary.

A useful owner-facing reserve update can include:

| Topic | Plain-language explanation |

|---|---|

| What the reserve fund is for | Major shared repairs and replacements |

| Why contributions are changing | To keep pace with aging components and projected costs |

| What owners should expect | More predictable planning and fewer financial surprises |

| What the board is doing | Following a study, reviewing funding annually, and communicating openly |

A script for the board president or treasurer

If you need a short meeting statement, keep it simple:

“We’re not increasing reserve contributions because something went wrong. We’re increasing them because major components wear out on a schedule, and the board’s job is to prepare before that becomes an emergency.”

That kind of statement tends to lower tension because it frames the issue as stewardship, not panic.

The communication goal

The goal isn’t to make every owner happy. That won’t happen.

The goal is to make the board’s reasoning understandable, consistent, and credible. When homeowners can see that reserve and reserve fund decisions are tied to property protection and fairness over time, they’re more likely to accept the plan even if they don’t love the increase.

Your Reserve Fund Questions Answered

Can the board borrow from the reserve fund to cover an operating shortfall?

Boards should be very cautious. Reserve money exists for major future repair and replacement obligations, not for ordinary budget problems.

If the board pulls from reserves, it risks weakening the community’s ability to pay for planned capital work later. In some communities, governing documents or adopted policies may also restrict that move. Before taking any such step, the board should review its documents, get accounting guidance, and create a documented repayment plan if the action is legally permitted.

Should we use a special assessment or raise dues?

That depends on the situation, but boards should understand the tradeoff.

A special assessment can address an immediate gap quickly. It may be necessary in a true funding crisis. But it also places a sudden burden on owners and can create hardship, conflict, and collection issues.

Raising dues to strengthen reserves is usually the steadier long-term method because it builds predictability into the budget. Many boards end up using a combination. They address an urgent need while also changing ongoing contributions so the same problem doesn’t repeat.

The best answer is often not choosing one tool forever. It’s matching the tool to the problem and fixing the underlying funding pattern.

Does a low reserve fund affect sales and financing?

Yes, it can.

Buyers, lenders, and real estate professionals often look closely at the association’s financial condition. If reserves appear weak, buyers may worry about deferred maintenance or future assessments. Lenders may also scrutinize the association more carefully. Even when a sale still goes through, low reserves can make the community look less stable and less attractive.

What should the board do first if reserves are severely underfunded?

Start with facts, not panic.

Order or update a professional reserve study if the current one is outdated or missing. Then compare the findings against current reserve balances, likely project timing, and the association’s governing documents.

After that, the board should prioritize:

- Immediate life-safety or property-preservation issues

- A written funding recovery plan

- Clear homeowner communication

- A realistic budget adjustment path

The board doesn’t have to solve the entire problem in a single meeting. It does need to stop the drift and adopt a credible plan.

How often should the board revisit reserve decisions?

At minimum, reserve funding should be part of the annual budget process, and the board should also revisit it when major project timing changes, costs rise sharply, or the association experiences unexpected damage.

Reserve planning works best when it’s treated as an ongoing governance responsibility, not a once-every-few-years event that gets attention only when cash is tight.

If your board wants experienced guidance on reserve planning, budgeting, owner communication, and day-to-day community management, Access Management Group can help. Their team has served Georgia associations for decades with a focus on protecting homeowners, supporting boards, and preserving community property values through informed, professional management.