When we talk about accounting for homeowners associations, we’re not just talking about balancing a checkbook. We’re talking about protecting the value of your home and securing the financial future of your entire community. As a homeowner, understanding your HOA's finances is key. For board members, it is the bedrock that keeps property values strong, prevents surprise costs for residents, and builds a transparent, thriving neighborhood.

The Foundation of a Thriving Community

Your community's finances are a lot like the foundation of a house. You don't see it every day, but its strength is what holds up everything else. Proper HOA accounting is that foundation. When it's handled with care, it directly protects every homeowner's investment and makes for a secure, well-maintained place for everyone to live.

This isn't just about reacting to bills as they come in. Proactive financial management, led by the board, is what stops those dreaded special assessments that can hit a family's budget hard. It also reduces legal risks for the board and, just as importantly, builds trust between the association’s leadership and the residents. This is more than numbers on a page; it’s the board's blueprint for creating a community that flourishes for the benefit of all homeowners.

More Than Just Bookkeeping

The sheer scale of community associations puts this responsibility into perspective. In a recent year, homes in HOAs across the U.S. had a combined value of $5.88 trillion, and those associations collected $90 billion in assessments. It’s a fact that homes in well-managed HOAs often sell for 5-6% more than similar homes elsewhere, which shows just how much solid financial practices matter to every homeowner.

This is why accrual-basis accounting is so critical for board members. It’s a method that gives you a true, real-time snapshot of your HOA's financial health by logging income when it's earned and expenses when they're incurred, not just when cash changes hands. This provides a more accurate picture for both the board and the homeowners.

Diligent financial oversight is a core component of your board's fiduciary duty. It is the most powerful tool you have to protect, preserve, and enhance the real estate investments of every single member of your association.

A Roadmap for Success

This guide is built to give HOA presidents and board members the confidence to handle their financial duties effectively, which in turn benefits every homeowner. We’ll walk through everything you need to know, from making sense of financial statements to building a strong, forward-thinking budget. A great starting point for any board member is getting a firm grasp of your HOA board responsibilities.

By mastering these fundamentals, you’ll ensure your community is on solid financial ground, ready for planned projects and whatever unexpected challenges come your way. This turns accounting from a chore into a strategic tool for building a better neighborhood for everyone.

How to Read Your HOA Financial Statements

Think of your HOA’s financial statements as the community's annual check-up. As a board member—or even an engaged homeowner—learning to read them isn't just a good idea; it's a fundamental part of protecting the community’s assets and your own home's value. You wouldn’t ignore a report from your doctor, and you shouldn't ignore your HOA’s financials.

These documents are the bedrock of accounting for homeowners associations, offering the transparency every healthy community needs. With thousands of new HOAs expected to form by 2026 and average monthly fees already hitting $259, getting the numbers right is non-negotiable for the board. Get it wrong, and communities can get hit with surprise special assessments, often ranging from $2,000 to $5,000, not to mention potential fines and board liability. You can find a detailed overview of why these statements are so critical here.

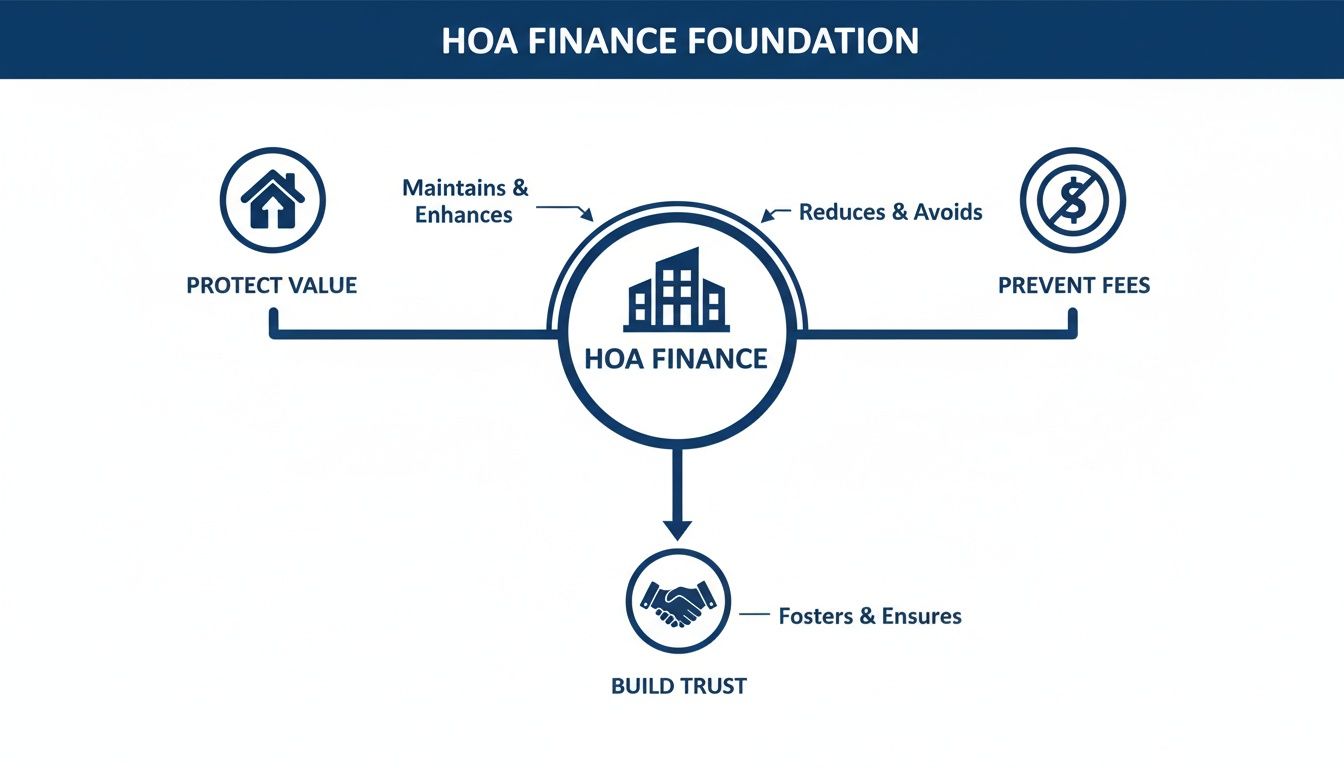

The diagram below really drives home how sound financial management protects your investment, helps avoid those dreaded extra fees for homeowners, and builds trust across the neighborhood.

As you can see, every financial decision has a ripple effect, touching everything from property values to homeowner satisfaction. This is why clear, understandable reporting is so important for building trust between the board and the residents.

To truly get a handle on your HOA's finances, you need to be familiar with three core reports. We've put together a quick guide to help you, as a board member or homeowner, understand what each one tells you and what questions it answers.

A Quick Guide to Your HOA Financial Reports

Understand the purpose of each key financial statement and the critical questions it helps your board answer for the good of the community.

| Financial Statement | What It Shows | Key Question It Answers for the Board |

|---|---|---|

| Balance Sheet | A snapshot of the HOA’s financial health at a specific moment in time (assets, liabilities, and equity). | What do we own, what do we owe, and what's our community's net worth right now? |

| Income Statement | Financial performance over a period of time, comparing income (revenue) against expenses. | Are we sticking to our budget and operating in a way that benefits homeowners? |

| Statement of Cash Flows | The actual movement of cash in and out of the association's bank accounts. | Where did our community's cash come from, and where did it actually go? |

Let's break down what you're looking at in each of these essential documents.

Demystifying the Balance Sheet

First up is the Balance Sheet, which gives you a snapshot of your community's financial position on a specific date, like the last day of the month. It’s a lot like a personal net worth statement for the entire association. At its core, it answers one simple question for homeowners and the board: "What do we own, what do we owe, and what’s left over?"

It’s broken down into three key parts:

- Assets: This is everything the HOA owns that has value. Think cash in the bank, any money owed by homeowners (Assessments Receivable), and physical property like the clubhouse or pool.

- Liabilities: This is what the HOA owes to others. Common examples include unpaid vendor invoices (Accounts Payable), assessments that homeowners paid in advance, and any outstanding loans.

- Equity (or Fund Balance): This is the association's net worth. You get this number by subtracting total liabilities from total assets. It represents all the funds the HOA has, split between operating and reserve funds.

When you see a Balance Sheet where assets are comfortably higher than liabilities, that's a great sign of financial stability that should give every homeowner confidence.

A strong Balance Sheet provides confidence to homeowners, potential buyers, and lenders. It proves the association is managing its resources responsibly and has the funds to meet its obligations, both today and in the future.

Unpacking the Income Statement

If the Balance Sheet is a photo, the Income Statement (sometimes called the Statement of Revenue and Expenses) is a video. It shows your HOA’s financial activity over a period of time—usually a month, a quarter, or the full year. It’s the business equivalent of a household budget, tracking money coming in versus money going out.

This statement is all about answering the question, "Is the board staying on budget?" You'll see line items for:

- Revenue: This is mostly homeowner assessments, but it could also include things like late fees, interest income, or fees from renting out the clubhouse.

- Expenses: This covers all the costs of running the community—landscaping, utilities, insurance, pool maintenance, and management fees, just to name a few.

By comparing the actual numbers to what you budgeted, the board can catch problems early. Are landscaping costs running way over? Is assessment revenue falling short of projections? This report is the board's number one tool for controlling costs and making sure the year ends on solid ground for the benefit of all homeowners.

Following the Money with the Statement of Cash Flows

The third piece of the puzzle is the Statement of Cash Flows. This report ties everything together by showing how the numbers on the Income Statement translate to actual cash in your bank accounts. An Income Statement might show revenue that hasn't actually been collected yet (if you're using accrual accounting), but the Statement of Cash Flows only cares about money that has physically moved.

It answers the crucial question, "Where did our cash come from, and where did it go?" This is incredibly useful for tracking the health of your reserve funds and making sure you have enough liquid cash on hand to pay the bills. It closes the loop between reported profit and your bank balance, giving the board and homeowners a final layer of clarity and accountability.

Building Your HOA Budget and Reserve Fund

Any successful community runs on a solid financial plan, not guesswork. For board members, two of the most critical parts of HOA accounting are crafting the annual budget and maintaining a healthy reserve fund. These aren't separate tasks; they work together to keep your community running smoothly today while preparing it for the big-ticket items of tomorrow—ultimately protecting homeowners from unexpected financial burdens.

Think of your annual budget as your HOA’s financial roadmap for the year. It lays out all expected income (mostly from homeowner assessments) and maps out all your operating expenses—everything from landscaping and pool service to insurance and management fees. A strong budget isn't just pulled from thin air. It’s built by digging into past spending and getting a realistic handle on future costs. Having a firm grasp of core financial principles like budgeting and forecasting is essential for a board to make sure no detail gets missed.

Taking this proactive approach lets your board set assessment levels that are both fair and accurate for homeowners. It ensures you have the cash flow you need to cover all the day-to-day operations without a single hiccup.

Crafting a Realistic Annual Budget

Putting together the budget should be a meticulous, data-driven process, and it’s a task the board, especially the treasurer, needs to own for the good of the community. The goal is to create what’s essentially a zero-based budget, where every dollar of projected income is assigned to a specific projected expense. No slush funds, no ambiguity. This transparency benefits everyone.

Here’s a straightforward way for a board to build the budget:

- Look Back Before You Look Forward: Start by poring over the last year's financial statements. Where were you over budget? Where were you under? More importantly, why?

- Get Fresh Quotes: Don't just assume your costs will be the same. Be proactive and get updated quotes from all your key vendors—landscapers, pool companies, and especially your insurance provider. Insurance costs, in particular, have been climbing.

- Account for Inflation: The cost of goods and services goes up. A budget that doesn't build in an adjustment for inflation is already behind before the year even starts, which could lead to shortfalls affecting the community.

- Pay Your Reserves First: Your budget absolutely must include a line item for your annual reserve fund contribution. This isn't an optional "nice-to-have"; it's a non-negotiable expense for your community's long-term health and the protection of homeowners' investments.

Once the draft budget is ready, it needs to be clearly communicated to homeowners and formally approved based on the rules in your governing documents. That kind of transparency is what builds trust and shows homeowners their money is being managed with care.

The Reserve Fund: Your Community’s Safety Net

While the operating budget handles the daily and monthly bills, the reserve fund is your community’s dedicated savings account for major repairs and replacements. This is the money you set aside for those predictable, large-scale projects that are definitely coming down the line—like replacing the clubhouse roof, repaving the streets, or overhauling the elevator.

A healthy reserve fund is the single best tool a board has for preventing financial crises and avoiding large, deeply unpopular special assessments for homeowners. It’s the hallmark of responsible, forward-thinking leadership.

Failing to properly fund your reserves is one of the worst financial mistakes an HOA board can make. It just kicks a very expensive can down the road, leaving a future board—and future homeowners—to deal with a massive bill they are completely unprepared for.

The Power of a Professional Reserve Study

So, how does the board figure out exactly how much you need to be saving for the community? The answer is a Reserve Study. This is a detailed report, prepared by an independent engineering or financial expert, that does two key things:

- Creates a Component List: It identifies all the major common-area assets the association is responsible for—the roofs, roads, pools, fences, etc.

- Creates a Funding Plan: It estimates the remaining useful life and the future replacement cost for each of those assets. From there, it calculates an annual funding amount needed to cover those costs when they come due.

Most industry experts recommend getting a full, professional Reserve Study done every 3-5 years, with the board doing a quick review and update each year in between. This study is your board’s best defense against ugly financial surprises. It gives you an objective, data-backed plan that justifies reserve contributions to homeowners and protects the board from any claims of mismanagement. Using dedicated community association management software can also make it much easier for boards to track and manage these complex funding plans with real accuracy, ensuring the community's assets are protected.

Managing Delinquencies and Collections with Fairness

Uncollected dues are more than just numbers on a report. They're a real problem that directly impacts your community’s budget and, therefore, every homeowner. When even a handful of homeowners fall behind, it can mean that promised repairs get delayed, landscaping projects are put on hold, or the pool has to close early. It’s a sensitive part of accounting for homeowners associations, and the board needs a process that is firm, fair, and, most importantly, legal.

The point isn’t to punish anyone. It's about making sure the association has the money it needs to run as promised for all residents. A solid collections process actually protects the homeowners who do pay on time. It ensures the financial load is shared equally, just like the community’s amenities are.

Establishing a Clear and Consistent Collections Policy

A board's best defense is a formal, written collections policy. This isn’t some document you file away; it needs to be officially adopted by the board and then given to every single homeowner. When people know the rules from the moment they move in, there's less room for confusion or arguments down the road.

A good policy is all about clarity, not surprises. It should spell out the entire process for homeowners, leaving no stone unturned:

- Due Dates: The exact day assessments are due.

- Grace Period: Any buffer the board allows before a payment is officially late.

- Late Fees and Interest: The specific fees and interest charged on overdue accounts, which must comply with your governing documents and state law.

- Timeline for Action: A step-by-step calendar of what happens once an account is delinquent, from the first notice to potential legal steps.

Above all, the board must be consistent. Applying the policy the same way for everyone is non-negotiable. It’s your best protection against claims of favoritism or discrimination, which can land the board in serious legal trouble and erode homeowner trust.

Implementing a Graduated Collections Process

A fair process doesn't go from zero to one hundred. Instead, it uses a series of escalating steps designed to solve the problem as early and amicably as possible. It's a more neighborly—and frankly, more effective—way for a board to handle things, which benefits the entire community.

Think of it as a series of increasingly serious communications:

- Friendly Reminder: The first step is often a simple, automated reminder sent right after a payment is missed. This catches honest mistakes without creating conflict between neighbors.

- Formal Notice of Delinquency: If the payment still isn't made, the next step is a more official letter. This notice should clearly state the total amount owed, including any late fees, and directly reference the association's collections policy.

- Final Demand Letter: Before things get legal, a final demand letter is sent, usually from the association’s attorney. This letter makes the serious consequences clear, including the possibility of a lien on the property or foreclosure.

- Legal Action: Only as a last resort should the board authorize its attorney to take legal action. This could mean placing a lien on the property to secure the debt against the home's title or, in the most severe cases, starting foreclosure proceedings.

A graduated collections process shows the board is acting in good faith. It gives homeowners multiple chances to get their account in good standing while proving the board is fulfilling its fiduciary duty to collect all money owed to the association.

This measured approach protects the community's finances while still treating homeowners with respect.

The Role of Professional Management in Collections

For volunteer board members, chasing down payments is often the worst part of the job. Having to confront your neighbors about money is awkward and can create a lot of bad blood in the community. This is one of the biggest reasons for a board to hire a professional management company.

An experienced manager acts as a neutral third party, benefiting both the board and homeowners. They take the personalities out of it, making sure every step follows the policy and complies with state law. They handle the notices, keep track of all communication, and can de-escalate conflicts before they blow up, which helps keep the peace in the neighborhood. This frees the board from those tough conversations and lets you focus on the bigger picture of building a better community for everyone.

Ensuring Compliance Through Audits and Internal Controls

Protecting your community's assets is about more than just building a solid budget. Real financial integrity in accounting for homeowners associations comes from having a combination of strong internal security and independent oversight. This is how your board demonstrates its commitment to its fiduciary duty, giving homeowners—and yourselves—true peace of mind.

Think of it like this: internal controls are the locks on the doors, and an audit is the independent security company that comes to check them. You absolutely need both. They work together to prevent honest mistakes and, frankly, to deter anyone tempted to commit fraud, ensuring homeowner funds are safe.

These layers of protection show your HOA’s finances are managed responsibly, which is the bedrock of building trust within your community.

Audits, Reviews, and Compilations Explained

The word "audit" gets thrown around a lot, but it's not a one-size-fits-all term. There are actually three distinct levels of financial review. Knowing the difference helps your board choose the right one based on your governing documents, state laws, and what the community really needs to ensure transparency for homeowners.

Compilation: This is the most basic service. A CPA takes the financial data you provide and simply organizes it into the proper financial statement format. They aren't verifying the numbers, just presenting them correctly. There is no assurance of accuracy.

Review: This is a step up. The CPA will look at the numbers and perform some analysis to see if they make logical sense. They’re looking for red flags or obvious errors, but not digging deep to verify individual transactions. This provides limited assurance to the board and homeowners that the financials are sound.

Audit: This is the deep dive. An independent CPA thoroughly examines the association's financial records. They’ll do things like verify bank balances, test your internal controls, and confirm transactions with outside parties. An audit offers the highest level of assurance that the financials are accurate and free of major errors, providing maximum transparency.

A huge part of this process is being prepared. Knowing how to prepare for an audit makes everything smoother and far more effective for the board and the auditor.

Key Internal Controls Every HOA Needs

Internal controls aren't just accounting jargon; they are the specific rules and procedures you put in place to guard the community’s money. They are your board's first and best line of defense against both simple mistakes and intentional misconduct, protecting homeowner funds.

Internal controls are not about a lack of trust; they are about a commitment to good governance. They protect the volunteers who serve on the board just as much as they protect the community’s assets and homeowners' investments.

Here are a few non-negotiable controls every single HOA board should have:

- Dual Signatures on Checks: Require two board members to sign any check over a set amount (say, $500). This simple step prevents any one person from spending large sums of the association’s money on their own.

- Separation of Duties: The person who approves invoices should never be the same person who signs the checks. Likewise, the person making bank deposits shouldn’t be the one reconciling the bank statements. This makes it much harder for discrepancies to go unnoticed.

- Regular Bank Reconciliation Reviews: Every month, a board member who is not a check-signer (the treasurer or president is a good choice) should review the full, reconciled bank statements to spot any unusual activity.

- Secure Invoice Approval Process: Create a clear, documented process for approving vendor invoices before they get paid. This ensures you’re only paying for work that was actually authorized and completed to the community's satisfaction.

Understanding HOA Tax Obligations

Yes, your HOA almost certainly has to file tax returns. While most HOAs are registered as non-profit organizations, that status doesn't automatically make them tax-exempt in the eyes of the IRS.

Most HOAs file one of two federal tax forms, and the choice between them can have a major impact on your association's tax bill. This isn’t a decision for a board to take lightly. It’s best made with guidance from a CPA who specializes in community association accounting to ensure you remain compliant and avoid any costly penalties that could impact homeowner funds.

Self Management vs Professional HOA Accounting

Sooner or later, every board faces a big question: who’s going to handle the money? It's a decision that goes right to the heart of your community's financial stability, legal standing, and even the sanity of your volunteer leaders. The choice boils down to handling it all in-house or partnering with a professional firm. This decision directly impacts every homeowner.

It’s easy to see the appeal of self-management, especially for newer or smaller associations trying to keep costs down. A well-intentioned volunteer treasurer, maybe someone with a little bookkeeping experience, steps up to manage the finances. While it seems like a great way to save on management fees, this path is loaded with risks that boards need to weigh carefully for the good of the community.

The Risks of Self Management

Let's be clear: accounting for homeowners associations is a world away from balancing a personal checkbook. The learning curve is steep, the time commitment is massive, and it requires a solid grasp of specific state laws and your own governing documents.

For volunteer-run boards, the challenges pile up quickly, often to the detriment of homeowners:

- Time and Burnout: The treasurer role is notoriously one of the toughest to fill—and keep filled. The sheer volume of work, from bookkeeping and collections to generating reports for the board and homeowners, leads to fast burnout, even for the most dedicated volunteers.

- Compliance Errors: HOA accounting is wrapped in red tape. A volunteer, no matter how careful, can easily make a mistake in financial reporting, reserve fund calculations, or tax filings. These errors can lead to hefty fines and put the entire board at legal risk, potentially costing all homeowners.

- Lack of Internal Controls: Without a professional set of eyes, it’s all too easy for a board to overlook crucial internal controls like the separation of duties. This opens the door to both honest mistakes and, in the worst cases, potential fraud that harms the entire community.

For a volunteer board, the perceived savings of self-management can be quickly wiped out by a single compliance mistake, an uncollected delinquency, or a poorly managed reserve fund. It shifts a significant burden onto untrained neighbors and puts homeowner investments at risk.

The Value of Professional Management

Bringing in a professional management firm isn’t just about outsourcing bookkeeping. It’s about the board gaining a strategic financial partner who brings expertise, established processes, and specialized tools to your community. This isn’t just another line-item expense; it's an investment in your HOA’s long-term stability and the board’s peace of mind, which directly benefits every homeowner.

A professional partner takes on the daily financial grind. They manage vendor payments, process assessments, and—critically—handle the often uncomfortable task of collections with a firm but fair and consistent approach. This frees up the board to step back from the weeds and focus on big-picture governance that improves the community for everyone.

To give you a clearer picture, let's compare how these two approaches stack up side-by-side for common accounting duties.

A Comparison of HOA Accounting Management

| Accounting Task | Self-Managed Approach (Volunteer Board) | Professional Management Approach |

|---|---|---|

| Assessment Collection | Volunteer treasurer manually tracks and deposits payments, often dealing with late-paying neighbors directly. | Automated system handles billing, online payments for homeowners, and lockbox services. Firm handles follow-ups professionally. |

| Delinquency & Collections | Uncomfortable process managed by a neighbor. Inconsistent application of late fees and lien processes. | A defined, legally-compliant process is followed for every delinquency, protecting the association's and homeowners' interests. |

| Financial Reporting | Reports may be infrequent, inconsistent, or lack the necessary detail for true financial oversight by the board or homeowners. | Monthly delivery of accurate, easy-to-understand financial statements (Balance Sheet, Income Statement, etc.) for full transparency. |

| Internal Controls | High risk of error or fraud, as one person may handle billing, collections, and bank reconciliations. | Strict separation of duties. Multiple people and system checks are in place to prevent errors and misappropriation of homeowner funds. |

| Software & Tools | Often reliant on basic software like QuickBooks, which is not designed for the complexities of fund accounting. | Access to enterprise-level software designed specifically for HOA management, ensuring compliance and transparency for homeowners. |

| Board Member Time | The treasurer and board spend significant time on day-to-day financial tasks and troubleshooting, taking focus away from community improvement. | The board's time is freed to focus on strategic decisions, community projects, and long-term planning for the benefit of all residents. |

As you can see, the differences are stark. A management company’s value extends far beyond simply writing checks.

A good firm provides access to the best HOA accounting software, tools that most self-managed boards simply can't afford or operate effectively. These systems automate tedious work, guarantee accuracy, and offer the transparency that homeowners rightfully expect.

Ultimately, a management firm brings a team of experts who are constantly tracking changes in HOA law, ensuring your association stays compliant and protected. By offloading these complex responsibilities, the board is empowered to do its real job: protecting and enhancing the value of the community for everyone.

Common Questions About HOA Accounting

As a board member, you’re bound to have questions about the financial side of running your community. We get it. Financial jargon can feel overwhelming, but a solid grasp of the basics is crucial for building a transparent and financially healthy association that serves its homeowners well.

To help you feel more confident in your role, we've put together some of the most common questions we hear from boards and homeowners, along with straightforward answers from our team of experts.

What Is the Difference Between Accrual and Cash Basis Accounting?

This is a big one, and it gets to the heart of how you see your community’s finances. It's a bit like tracking your personal budget.

- Cash basis accounting is the simpler of the two. It records income only when cash hits the bank, and expenses only when the money is paid out. It’s a real-time snapshot of your bank balance.

- Accrual basis accounting is more sophisticated. It records income when it's earned (like when assessments are officially due for the month) and expenses when they're incurred (when a vendor finishes a job), no matter when the actual cash moves.

For HOAs, accrual accounting is the undisputed industry standard for a reason. It provides a much more honest and complete picture of the association's financial health for both the board and the homeowners, showing you the money you're owed and the bills you have to pay—not just the cash in your account today.

How Often Should Our HOA Conduct a Reserve Study?

Think of a reserve study as your community’s long-term financial roadmap. It plans for the eventual repair or replacement of major assets like roofs, paving, and pools. Ignoring this is one of the biggest risks a board can take on behalf of its homeowners.

Most experts, and many state laws, recommend a full, professional reserve study be conducted every 3-5 years. In the years between, the board should review it annually to ensure the funding plan is still on track with current costs.

This proactive approach is the single best way for a board to avoid hitting homeowners with large, unpopular special assessments. It’s a hallmark of responsible and forward-thinking leadership that protects everyone's investment.

Can Board Members Be Held Personally Liable for Financial Mismanagement?

Yes, absolutely. This is a very real risk that every board member needs to understand. When you join the board, you take on a fiduciary duty to act in the best financial interest of the association and all its homeowners.

If a board acts with gross negligence—or knowingly ignores its governing documents and state laws—members can potentially be held personally liable for the financial fallout. This is precisely why following best practices, maintaining strong internal controls, and carrying adequate Directors & Officers (D&O) insurance is non-negotiable. Partnering with an experienced management firm adds another critical layer of protection for these volunteer leaders.

Why Do Our HOA Fees Seem to Go Up Every Year?

This is a question every board faces from homeowners. The answer is usually quite simple: inflation and rising costs. Everything required to maintain the community—from insurance and landscaping to utilities and pool chemicals—gets more expensive over time.

A well-run HOA board anticipates these increases in its annual budget. A modest, planned annual increase is far healthier for the community than keeping fees artificially flat for years. The alternative is a sudden, massive fee hike or a special assessment to cover a shortfall, which is never popular and signals poor financial planning by the board that ultimately harms homeowners.

Answering these questions and confidently managing your HOA’s finances takes expertise and dedication. At Access Management Group, we partner with associations to provide that professional oversight, protecting and enhancing the value of your community for every homeowner. Find out how our state-of-the-art tools and experienced managers can bring stability and peace of mind to your board at https://accessmgt.com.