Your first HOA statement arrives. The amount isn’t shocking by itself. What unsettles most owners is the uncertainty behind it.

What does HOA cover, exactly? Lawn care? Roofs? Pool repairs? Insurance? Legal fees? A future paving project? And if something goes wrong inside your home, where does the association’s responsibility stop and yours begin?

That confusion is normal. New homeowners ask because they don’t want surprise costs. Board members ask because they don’t want preventable disputes. Community presidents ask because one vague answer today can turn into a claim, complaint, or special assessment later.

Welcome to the Neighborhood Understanding Your HOA

If you live in an HOA, you’re not in a niche arrangement. In 2025, the United States is home to approximately 373,000 community associations, accommodating 77 million people, or 23% of the U.S. population, and accounting for 33% of all U.S. housing stock. Those communities collect $103.3 billion in assessments and help protect property values exceeding $12.9 trillion, according to 2025 HOA facts and figures.

That scale matters because HOA coverage isn’t just about amenities. It’s about how millions of owners share financial responsibility for property that no one owner can maintain alone.

What coverage really means

In practice, HOA coverage usually includes some mix of these responsibilities:

- Shared property care: Entrances, landscaping, private roads, hallways, roofs, elevators, or building exteriors, depending on the community type.

- Operational support: Lighting, irrigation, cleaning, management, accounting, and vendor coordination.

- Risk protection: Insurance for common property and liability exposures.

- Long-term planning: Reserve funding for major repair and replacement projects.

The exact mix changes dramatically from one association to the next. A single-family neighborhood with a monument sign and detention pond doesn’t operate like a high-rise condominium with elevators, boilers, hallways, and a staffed front desk.

Practical rule: HOA dues aren’t a general warranty for everything near your home. They pay for obligations the association has accepted in its governing documents and budget.

Why owners and boards get this wrong

Most disputes start with assumptions. Owners assume the HOA covers anything “outside.” Boards assume owners understand the documents. Neither assumption is safe.

A better approach is to treat HOA coverage as a boundary question:

- What property is shared

- What costs are communal

- What risks are insured

- What remains the owner’s job

That boundary affects maintenance calls, insurance claims, reserve planning, and resale disclosures. When people understand it early, they make better decisions and avoid expensive misunderstandings.

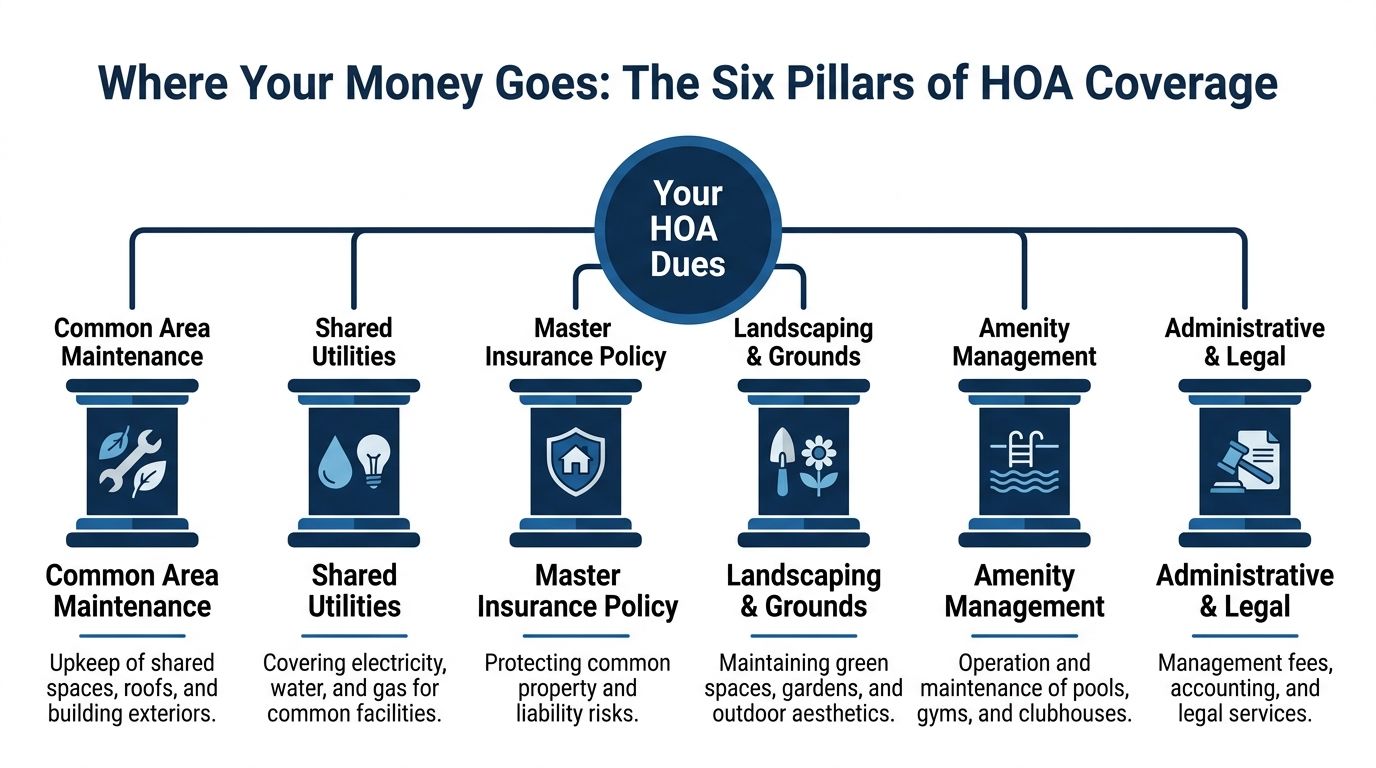

Where Your Money Goes The Six Pillars of HOA Coverage

A budget meeting gets tense fast when the landscaping looks fine, but the roof reserve is short, the master policy deductible has climbed, and a storm claim is still unresolved. That is the point where owners stop asking what dues cover in theory and start asking what the association can pay for without a special assessment.

An HOA budget works like an operating plan for shared property, shared risk, and future repair obligations. Every dollar has a job. If the board underfunds one category, the cost usually shows up somewhere more painful later through emergency repairs, deferred projects, insurance disputes, or sudden owner charges.

Common area maintenance

This is usually the largest and most visible part of HOA spending. It covers the physical care of property the association is obligated to maintain.

In a single-family HOA, that may mean entry features, perimeter fencing, irrigation, ponds, sidewalks, and private streets. In a condominium or townhome community, it can include roofs, siding, exterior painting, hallways, elevators, shared plumbing lines, gate systems, and drainage structures. The legal issue is not whether something is expensive. The issue is whether the governing documents assign that expense to the association.

Boards that hold dues artificially low often cut this category first. That decision rarely stays cheap. Small pavement failures become replacement projects. Minor water intrusion becomes a building envelope claim. Routine work is far less expensive than emergency work.

Shared amenities

Amenities attract buyers, but they also create recurring financial and liability exposure.

A pool requires chemicals, inspections, furniture replacement, deck repairs, access control, and insurance review. A clubhouse adds cleaning, HVAC service, utility bills, and wear from rentals or resident use. Courts, playgrounds, fitness rooms, and walking trails all bring maintenance standards that cannot be ignored once the association owns them.

I often tell boards to evaluate amenities in two ways. First, ask what they cost to run each year. Second, ask what it would cost if someone gets hurt or the equipment fails and the association did not maintain it properly. That second number is why boards need disciplined vendor oversight and written maintenance schedules. Homeowners can use an annual home maintenance checklist as a practical reminder that shared property also needs routine, documented care.

Utilities

Utility costs are less visible than a new gate or fresh mulch, but they can move a budget quickly.

Typical examples include common-area lighting, irrigation water, pool water, restroom service, clubhouse electricity, security systems, and in some buildings, gas or water service that supports multiple units. Utility responsibility also varies by community design. A detached-home HOA may have minimal shared utility expense, while a mid-rise condominium may carry substantial common mechanical and utility costs.

This category creates gray-area disputes when owners assume every bill tied to the building belongs to the association. It does not. The answer depends on how the meters are set up, what the declaration says, and whether the service supports one unit or shared components.

Master insurance policy

Insurance is one of the easiest budget lines to misunderstand. Owners see it in the budget and assume it protects everything connected to their home. In practice, the association’s policy usually protects common property, certain building components, and liability tied to association operations.

That still leaves hard questions. Is the loss below the deductible? Does the damage involve owner improvements? Did a maintenance failure contribute to the claim? In many communities, the fight is not over whether there is insurance. The fight is over which policy responds first and who absorbs the deductible.

Boards should explain this line item plainly in budget meetings and resale materials. Clear explanations reduce claim disputes and help owners buy the right personal coverage instead of finding out after a loss that the master policy stops short of the damage inside the unit.

Reserve funds

Reserves pay for major repair and replacement projects that are predictable even if the exact timing is not. Roofs age. Asphalt cracks. Boilers wear out. Elevators need modernization. Pool surfaces fail.

A budget can look balanced and still be weak if it pays current bills while ignoring those future obligations. That is how communities drift into special assessments. I have seen boards postpone reserve contributions to avoid a dues increase, then face a much larger owner backlash when a major component fails and cash is not there.

Good reserve planning also helps with fairness. Owners should pay their share of the assets they use during their time in the community, rather than passing the full bill to whoever owns there when the component finally breaks.

Management and administration

Administration does not get much attention until it breaks down. Then the consequences spread quickly.

This category covers accounting, collections, financial reporting, contract administration, meeting support, records management, compliance processes, owner communication, and coordination with legal and insurance professionals. Strong administration protects the association from preventable mistakes such as missed renewals, weak collections, incomplete vendor scopes, and poor documentation during disputes. Boards that want a clearer picture of this work should review how HOA accounting services support financial clarity.

What a sound budget looks like

The healthiest HOA budgets usually share a few traits:

- Obligations come before optics. Roofs, drainage, insurance, and pavement usually deserve funding before decorative upgrades.

- Each line item ties to a document, asset, or known risk. If the board cannot explain why a cost belongs in the budget, it needs closer review.

- Reserve contributions are treated as current expenses, not optional savings.

- Owners get plain-language explanations. Fewer disputes start when people understand what dues are buying and what they are not.

The core trade-off is straightforward. Lower dues can feel good for a year or two. Underfunded maintenance, thin reserves, and vague insurance expectations usually cost more later, and they tend to cost more at the worst possible time.

Drawing the Line Where HOA Responsibility Ends and Yours Begins

Most HOA frustration isn’t about the rule itself. It’s about the line. Owners want to know who fixes the issue, who pays, and who needs to act first.

The answer depends less on instinct than on property type and governing documents.

Three categories that matter

Most communities divide responsibility into some version of these buckets:

- Common elements: Property used by everyone, such as roads, hallways, roofs, structural walls, shared mechanical systems, clubhouses, and pools.

- Limited common elements: Property reserved for one owner or a small group, such as balconies, patios, assigned parking spaces, or exterior doors in some communities.

- Unit or lot responsibility: Interior surfaces, fixtures, appliances, finishes, and components that serve only one home.

The gray areas usually sit in the second bucket. A balcony may belong to the association structurally but still require the owner to maintain cleanliness and report damage. A window may be part of the building envelope in one community and the owner’s replacement duty in another.

The line shifts by community type

A detached-home HOA often covers much less than a condominium association. That’s why “what does hoa cover” can’t be answered well without naming the type of community.

| Item | Single-Family Home | Townhome | Condominium |

|---|---|---|---|

| Roof | Usually homeowner | Often HOA, but check documents | Usually HOA |

| Exterior siding or walls | Usually homeowner | Often HOA for exterior envelope | Usually HOA |

| Interior drywall and finishes | Homeowner | Homeowner | Homeowner |

| Hallways and lobbies | Not typically applicable | Sometimes shared | Usually HOA |

| Balcony or patio | Often homeowner, subject to rules | Often limited common element | Often limited common element |

| Main shared plumbing lines | Rare in detached setup | Often HOA if serving multiple homes | Often HOA if serving multiple units |

| Faucet, toilet, or interior fixture | Homeowner | Homeowner | Homeowner |

| Landscaping around individual home | Varies widely | Often mixed | Usually limited or minimal owner scope |

| Amenities like pool or clubhouse | HOA | HOA | HOA |

| Windows and doors | Usually homeowner | Mixed | Mixed, document-driven |

That table reflects typical patterns, not universal rules. The controlling answer is always in the declaration, maintenance chart, insurance language, and any adopted maintenance standards.

Practical examples that cause confusion

A few recurring scenarios make the boundary easier to understand:

Shared pipe versus interior damage

If a plumbing line behind a wall serves multiple units, the association often handles the shared pipe itself. But the damaged flooring, cabinets, or paint inside one unit may still fall to the owner or the owner’s insurer.

Roof leak versus ceiling stain

The association may be responsible for the roof repair. The stained ceiling inside the unit may not be the association’s cost unless the documents or claim outcome say otherwise.

Balcony structure versus balcony use

The framing, slab, or railing may be an HOA duty. Furniture damage, upkeep, or owner-caused wear may stay with the resident.

When a repair touches both common property and private property, don’t ask only “Who caused it?” Ask “Who owns this component?” and “What do the documents say happens next?”

What homeowners should do before a problem gets expensive

Owners save themselves time by keeping a maintenance file with the declaration, rules, insurance summary, and repair contacts. It also helps to use a seasonal reference such as this annual home maintenance checklist so small owner-side issues don’t get mistaken for HOA failures.

If you’re on the board, don’t rely on institutional memory. Pull the governing documents, create a maintenance matrix, and circulate it. Communities can’t enforce or explain responsibilities consistently unless those responsibilities are written clearly. Boards that need a clean starting point should work directly from their HOA governing documents.

The HOA Insurance Safety Net and Its Critical Gaps

A pipe bursts on a Saturday night. By Monday morning, the hallway drywall is open, one unit owner is asking who pays for cabinets, another wants hotel reimbursement, and the board is trying to confirm whether the master policy deductible will hit the association or the owner involved. This is usually the moment everyone learns that HOA insurance is a starting point, not a full reimbursement promise.

What the master policy usually covers

The master policy generally protects the association’s shared property and its liability exposure. In many condominium communities, that means the building shell, roofs, shared walls, common mechanical systems, elevators, lobbies, clubhouses, pools, and other common areas, as outlined by the Insurance Information Institute’s condo insurance overview.

Well-advised boards often carry more than one policy. General liability, directors and officers coverage, fidelity or crime coverage, workers compensation where required, and equipment breakdown coverage each address a different risk. If one of those layers is missing, the gap can turn into either a lawsuit problem or a budget problem.

Bare walls and all-in are claim issues, not technical labels

Boards and owners often hear bare walls and all-in as if they settle the question. They do not.

- Bare walls usually covers the basic structure and common elements, with limited or no coverage for interior finishes inside the unit.

- All-in usually reaches further into original unit components, but policy language and governing documents still control the outcome.

The trade-off is straightforward. Broader master coverage can reduce disputes over original interiors, but it can also increase premiums and shift more claim activity onto the association’s policy. Narrower master coverage may keep the association’s policy simpler, but owners need stronger HO6 coverage and a clear understanding of what they are expected to insure themselves.

Drywall, subfloor, cabinets, countertops, built-ins, and owner upgrades are where arguments start. A board should never assume the insurance agent, manager, and legal counsel all mean the same thing unless the documents and policy schedule line up in writing.

The gap owners discover after the adjuster arrives

Many owners hear “the HOA has insurance” and assume that includes the inside of the unit, temporary living costs, personal property, and every improvement they paid for. It often does not.

The master policy exists to protect the association first. An owner’s HO6 policy is what usually addresses interior finishes that fall on the owner, betterments and improvements, personal belongings, loss assessment exposure, and personal liability. The National Association of Insurance Commissioners explains those owner-side responsibilities in its condominium insurance consumer guide.

One more problem shows up in expensive claims. Deductibles. If the master policy has a large wind, water, or property deductible, someone still has to absorb that cost. In some communities the association pays it. In others, the documents allow the association to charge it back to a unit owner when the loss originates from that unit or is tied to owner negligence. That issue should be settled before a loss, not argued after demolition starts.

Review the certificate of insurance, the declaration, and the deductible allocation language together. A policy summary without the governing documents leaves out the part owners and boards usually end up fighting over.

Where liability disputes turn expensive

Property repairs are only part of the exposure. Liability claims are where the gray areas become legal ones.

A guest slips near the pool after a maintenance vendor missed algae buildup. An owner hosts a party and someone gets hurt on a balcony. Water escapes from a washing machine hose, damages two units, and also affects common hallway finishes. Each event raises separate questions about control, negligence, maintenance duty, and which carrier responds first.

In practice, delays happen for predictable reasons. The association is looking at common-area responsibility. The unit owner is looking at personal coverage. Carriers are sorting out primary versus secondary responsibility. Meanwhile, damaged property sits longer, residents get frustrated, and legal fees can start to rival the repair cost.

Boards can reduce that risk by reviewing claims history every renewal cycle, confirming deductible allocation rules with counsel, and requiring proof of owner HO6 coverage where the documents allow it. Homeowners should confirm loss assessment coverage, interior building coverage, water damage limits, and whether their policy is written to match the community’s master policy structure.

What works in practice

The communities that handle insurance claims well are rarely the ones with no losses. They are the ones that decided key issues before the first claim.

For boards, that means annual insurance review with the broker, manager, and legal counsel in the same conversation. For owners, it means asking a sharper question than “What does the HOA cover?” Ask where the master policy stops, what deductible can be charged back, and which parts of the unit you are expected to insure yourself. Those answers do more to prevent surprise bills and special assessments than any generic insurance summary.

Beyond Monthly Dues Understanding Reserves and Special Assessments

A board meeting can stay calm for months, then one reserve item fails and the tone changes fast. The roof bid comes in higher than expected. The gate operator is no longer serviceable. The pool needs resurfacing before summer. Owners ask the same question every time. Why weren’t the monthly dues enough?

The answer usually sits in the gap between routine budgeting and long-term replacement planning.

Why reserves matter more than many owners realize

Reserve funds are set aside for major repair and replacement of common components. They are not a slush fund for day-to-day shortfalls, and they are not optional if the association wants to avoid sudden financial strain.

In well-managed communities, reserves do more than pay future invoices. They reduce legal friction. They give boards time to bid work properly, sequence projects, and explain costs before owners conclude that mismanagement caused the problem. A reserve balance also protects property values because buyers, lenders, and review attorneys notice when a community has a long list of aging assets and no credible plan to replace them.

Weak reserves create hard choices. The board delays the project and accepts more wear, higher repair costs, and resident complaints. Or the board approves a special assessment and deals with collection problems, owner pushback, and sometimes a challenge over whether the expense should have been anticipated in the regular budget.

Special assessments are usually a warning sign, not just a billing event

Some special assessments are unavoidable. Storm damage, code changes, litigation, and hidden construction defects can force expenses that no reserve study could time perfectly.

But in many associations, a special assessment points to a deeper issue. The board underfunded reserves for years to keep dues artificially low. The reserve study was outdated. A prior board added amenities without adding replacement funding. Industry guidance from the Community Associations Institute on reserve studies and reserve funding reflects the same practical reality. Communities that ignore long-term capital costs eventually collect them under pressure.

That pressure is expensive. Emergency projects often attract fewer bids, less favorable contract terms, and more owner resistance. If enough owners cannot pay on time, the association may need to borrow, defer other work, or increase collections activity. By then, the financial issue has become a governance issue.

What boards should do

Boards that want to reduce the risk of special assessments should focus on four habits.

- Use the reserve study as a working document: Compare it against current site conditions, vendor input, inflation, and any components the study may have missed.

- Match funding to actual obligations: Roads, private drainage systems, elevators, roofs, siding, retaining walls, clubhouse systems, and security gates all need a realistic replacement path.

- Explain the trade-offs clearly: Owners may not like dues increases, but they usually dislike sudden five-figure assessments even more.

- Separate repairs from upgrades: Replacing a worn component is one decision. Adding a better finish, new amenity, or expanded scope is another, and it should include a plan for future maintenance and replacement.

One caution from practice. Boards sometimes postpone dues increases because the reserve account still looks healthy on paper. That can be misleading if the next two major projects are close together or recent cost escalation has made the study stale.

What homeowners should review before buying or before voting

Owners do not need an accounting background to spot risk. They need the right documents and the discipline to read them.

Request these items:

- The current operating budget

- The latest reserve study

- Recent board meeting minutes

- Any notice of pending capital projects

- The association’s assessment and collection policy

- Information on existing loans or prior special assessments

Those records help answer the questions that matter in the gray areas. Is the community saving enough for known replacements? Has the board been discussing deferred maintenance for months without acting? Are dues low because the association is efficient, or because the board has been postponing unpopular decisions?

Large projects go better when owners hear about the cost, timing, and funding options before the work becomes urgent.

A healthy reserve position gives the board room to make better choices. It also gives owners fewer unpleasant surprises. In my experience, communities avoid the worst conflicts when they are honest early about aging assets, realistic about funding, and disciplined enough to treat reserves as part of property protection, not just accounting.

Your Definitive Guide to Verifying HOA Coverage

When owners ask what their HOA covers, the correct answer isn’t “usually.” It’s “let’s read the documents.”

That’s where coverage becomes specific, enforceable, and much easier to manage.

Start with the declaration

The declaration, often called the CC&Rs, usually carries the heaviest weight on maintenance boundaries and property definitions.

Look for language that identifies:

- Common elements

- Limited common elements

- Unit or lot boundaries

- Maintenance duties

- Repair and replacement obligations

- Insurance requirements

- Damage and casualty procedures

If your community has diagrams or exhibits, review those too. Many disputes happen because people read the text and skip the definitions.

Then review the bylaws

Bylaws often answer the operational questions that the declaration doesn’t spell out in detail.

Focus on:

- Board authority to maintain and repair

- Budget approval and assessment procedures

- Owner notice requirements

- Insurance oversight responsibilities

- Rules for entering units in emergencies

The bylaws won’t always define every component, but they often explain who has authority to act and how decisions get made.

Don’t ignore the rules and policies

Rules and regulations, maintenance standards, architectural guidelines, and board-adopted resolutions can fill in practical details.

You may find guidance on:

- Window and door standards

- Balcony and patio use

- Owner maintenance expectations

- Reporting procedures for leaks or damage

- Insurance certificate requirements

- Vendor access and scheduling

If the board has adopted a maintenance responsibility chart, keep a copy. It’s often the most useful day-to-day reference an owner can have.

Use a document checklist

A disciplined review looks like this:

- Identify the component at issue

- Find the formal property classification

- Check the maintenance clause

- Check the insurance clause

- Review any policy resolution or maintenance matrix

- Confirm whether state law changes the document result

- Get the answer in writing from management or legal counsel when needed

That last step matters. Verbal explanations disappear. Written interpretations can be tracked and applied consistently.

What boards can do to reduce confusion

Boards can prevent many disputes by issuing a plain-language owner guide that summarizes common maintenance and insurance boundaries without trying to replace the legal documents. The guide should point back to the governing documents as the authority, not compete with them.

When communities make owners dig for basic answers, they create rumor-driven governance. That never ends well.

Partnering for a Thriving Community

The answer to what does HOA cover isn’t a short checklist. It’s a system of shared obligations, insurance boundaries, maintenance duties, and long-term financial planning.

When those pieces are clear, owners know what they’re paying for. Boards make cleaner decisions. Presidents spend less time putting out preventable fires. Property values are better protected because the community is operating on facts instead of assumptions.

Strong communities usually share three traits. They define responsibility clearly, fund major obligations before they become emergencies, and communicate early when risk or repair affects owners.

That kind of consistency doesn’t happen by accident. It requires experienced coordination, reliable accounting, document fluency, and day-to-day leadership support from professionals who understand how associations function. Boards that want a clearer picture of that role can review what a community association manager does.

Frequently Asked Questions About HOA Coverage

Does the HOA cover my roof leak

Maybe the roof repair itself. Not always the interior damage. In many communities, the association handles the common structural component, while the owner handles damaged finishes inside the home unless the documents or insurance outcome say otherwise.

Does HOA insurance replace my personal condo policy

No. A master policy and an owner policy do different jobs. Condo owners should review whether they need HO6 coverage for interior property, improvements, personal belongings, and personal liability.

Are balconies and patios always the owner’s job

No. They’re often limited common elements, which means the structure may be an HOA responsibility while upkeep or owner-caused damage remains the owner’s responsibility.

Can the HOA charge a special assessment even if I already pay dues

Yes, if the documents and applicable law allow it. Monthly dues fund operations and reserves, but a major unfunded project or major loss can still lead to an extra assessment.

If a pipe in the wall bursts, who pays

It depends on whether that pipe serves one home or multiple homes, where the damage occurred, and what the governing documents say. Shared infrastructure often falls to the association. Interior restoration often involves the owner and the owner’s insurance.

What’s the fastest way to get a reliable answer

Read the declaration, bylaws, insurance summary, and any maintenance matrix together. If the issue is significant, ask management or association counsel for a written interpretation instead of relying on neighbor advice.

If your board wants clearer maintenance boundaries, stronger financial planning, and steadier day-to-day support, Access Management Group can help. Their team has served condominium and homeowner associations since the 1970s, with a long-standing focus on protecting, preserving, and enhancing community real estate investments in Georgia.