The first monthly statement catches many condo owners off guard. The mortgage makes sense. Property taxes make sense. Insurance makes sense. Then there is the association fee, and for a lot of owners, that is the line item that raises the core question: what am I paying for?

That question isn’t small. In 2024, about 25% of all U.S. owned households paid condo or homeowners association fees, the national median monthly fee was $135, and 3 million households paid more than $500 monthly according to the U.S. Census Bureau’s reporting on condo and HOA fees. So if you’re looking at homeowners association fees for condos and trying to decide whether the amount is fair, sustainable, or risky, you’re in a very large group.

After decades in condominium and community association management, one pattern shows up again and again. Owners rarely object to paying fees when they understand the purpose, trust the process, and can see that the board is protecting the property for the long term. Trouble starts when fees are too low for too long, reserves are neglected, and everyone acts surprised when a major repair bill arrives.

Your Guide to Condo Association Fees

A condo owner in Atlanta opens the payment portal for the first time and sees a recurring assessment that’s higher than expected. That reaction is normal.

Most owners know condo living includes shared expenses. Fewer know how those expenses are structured, why condo fees usually differ from neighborhood HOA dues for detached homes, and what separates a healthy fee from an artificially low one.

That distinction matters. A low monthly fee can feel like a bargain right up until the building needs a roof replacement, waterproofing work, elevator repairs, or major insurance adjustments. Then the full cost appears all at once.

Why condo fees deserve close attention

Homeowners association fees for condos are not just a convenience charge. They are the funding mechanism for the building’s operations, maintenance obligations, and long-term capital responsibilities.

For homeowners, the fee affects monthly affordability, resale value, and exposure to surprise assessments. For board members, the fee is one of the clearest tests of fiduciary judgment. Set it too high without explanation and owners lose confidence. Set it too low and the community eventually pays for it in a much harsher way.

Good condo finance isn’t about keeping fees low. It’s about keeping the community stable.

What experienced boards focus on

Boards that handle condo finances well usually do three things consistently:

- They budget for reality: They fund the services the building needs, not the services owners wish were cheaper.

- They separate short-term and long-term money: They don’t use reserve cash to patch routine operating shortfalls.

- They explain the trade-offs clearly: Owners are more willing to support responsible fees when the board shows what those fees prevent.

If you’re an owner, this guide will help you read the number on your statement with more confidence. If you’re on the board, it will help you evaluate whether your current fee structure is protecting the community or postponing a problem.

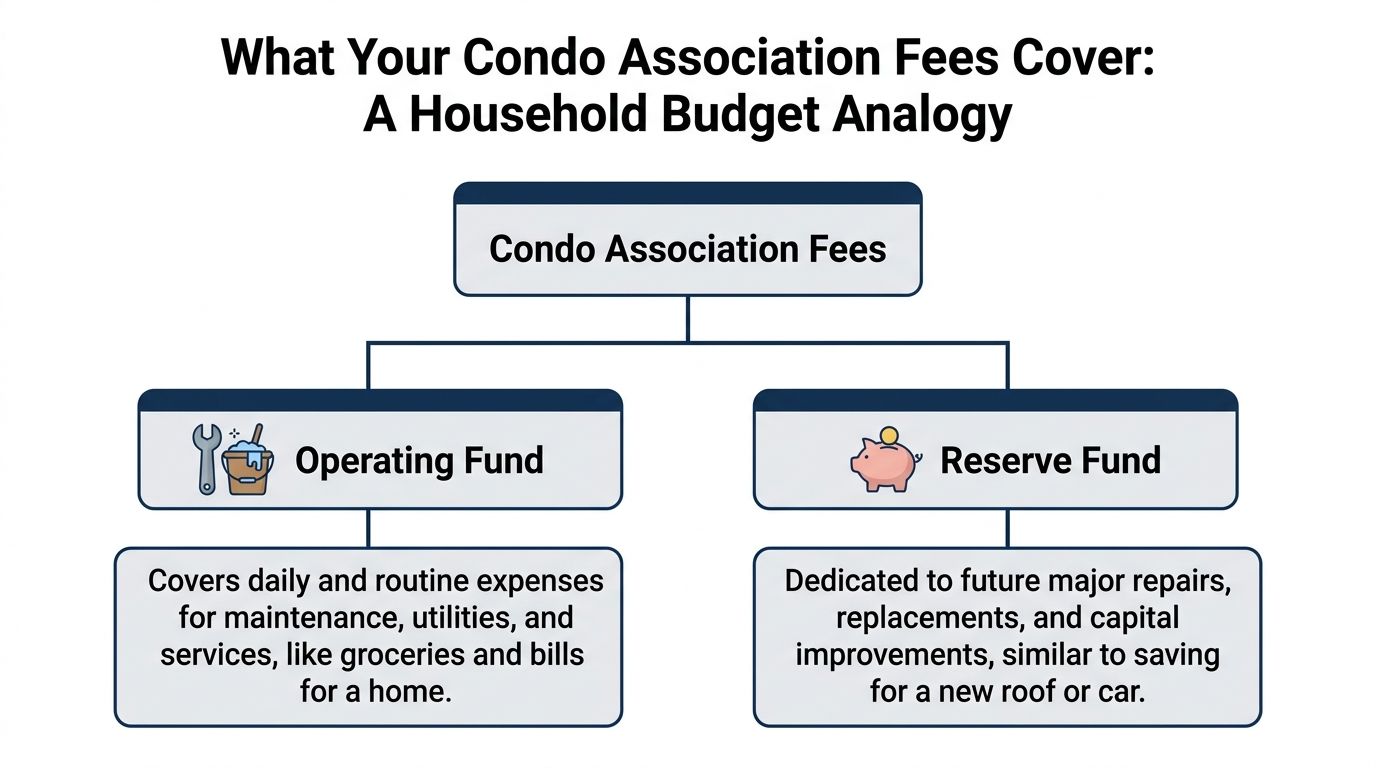

What Your Condo Association Fees Cover

The cleanest way to understand a condo fee is to think about a household budget. Some money pays the bills that recur every month. Some money goes into savings for the expensive items you know are coming, even if they aren’t due today.

A condominium works the same way. Every properly structured budget has an operating fund and a reserve fund.

The operating fund

The operating fund is the association’s working account. It covers the recurring costs of running the property day to day.

Typical operating expenses often include:

- Common area utilities: Lighting in hallways, lobbies, parking areas, and other shared spaces.

- Janitorial and cleaning: Interior common areas, trash rooms, entryways, and shared restrooms if the property has them.

- Grounds care and grounds care: Beds, turf, seasonal cleanup, irrigation service, and routine exterior appearance work.

- Management and administrative costs: Financial reporting, owner communications, vendor coordination, collections support, and meeting administration.

- Routine maintenance and service contracts: Small repairs, preventive maintenance, inspections, and regular system servicing.

- Insurance premiums: Master policy costs and related shared risk protection.

- Security and staffing where applicable: Front desk coverage, gate operations, access control support, or patrol services in communities that provide them.

The reserve fund

The reserve fund is different. This is long-term capital money. It is set aside for major repairs and replacements that will happen eventually, even if the exact date isn’t known.

Reserve funding often supports expenses such as:

- Roof replacement

- Exterior painting or waterproofing

- Pavement and concrete replacement

- Elevator modernization

- Pool surface and equipment replacement

- Building envelope repairs

- Major mechanical replacements

- Clubhouse or common-area capital renewal

Operating vs reserve funds

| Operating Fund Expenses (The “Everyday”) | Reserve Fund Expenses (The “Big Ticket” Items) |

|---|---|

| Utility bills for shared areas | Roof replacement |

| Janitorial and routine cleaning | Elevator modernization |

| Day-to-day maintenance calls | Major paving or concrete replacement |

| Management and administration | Exterior painting or waterproofing |

| Grounds maintenance service | Pool renovation or equipment replacement |

| Ongoing service contracts | Large mechanical system replacement |

| Insurance billed in the normal cycle | Capital repairs to building components |

Why condo fees are usually higher than HOA dues for detached homes

Condo associations usually carry more structural responsibility. That changes the budget.

According to FirstService Residential’s explanation of condo fees vs. HOA fees, condo fees are systematically higher than single-family HOA fees because condo budgets must cover major shared structural components such as roofs, elevators, and complex plumbing systems. In some markets, that can result in condo fees being 25% to 60% higher.

That tracks with what managers see in practice. A detached-home HOA may maintain entrances, amenities, and grounds care. A condo association often has to maintain the building itself. That means the board is responsible for expensive systems no single owner can handle alone.

Practical rule: If a condo fee seems unusually low for a building with elevators, extensive common interiors, or aging infrastructure, don’t assume it’s efficient. Assume it needs explanation.

What doesn’t work

Boards get into trouble when they blur these categories.

A few common mistakes:

- Using reserves for ordinary bills: That weakens long-term capital planning.

- Ignoring preventive maintenance: It lowers current spending, then raises future replacement costs.

- Treating reserves like optional savings: In a condo, they are not optional in any practical sense.

Owners should be able to look at the budget and tell what portion of their fee supports operations and what portion supports reserves. If that isn’t clear, the association needs better reporting.

How Condo Association Fees Are Calculated and Adjusted

Condo fees don’t come out of thin air. A responsible board starts with the expenses the community must cover, builds an annual budget, and then allocates that amount according to the governing documents.

That process is financial planning, but it’s also governance. The board has to balance present affordability against future obligations, and that balance affects every owner.

The annual budgeting process

Most condo fee calculations begin with a straightforward sequence.

-

Review current operating costs

The board and manager examine contracts, utility trends, insurance renewals, maintenance history, and known service changes. -

Project next year’s operating needs

Every routine category gets updated based on current conditions. If a building is aging, maintenance line items usually need closer scrutiny. -

Evaluate reserve requirements

The board compares current reserve contributions to the property’s expected capital repair and replacement needs. -

Set the total assessment requirement

Once operating and reserve needs are combined, the association determines how much total assessment income it must collect. -

Allocate the budget among owners

In most condominiums, this happens through the ownership percentages or formulas stated in the declaration.

Why one unit may pay more than another

In condo communities, fees are often allocated on a pro-rata basis tied to each unit’s percentage of ownership. That percentage may be based on square footage or another formula built into the governing documents.

Larger units commonly carry a larger share. Some communities also have limited common element allocations or special formulas for certain components, depending on their documents.

What matters most is consistency. Boards should not improvise fee allocation methods. They should follow the declaration exactly and explain the method in plain language when owners ask.

Why fees increase even when the board is careful

Owners often assume a fee increase means the board failed to control spending. Sometimes the opposite is true.

The Foundation for Community Association Research reports that community associations are projected to reach 377,000 by 2026, 91% faced unexpected expense hikes tied to inflation and rising insurance costs, and 71% of boards planned fee increases for 2025. That tells owners something important. Adjustments are normal in a changing cost environment, not evidence of mismanagement by themselves.

In communities, the main drivers are usually easy to identify:

- Insurance pressure: Master policy increases can move a budget quickly.

- Vendor cost changes: Grounds care, cleaning, maintenance, and mechanical service contracts rarely stay flat.

- Utility volatility: Shared electric, water, and other utility expenses can shift.

- Deferred maintenance catching up: Boards that delayed work often face steeper costs later.

- Reserve correction: If prior boards underfunded reserves, a future board has to fix it.

What good adjustment look like

A solid board doesn’t hide the reason for an increase. It shows owners the math.

That usually includes:

- Approved budget detail

- Comparison to prior actual expenses

- Clear explanation of unusual changes

- Reserve funding rationale

- Expected owner impact by unit type

For communities that want more disciplined reporting and assessment administration, boards often rely on specialized accounting systems and management support. A practical example is accounting for homeowners associations, where structured invoicing, collections tracking, and financial reporting help boards tie assessments directly to budget execution.

The right question isn’t “Did fees go up?” It’s “Did the board increase fees for known reasons, with documentation, before a larger problem forced their hand?”

What does not work

Three budgeting habits usually create avoidable conflict:

- Flat budgets that ignore rising costs

- Across-the-board cuts without asset analysis

- Fee decisions driven by owner pressure instead of financial obligations

That last one is especially damaging in condos. Buildings don’t become cheaper to maintain because a meeting got tense.

Avoiding Financial Shocks with a Strong Reserve Fund

The greatest financial risk in most condominium communities isn’t the monthly fee itself. It’s the gap between what the property will eventually need and what the association has saved.

That gap is where special assessments come from.

Why low fees can be dangerous

Owners naturally like low monthly costs. Boards feel pressure to deliver them. But unusually low condo fees often signal that the association is not collecting enough to match the property’s real obligations.

That’s not a savings strategy. It’s a delay strategy.

The Nolo guidance on condo and HOA dues notes that unusually low fees can be a red flag for an inadequate reserve fund. It also identifies a key benchmark: a reserve study should aim to cover 70% to 100% of projected capital needs over 30 years. When communities miss that standard, sudden special assessments can exceed $10,000 per unit and can hurt property values.

What a reserve study does

A reserve study gives the board a structured way to answer the question owners ask most often and understand least: are we saving enough?

A credible reserve study typically identifies:

- Major common elements the association must repair or replace

- Estimated useful life of each component

- Estimated remaining life

- Current replacement cost

- Recommended funding path

This is the framework boards need because reserve adequacy cannot be judged by account balance alone. A reserve account may look large on paper and still be weak if the building has expensive projects approaching.

A simple way to evaluate adequacy

Owners and boards don’t need to become reserve specialists to ask smart questions. Start with this working checklist.

Ask whether the reserve study is current

If the study is old, the board is planning with stale assumptions. Component conditions change. Costs change. Priorities change.

Ask whether the board is following the study

Some communities commission a reserve study, then ignore the funding recommendations because owners resist higher fees. That defeats the purpose.

Ask how major projects will be funded

The answer should be specific. If the roof, waterproofing, paving, or elevator work is foreseeable, the board should already know whether reserves will cover it or whether financing or a special assessment may be required.

Ask whether reserves are being used properly

Reserve money should be used for capital repair and replacement, not routine operating shortfalls. If the association borrows from reserves to cover ordinary bills, owners should expect future strain.

Consequences of Underfunding

Underfunded reserves create a chain reaction.

- Repairs get delayed

- Component failures become emergencies

- Emergency work costs more

- Boards lose flexibility

- Owners receive sudden assessments

- Buyers and lenders become more cautious

Here, board decisions become fiduciary decisions in the clearest sense. When a board knowingly keeps fees low by starving reserves, it shifts today’s political comfort ahead of tomorrow’s legal and financial responsibility.

Reserve funding is how a board turns predictable deterioration into predictable payments.

What works in practice

Communities with healthier financial outcomes usually follow the same habits:

- They update reserve studies on a regular schedule

- They tie annual contributions to actual component needs

- They explain reserve funding in owner-friendly language

- They avoid using reserves as a convenience account

- They plan projects before they become emergencies

Boards that need a more detailed framework for evaluating reserve obligations can review condo reserve fund requirements and compare current practices against common reserve planning expectations.

A board-level framework for decision making

When a board is deciding whether condo fees are too high, too low, or about right, these are the questions worth asking:

| Question | Healthy answer |

|---|---|

| Is the reserve study current? | Yes, and the board uses it |

| Are reserve contributions aligned with expected capital needs? | Yes, contributions reflect known obligations |

| Are operating expenses fully covered without borrowing from reserves? | Yes |

| Are major projects identified before failure occurs? | Yes, with a funding path |

| Can owners understand how the fee was built? | Yes, through clear budget communication |

What does not work

A few approaches almost always backfire:

- Keeping fees artificially low to avoid complaints

- Postponing visible repairs because cash is tight

- Hoping a future board will solve reserve gaps

- Assuming property values will offset poor financial planning

That last assumption is particularly risky. Buyers don’t just purchase a unit. They purchase into the association’s financial condition.

Navigating Your Role in the Association’s Finances

Condo finances work best when owners and board members understand that they are not on opposite sides. They have different jobs, but the same stake. They both need a stable property, predictable funding, and credible financial records.

When that partnership breaks down, owners feel shut out and boards feel attacked. When it works, fees are easier to explain, collections improve, projects move faster, and trust holds up even during difficult budget cycles.

What owners should do

Owners don’t need to manage the association, but they do need to stay informed.

Useful owner habits include:

- Read the budget package: Don’t stop at the total assessment number. Look at the categories that changed.

- Review meeting notices and minutes: Boards often explain pending projects and cost pressures there.

- Ask focused questions: “How was the reserve contribution determined?” is better than “Why are fees so high?”

- Pay assessments on time: Delinquencies hurt the whole community by disrupting cash flow.

- Watch for patterns, not rumors: One unhappy conversation in the hallway is not financial analysis.

What board members must do

Board service in a condominium is a fiduciary role. That means directors must act in the best financial interest of the association as a whole, not just respond to the loudest owner concerns.

A board’s responsibilities typically include:

- Approving realistic budgets

- Maintaining accurate records

- Protecting reserve integrity

- Following governing documents

- Communicating financial decisions clearly

- Documenting the basis for major decisions

That communication piece matters even more because external benchmarks are changing. The ACS technical note on condo and HOA fee reporting explains that starting in 2024, the U.S. Census Bureau combined condo and HOA fees in its housing cost reporting, which makes historical comparisons difficult. Boards should understand those reporting changes before citing outside fee trends to owners.

Transparency is a practical tool, not a slogan

Owners don’t expect perfection. They do expect a board that can explain its decisions.

That usually means sharing:

- Approved annual budgets

- Year-end financial statements

- Reserve study summaries

- Known major project timelines

- Assessment change notices with plain-language explanations

Boards that need a clearer operating framework can review practical guidance on HOA board responsibilities and use it to sharpen roles, documentation, and owner communication.

A board earns credibility when owners can trace each fee decision back to a documented obligation.

Where associations lose trust

The same trust failures appear repeatedly in struggling communities:

- Vague explanations for fee increases

- Late disclosure of major repair needs

- Confusing financial statements

- Defensive responses to legitimate owner questions

- Inconsistent enforcement of collection policies

Most owners can accept bad news sooner than they can accept hidden news later.

What Every Condo Buyer Must Ask About Association Fees

A condo buyer should never stop at “What are the monthly dues?” That number by itself tells you very little.

A better approach is to treat the association’s finances the way you would treat the unit’s roof leak, HVAC age, or plumbing history. You’re buying into a shared financial structure. If that structure is weak, your ownership costs can change quickly.

The due diligence questions that matter

Ask for these items before you close, and pay attention to how quickly and clearly the answers arrive.

-

Can I review the current approved budget?

This shows what the association is funding now, not what someone remembers from last year. -

Can I see recent financial statements?

You want to know whether the association appears organized, current, and consistent in its reporting. -

Is there a reserve study, and is it current?

This is one of the most important questions in any condominium purchase. -

How are major repairs expected to be funded?

A confident answer suggests planning. A vague answer suggests risk. -

Are there any pending special assessments or major capital projects?

Buyers need to know whether ownership could begin with an additional financial obligation. -

Have there been recent fee increases, and why?

The explanation matters more than the fact of the increase. Regular, documented adjustments are often healthier than long periods of flat fees followed by a sharp correction. -

What does the fee include, and what remains the owner’s responsibility?

This helps you understand your true monthly cost and maintenance exposure. -

Are there delinquency issues affecting cash flow?

Collections problems can pressure the entire budget and delay necessary work.

Green lights and red flags

A healthy association often shows the same signs:

- Clear records

- Current reserve planning

- Plain-language explanations

- A steady budgeting pattern

- Defined project priorities

Red flags tend to look different:

- Very low fees with no reserve explanation

- No current reserve study

- Repeated deferral of visible maintenance

- Confusing or incomplete financials

- Seller assurances that aren’t backed by documents

What buyers often misread

Some buyers assume high fees automatically mean a bad association. That isn’t necessarily true.

High fees may reflect extensive amenities, aging infrastructure, staffing requirements, or a board that is finally correcting underfunding. Low fees may reflect the opposite. Without documents, neither number tells the full story.

The smartest buyers ask whether the fee is adequate, not whether it is cheap.

Frequently Asked Questions About Condo Association Fees

Can condo association fees be negotiated

No. Individual owners generally can’t negotiate their personal monthly assessment. The fee is set through the association’s budget and allocation method under the governing documents.

If an owner thinks the fee structure is wrong, the remedy is community governance. Review the records, attend meetings, and raise the issue through the board process.

Why do condo fees usually rise over time

Buildings age. Service contracts change. Insurance changes. Reserve needs become clearer.

A flat fee over many years may look attractive, but in many communities it means the board has delayed real financial adjustments. Gradual, documented increases are usually easier on owners than a large correction after years of underfunding.

Does a high condo fee always mean the association is healthy

No. A high fee can still coexist with poor planning, weak controls, or deferred maintenance.

The right question is whether the budget is well built, the reserves are credible, and the board can explain where the money goes. Fee amount alone is never enough.

What happens if an owner doesn’t pay

That creates a problem for the entire community because the association still has to meet its obligations.

Most associations follow a collection process set by policy and legal requirements. Owners should understand that unpaid assessments don’t disappear. They shift pressure onto the community’s cash flow and often lead to additional enforcement costs.

Should owners worry if the association has low fees

They should at least ask more questions.

Low fees are only good news if the association is also funding operations properly, maintaining the property, and building reserves for known capital work. If any of those pieces are missing, low fees may be a warning sign rather than a benefit.

What is the single most important financial question a board should ask

“Are we funding the property we have?”

That question cuts through most budget confusion. It forces the board to look at the current building, the current contracts, the necessary reserve needs, and the true consequences of postponing costs.

Access Management Group works with condominium and homeowner associations across Georgia on the practical side of community finance, including assessment administration, financial reporting, and board support. If your community needs clearer budgeting, stronger reserve planning, or better owner communication around homeowners association fees for condos, learn more at Access Management Group.