You’ve just joined the board, and within weeks someone asks the question every new condo president dreads: “How are we going to pay for that?”

The roof is aging. The elevators are acting up. The waterproofing repair can’t wait much longer. Owners are frustrated, vendors want answers, and the operating account was never meant to carry capital replacements. That’s when many boards discover an ugly truth. They weren’t budgeting for the building’s future. They were just surviving the present.

A reserve study changes that. It gives the board a disciplined way to plan for predictable major repairs before they turn into community-wide conflict. If you want to protect owner equity, avoid financial panic, and govern like a board that takes its fiduciary duty seriously, reserve studies for condominiums belong near the top of your list.

Your Community’s Financial Safety Net

A board usually doesn’t appreciate reserve planning when things are quiet. It appreciates it when a major component fails and the money isn’t there.

That’s the moment trust breaks. Owners don’t just see a repair bill. They see a board that didn’t plan, a budget that didn’t reflect reality, and a property that may now carry the stigma of deferred maintenance. If the only answer is a surprise assessment, the damage goes beyond the invoice. It hits resale conversations, owner confidence, and the board’s credibility. Boards dealing with those consequences often end up learning the hard lessons behind a condominium special assessment.

What a prepared board does differently

A prepared board treats major common element replacements as inevitable, not hypothetical. Roofs wear out. Paving deteriorates. Mechanical systems age. Exterior components don’t care whether the association feels financially ready.

A reserve study gives the board a long-range view of those obligations and a practical funding path. It’s the difference between reacting to a crisis and governing with foresight. That’s why I don’t view reserve studies for condominiums as paperwork. I view them as the board’s financial safety net.

Practical rule: If a repair would trigger owner panic if it happened next year, it belongs in the board’s reserve planning conversation now.

Why this matters to homeowners

Homeowners don’t buy into a condominium just for a unit. They buy into a shared physical asset and a shared financial structure. When the board funds reserves responsibly, owners get more than a healthier balance sheet. They get predictability.

That predictability matters because boards make one of two choices. They either collect steadily over time, or they collect painfully when something breaks. The second option is always more disruptive.

A reserve study helps the board choose the first path. It supports stable planning, better decision-making, and a stronger case that the board is protecting owner investments instead of pushing costs onto future owners.

What Is a Condominium Reserve Study

A condominium reserve study is a building health plan with numbers attached. It tells the board what major common components it’s responsible for, how those components are aging, what they may cost to repair or replace, and how the association should fund those future obligations.

That sounds technical, but the logic is simple. Your building is wearing down every year. A reserve study measures that reality and turns it into a funding strategy.

The physical side of the study

The first half is the physical analysis. In this part, the provider inventories major common elements, reviews condition, and estimates useful life and replacement cost.

That includes the assets owners don’t always think about until they fail. Roof assemblies, pavement, waterproofing, siding, elevators, HVAC serving common areas, and other shared components often belong here, depending on the property and governing documents.

If your board wants a good mental model, consider it a comprehensive schedule of condition for the community’s common elements. You need an organized record of what exists, what condition it’s in, and what likely lies ahead.

The financial side of the study

The second half is the financial analysis, in which the reserve professional evaluates current reserve fund status and recommends a funding plan over a long horizon.

According to Reserve Advisors’ explanation of reserve studies, reserve studies bifurcate into physical analysis and financial analysis, and the standard contents include summaries of units, physical descriptions, fund conditions, and 20-year tabular projections so boards can forecast expenses accurately.

That matters because a reserve study isn’t just a component list. It’s a decision tool. It shows whether current contributions are aligned with future obligations or whether the board is building a problem for later.

Terms every board president should understand

A few terms come up constantly in reserve studies for condominiums:

- Common elements are the shared components the association is responsible to maintain, repair, or replace.

- Useful life is how long a component is expected to perform before replacement becomes necessary.

- Remaining useful life is what’s left, not what the component had when it was new.

- Current replacement cost is the present-day estimate to replace the component.

- Recommended contribution is the funding level the study says the board should build into the budget.

A reserve study isn’t predicting the future with perfect accuracy. It’s giving the board a disciplined basis for responsible decisions.

That’s the key mindset. Don’t ask whether the study will be perfect. Ask whether your board is willing to budget major capital obligations with no structured analysis. It shouldn’t be.

The Two Main Reserve Study Funding Methodologies

Most boards get stuck on one question: how should we fund this?

There are two main approaches. One is more precise and more conservative. The other offers flexibility but requires discipline. If you don’t understand the difference, you can’t make a sound budget decision.

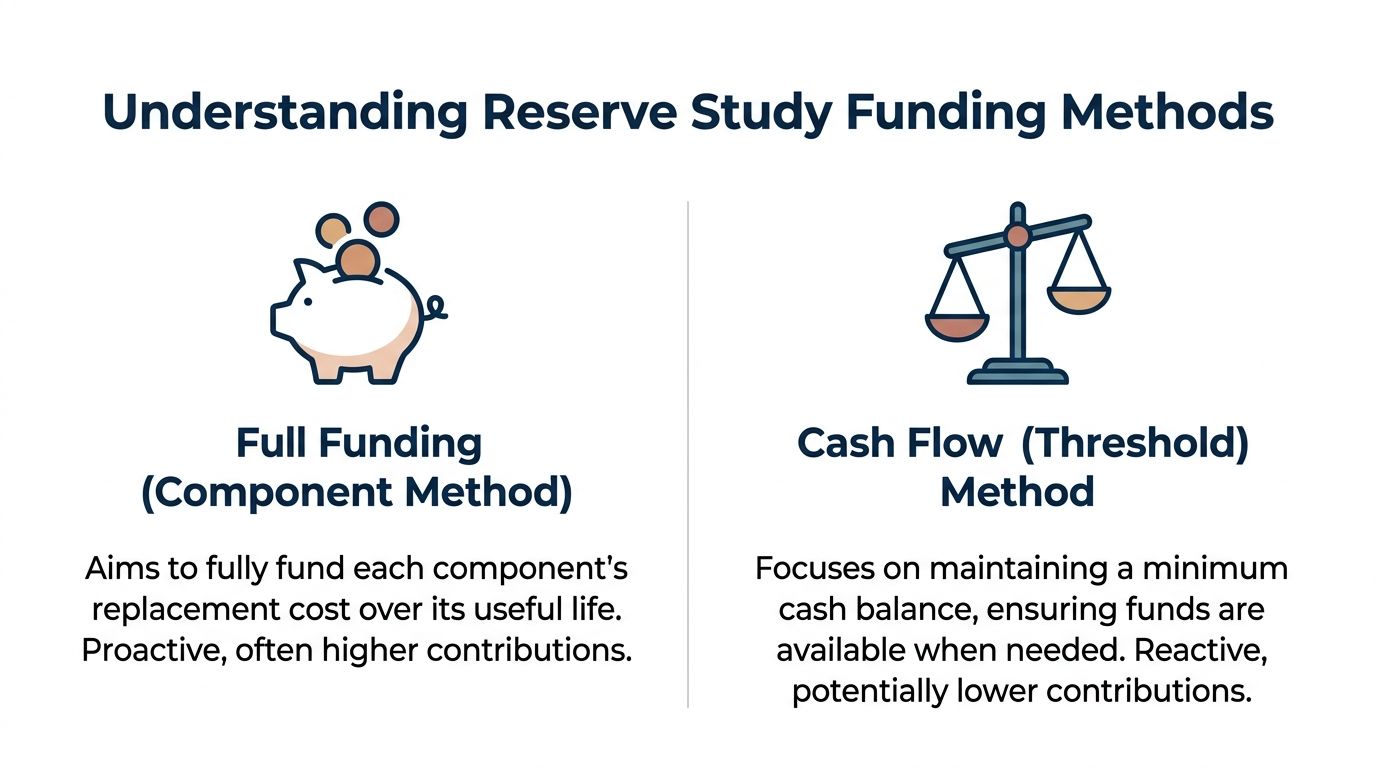

Full funding as the disciplined option

Full Funding, sometimes called the component method, works like a set of dedicated savings buckets. Each major component accumulates funding over its useful life so the association steadily builds toward that component’s eventual replacement cost.

This method tends to be more conservative. Boards that choose it are usually prioritizing stability, lower long-term risk, and a clearer relationship between deterioration and funding. I like this approach for boards that want fewer unpleasant surprises and stronger financial optics.

Cash flow as the flexible option

Cash Flow, also called threshold funding, works more like one pooled reserve account. The goal isn’t to fully accumulate every component’s projected replacement amount at the same time. The goal is to keep the reserve balance above a minimum threshold while meeting expected expenditures as they arise.

This approach can work well when the study is credible, the board reviews it carefully, and annual budgeting is disciplined. It is not an excuse to keep assessments artificially low. Used responsibly, it’s a planning methodology. Used carelessly, it becomes a delay tactic.

The metric that tells you where you stand

The most important number in the reserve conversation is Percent Funded. It compares your current reserve balance to the Fully Funded Balance, which represents the accumulated deterioration your reserves should cover.

The CAI Foundation reserve planning guide states that Percent Funded is categorized this way: 0-30% is weak and carries high insurance risk, 30-70% is fair and is where threshold funding is commonly recommended, and 70-100% is strong. The same guide says associations should generally allocate 15% to 40% of total assessments to reserves.

That one metric tells a board a great deal. A community in the weak range is exposed. A community in the fair range has work to do but can still operate from a defensible plan. A community in the strong range is in a better position to manage capital expenses without constant financial drama.

Comparing reserve funding methodologies

| Feature | Full Funding (Component) Method | Cash Flow (Threshold) Method |

|---|---|---|

| Core idea | Builds funding toward each component’s deterioration | Maintains a pooled balance above a planned minimum |

| Board mindset | Conservative and highly proactive | Flexible, but only if the board stays disciplined |

| Budget impact | Often calls for higher regular contributions | May smooth contributions, but can mask underfunding if handled poorly |

| Risk profile | Lower chance of sudden catch-up decisions | More sensitive to bad assumptions, delays, or skipped updates |

| Best fit | Boards focused on long-term stability and cleaner reserve posture | Boards with good forecasting, active oversight, and strong budgeting habits |

My recommendation to new board presidents

If your community has a history of low reserves, deferred maintenance, or resistance to realistic dues, don’t chase flexibility. Chase clarity. Full funding often forces a harder conversation upfront, but it prevents worse conversations later.

If your reserve professional recommends threshold funding, then insist on discipline. Review the assumptions, understand the spending schedule, and make sure the board treats the reserve plan as a living financial framework, not a document to approve and forget.

Boards don’t get in trouble because a methodology exists. They get in trouble because they use a methodology without the governance to support it.

The Reserve Study Process from Start to Finish

Boards often make this harder than it needs to be. A reserve study is a professional project, and it should be run like one. The process is straightforward when the board stays organized and stops treating provider selection as a race to the lowest fee.

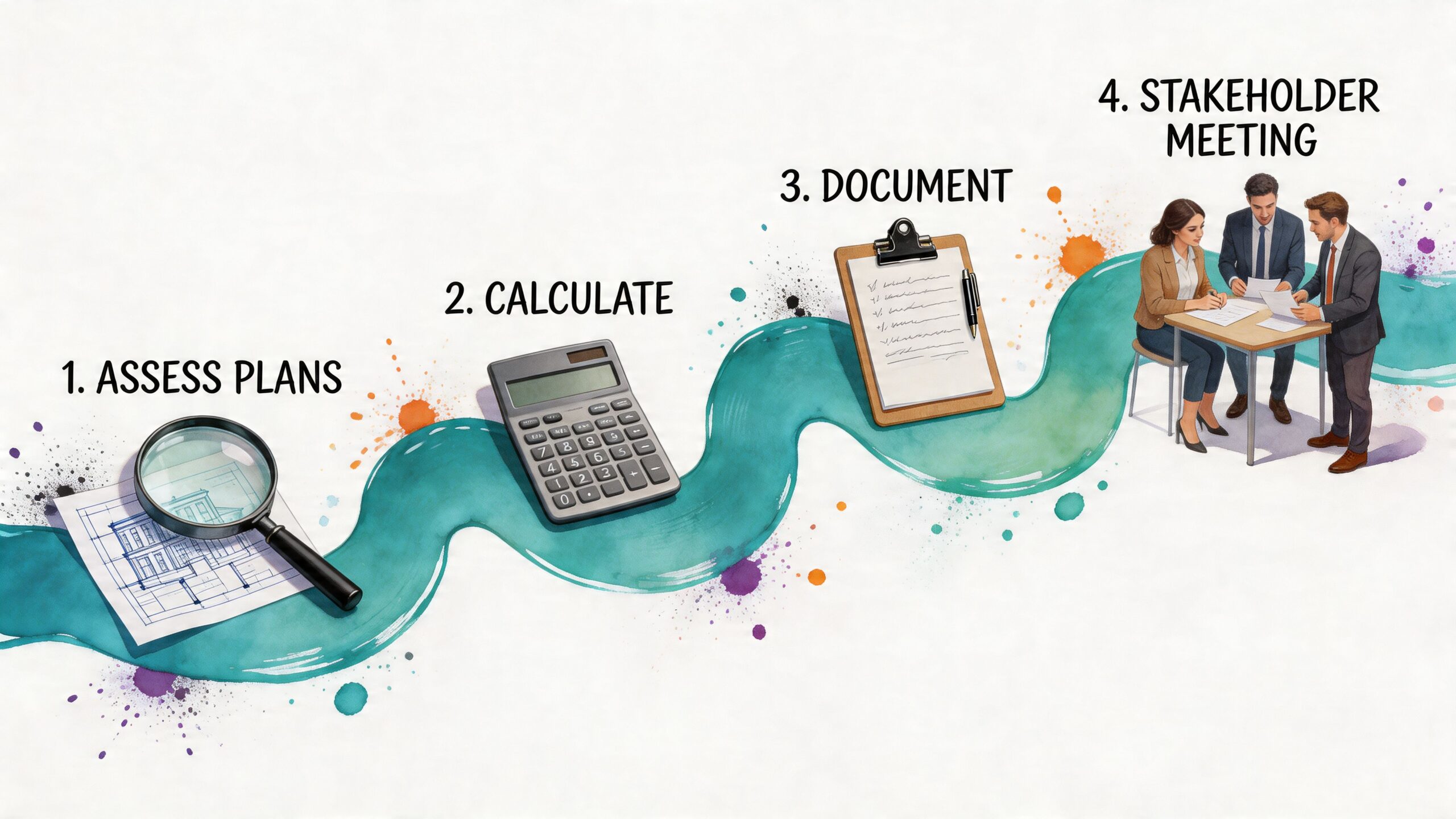

Step one, select the right scope and provider

Start with qualifications, not price. The board needs a provider who understands condominium components, funding models, and realities of shared-property governance.

The Rimkus guide to reserve studies notes that reserve studies are typically updated every 3-5 years, and it identifies four levels of service: Level I for a full physical inspection for a new study, Level II for an update with on-site review, Level III for an update with no on-site review, and Level IV for pre-construction budgeting.

That framework matters because not every association needs the same thing.

- New study needed: A community with no credible baseline usually needs Level I.

- Existing study, conditions changing: A board that wants refreshed field verification should look closely at Level II.

- Minor update cycle: If the prior work is solid and site conditions haven’t materially changed, Level III may be enough.

- Developer or early planning use: Level IV serves pre-construction budgeting, not mature operational decision-making.

Step two, prepare the board’s information

A reserve provider can only assess what the association identifies and documents. Give the provider complete records, not half the story.

That means gathering governing documents, maintenance history, prior reserve studies, vendor proposals, repair invoices, and any known issue lists. If the association recently patched a roof section, replaced part of a mechanical system, or deferred a major project, the provider needs to know.

Boards often assume the site visit will reveal everything. It won’t. Good reserve planning depends on both inspection and documentation.

Step three, participate in the site review and draft discussion

When the provider visits the property, don’t treat it as a formality. Walk the site with purpose. Point out recurring problem areas, recently repaired items, and components that owners complain about most often.

Then read the draft carefully. Not casually. Carefully.

Look for problems such as:

- Missing components that the association clearly maintains

- Wrong assumptions about age, condition, or replacement responsibility

- Outdated repair history that changes useful life expectations

- Overly optimistic timing that pushes real costs too far into the future

A reserve study draft is where the board catches errors before they become budget policy.

Step four, adopt it and actually use it

The final report isn’t a trophy. It’s an operating tool. Once the board adopts it, the findings should inform budget development, capital planning, owner communication, and project timing.

A board that commissions the study and then ignores the funding recommendations wastes everyone’s time. Worse, it creates a false sense of security. Owners hear “we have a reserve study” and assume the finances match the report. Often, they don’t.

The right habit is simple. Put the reserve study on the annual governance calendar. Revisit assumptions, compare planned spending to actual conditions, and determine whether the study still reflects reality.

Using Reserve Study Findings to Build a Strong Budget

A reserve study becomes valuable when it changes the budget. Until then, it’s just a report.

Board courage is paramount. If the study says your current reserve contribution is too low, the answer isn’t to file the report and hope a future board deals with it. The answer is to build a budget that starts closing the gap now.

Turn the recommendation into a real budget line

The reserve contribution belongs in the annual budget as a deliberate funding decision, not as whatever is left over after operating expenses. Boards that budget reserves last usually underfund them.

That’s backwards. Major replacements are not optional. They are known future obligations. Treat them with the same seriousness as insurance, management, utilities, and contracted maintenance.

A strong board budget does three things:

- It reflects the reserve study’s recommended contribution.

- It separates reserve funding from routine operating spending.

- It explains to owners why regular funding is better than emergency collection.

If your board needs cleaner financial reporting around reserve activity, solid accounting for homeowners associations supports better decisions and better homeowner communication.

Why outdated studies create bad budgets

A board can’t budget accurately from stale assumptions. Material pricing changes, interest-rate pressure, and aging components can quickly make an old plan unreliable.

The Davis-Stirling reserve funding discussion states that, amid 2024-2026 economic shifts, smaller associations have seen 25% higher special assessment rates than larger peers when studies are outdated. That should get every small and mid-sized condo board’s attention.

If your community has been relying on an old reserve plan, your budget may look stable on paper while actual replacement costs move in the opposite direction.

What disciplined budgeting looks like

A disciplined board doesn’t ask, “How low can we keep dues?” It asks, “What level of funding protects the community over time?”

That shift in mindset changes everything.

- When reserves are underfunded: The board faces catch-up decisions, compressed project timelines, and owner resistance when bad news finally surfaces.

- When reserves are funded consistently: The board has options. It can phase projects, negotiate from a position of readiness, and avoid governance by crisis.

- When owners understand the plan: Dues increases become easier to explain because they’re tied to visible obligations, not vague financial anxiety.

Owners may not like higher assessments. They dislike surprise assessments even more.

Reserve funding supports value, lending, and credibility

Reserve budgeting is not just about repairs. It affects how outsiders view the association.

The CAI Foundation guide cited earlier notes that some lender requirements include dedicating at least 10% of annual operating budget to reserves for FHA-backed loans or having a current study in place. That means reserve policy can influence financing conversations for buyers and sellers, not just internal accounting.

A board with a credible reserve plan also presents better to insurers, auditors, owners, and prospective purchasers. It signals competence. And in condominium governance, competence protects value.

Legal Requirements and Best Practices for Georgia Boards

Georgia boards often ask the wrong opening question. They ask, “Are reserve studies legally required?” The better question is, “What would a prudent board do to protect owner investments?”

Georgia does not have the same kind of statewide reserve study mandate described in other states within the verified materials. That doesn’t let a board off the hook. It raises the standard for judgment. If the law gives you discretion, then your fiduciary duty matters even more.

Best practice is the real operating standard

Nationally, reserve planning has been part of association governance for a long time. The CAI Foundation guide explains that reserve studies for condominiums originated as a financial planning concept in 1947, and it notes that 12 states mandate reserve funding today in some form through the cited framework in Best Practices Report 5 on reserve studies and funding.

My advice to Georgia boards is simple. Don’t wait for a mandate to tell you how to manage risk. Follow recognized best practices because they are good governance, not because someone forced you to do it.

The same verified guidance also notes California’s requirement for visual inspections every 3 years under Civil Code §5550 and Florida’s 10-year Structural Integrity Reserve Studies for certain buildings. You don’t need to live in those states to learn from their standards. They show where association governance is headed and what serious oversight looks like.

A board checklist worth adopting

Use this as an annual board checklist:

- Review the study annually: Confirm that major assumptions still match actual conditions and known projects.

- Track component changes: If the association repaired, replaced, or deferred a major item, note it for the next update.

- Protect reserve cash: Don’t blur the line between operating needs and reserve obligations.

- Schedule updates on time: If the property is aging or conditions are changing, don’t let the study drift into irrelevance.

- Discuss owner communication early: Funding decisions go better when the board explains the why before the budget meeting.

The Georgia reality

Because Georgia lacks a statewide reserve mandate in the verified material, many boards convince themselves they can postpone the issue. That’s a mistake.

No statute prevents financial drift. No lack of mandate repairs a failing roof. No board president wants to explain why obvious capital obligations were ignored until a special assessment became unavoidable.

Good Georgia boards treat reserve planning as a fiduciary necessity, not a compliance accessory.

Your Path to Financial Stability

A reserve study gives a condo board something every community needs and too many lack: a plan grounded in the physical reality of the property and the financial reality of future replacement costs.

That plan changes the board’s role. Instead of reacting to breakdowns, the board can budget intentionally, communicate transparently, and make capital decisions before urgency drives the outcome. That’s better for homeowners, better for resale confidence, and better for the long-term condition of the property.

The strongest communities don’t stumble into stability. Their boards build it through disciplined reserve planning, regular review, and budgets that reflect the building's true needs.

If you’re a new board president, start there. Don’t inherit vague assumptions. Don’t accept “we’ve always done it this way.” Get a credible reserve study, use it, and insist that future budgets respect it.

That’s how you protect the community’s finances without waiting for a crisis to teach the lesson for you.

Frequently Asked Questions About Reserve Studies

Can our board do a reserve study ourselves

A board can gather records, inventory components, and organize maintenance history. That work is useful. It is not the same as obtaining a professional reserve study.

For very small communities, a scaled approach may be discussed in industry materials, but for most condominium boards, a professionally prepared study provides better credibility, better assumptions, and a stronger basis for budgeting. DIY spreadsheets are fine as support documents. They are a poor substitute for professional analysis.

If our documents don’t require one, do we still need one

Yes, in my view you do.

A governing document that is silent on reserve studies doesn’t erase the board’s responsibility to plan for major common element replacement. If your association maintains shared components with meaningful replacement cost, the board needs a reserve planning tool. Silence in the documents is not a strategy.

How often should we update the study

Use the study type and age of the property to guide that decision, and don’t let it sit untouched for too long. As noted earlier, professional guidance commonly places updates on a recurring cycle, with the right level of service depending on whether you need a new baseline, an on-site refresh, or a financial-only update.

How do we explain higher reserve contributions to owners

Be direct. Tell owners the board is funding known future obligations gradually so the community can avoid more disruptive collection later.

Don’t talk in vague slogans. Show them the major components the association is responsible for and explain that stable contributions protect property values, reduce the odds of emergency assessments, and support responsible governance.

What’s the biggest mistake boards make

They commission the study and then ignore it.

The second biggest mistake is keeping assessments artificially low to avoid short-term pushback. Owners may applaud that for a while. Then the building sends the actual bill.

Access Management Group helps condominium and homeowner association boards protect, preserve, and enhance their communities with experienced management, disciplined financial oversight, and practical guidance rooted in decades of association expertise. If your board needs a stronger approach to reserve planning, budgeting, and long-term property stewardship, Access Management Group is the partner to call.