A board meeting like this usually starts with a simple agenda item and ends with a hard reality. The roof has failed sooner than expected. A retaining wall is shifting. Storm damage exposed repairs insurance won’t fully cover. The reserve account isn’t deep enough, and delaying the work will only increase risk to the community and to every owner’s property.

That’s when boards and homeowners run into one of the least popular but most important tools in community governance: the special assessment.

Handled poorly, a special assessment creates anger, distrust, owner delinquencies, and legal exposure. Handled properly, it preserves buildings, protects safety, stabilizes operations, and defends long-term real estate value. Boards need to treat it as a governance issue first and a billing issue second. Homeowners need a clear explanation of why the charge exists, how it was calculated, and what happens if the association does nothing.

Navigating Community Financial Crossroads

Most boards don’t want to levy a special assessment. Homeowners certainly don’t want to receive one. But when a major repair can’t wait and the funds aren’t available, avoiding the decision is worse than making it.

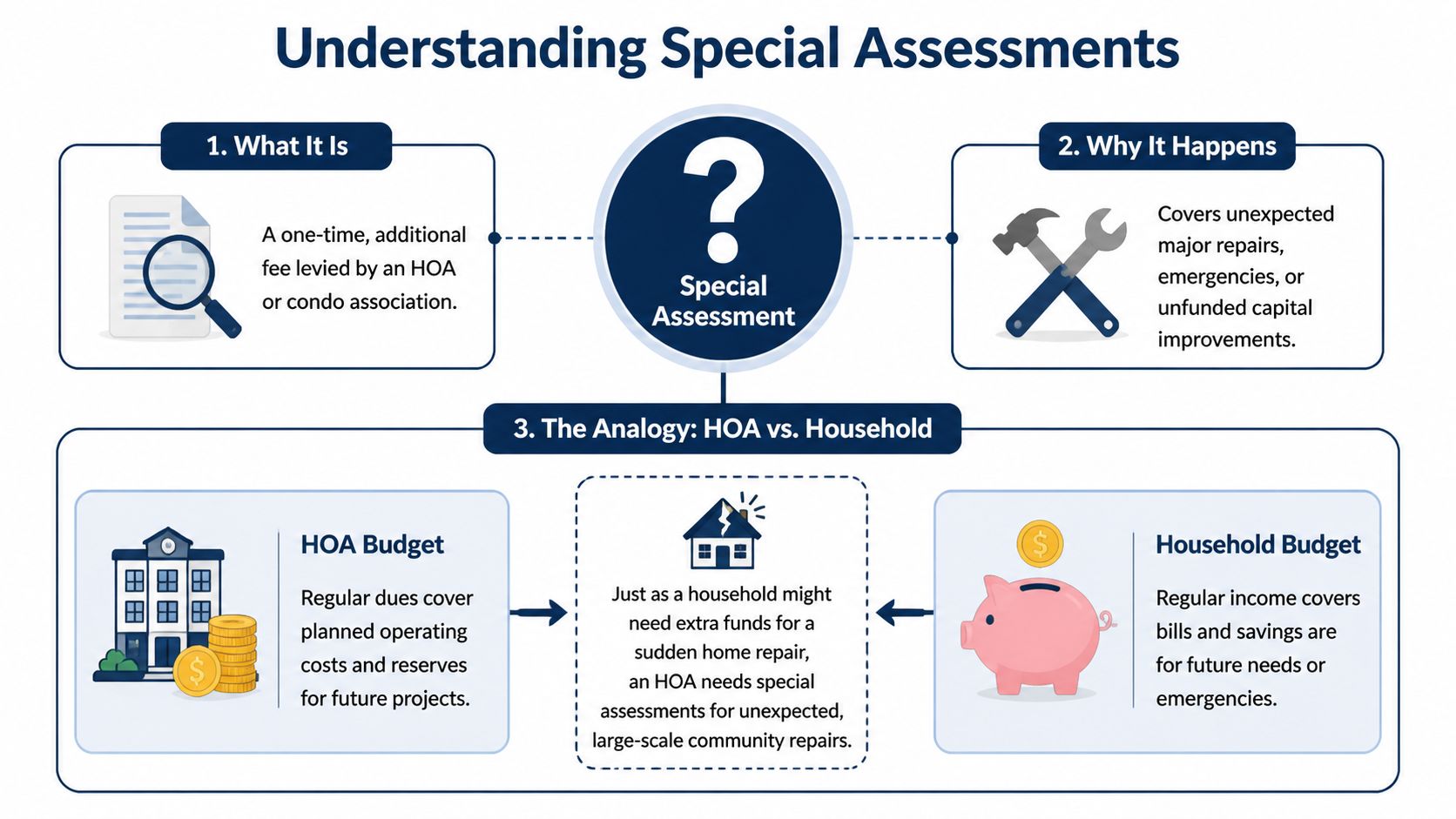

A special assessment is not a punishment. It’s a mandatory charge the association uses to fund a major cost that regular assessments and reserves can’t adequately cover. In practical terms, it’s often the difference between fixing a serious problem now or allowing the community’s physical condition and financial stability to deteriorate.

The stakes are bigger than one invoice. Special assessments can affect owner cash flow, payment performance, resale activity, and the tone of the entire community. They can also support projects that improve desirability and protect property values when boards use them for meaningful infrastructure work, as discussed by Reserve Data Analysis in its review of special assessments and community impact.

What boards must remember

A board’s job isn’t to avoid difficult decisions. It’s to make defensible ones.

That means asking the right questions early:

- Is the repair mandatory or discretionary

- Can reserves cover all or part of it

- What do the governing documents allow

- How will owners be informed before bills go out

- What payment structure gives the community the best chance of collecting without causing avoidable hardship

Boards lose credibility when they act surprised by known capital needs. Owners expect bad news to be managed, not discovered at the last minute.

In special assessments in real estate, the communities that perform best are not the ones that never face a funding gap. They’re the ones that respond with discipline, documentation, and transparent communication.

What Exactly Is a Special Assessment

Association finances work a lot like household finances. Your regular dues are the monthly income that pays predictable bills. Your reserve fund is the savings account set aside for major future replacements. A special assessment is the extra money you need when the expense is too large, too urgent, or too underfunded for both of those buckets.

That distinction matters because many owners confuse special assessments with fines or routine dues increases. They are not the same thing. A fine is a penalty for violating rules. A regular assessment funds normal operations. A special assessment is a separate charge for a defined project or expense that exceeds normal funding.

The cleanest way to explain it to owners

If your home needed an immediate, expensive repair and your checking account plus savings account weren’t enough, you’d need to find additional funds. An association faces the same problem, except the repair affects shared property and every owner has a stake in the outcome.

Use that analogy when communicating with homeowners:

- Regular dues pay for recurring costs such as landscaping, management, utilities, routine maintenance, and insurance.

- Reserves are saved over time for major predictable replacements.

- Special assessments fill a one-time or temporary funding gap for a major need.

What a special assessment is not

Boards should be precise with language. Sloppy wording causes unnecessary disputes.

- Not a fine: It isn’t imposed because someone broke a rule.

- Not a casual fee: It must connect to a legitimate association expense.

- Not a substitute for planning: If a board uses special assessments repeatedly for predictable work, owners will rightly question reserve discipline.

- Not always evidence of bad governance: Even well-run communities face emergencies, legal changes, and insurance-related shortfalls.

Practical rule: If the board can’t explain the need, scope, and funding gap in plain English, it isn’t ready to levy the assessment.

Why owners resist them

Owners resist special assessments for understandable reasons. They often arrive suddenly, they can feel unfair, and they force households to reprioritize spending. They also trigger a deeper concern that many boards underestimate: if the association didn’t plan for this, owners start wondering what else has been missed.

That’s why boards must frame the assessment around stewardship. The issue isn’t whether owners like paying it. They won’t. The issue is whether the board can show that the charge is necessary, authorized, and tied to preserving the community’s assets.

Common Triggers for Special Assessments

The most common trigger is simple. The community has a major cost, and normal funding isn’t enough.

That can happen for many reasons. Some are predictable but ignored. Others arrive without warning. In both cases, the board has to distinguish between discomfort and danger. Owner frustration is manageable. Structural deterioration, uninsured losses, and deferred life-safety work are not.

Deferred maintenance and weak reserves

This is the trigger boards should take most seriously because it’s often preventable.

Roofs, pavement, balconies, siding, drainage systems, elevator components, and building envelopes don’t fail overnight. Communities usually get warning signs. When boards keep dues artificially low, postpone reserve contributions, or ignore reserve study guidance, they push predictable costs into crisis territory. The special assessment then becomes a catch-up mechanism.

Boards should be blunt with themselves here. If the project was foreseeable and reserves were inadequate, the right lesson is not “owners won’t like this.” The right lesson is “we need a stronger reserve strategy after this is over.”

Storm damage, insurance gaps, and climate pressure

Weather-related costs are putting more associations in a bind. Special assessments can range from a few hundred to tens of thousands of dollars, and they’re increasingly common in states such as Florida, California, and Texas because of weather changes and infrastructure demands, according to Realtor.com’s reporting on high-cost HOA special assessments.

That pressure gets sharper when insurance doesn’t fully solve the problem. The same reporting notes that post-2025 storms led some Florida HOAs to levy average assessments of $5,000 to $20,000 per unit for roof and wind mitigation after insurers raised deductibles by more than 300%.

Boards in storm-exposed markets should assume this issue is no longer occasional. It’s structural.

What that means operationally

- Review policy limits and deductibles early: Don’t wait for a claim denial or a renewal shock.

- Prioritize resilience projects: Roof hardening, drainage work, water intrusion controls, and wind mitigation aren’t cosmetic.

- Model funding options before storm season: The best time to discuss cash needs is before the emergency.

A board that treats climate-related costs as unusual will keep getting cornered. A board that budgets for volatility will make better decisions.

New legal or safety requirements

Sometimes the community didn’t choose the expense at all. Changes in statutes, inspection requirements, or local enforcement can force expensive repairs or upgrades on a short timeline.

When that happens, the board still needs to communicate carefully. Owners may blame the board for the cost even when the board didn’t create the requirement. The cure is documentation. Show the legal trigger, the compliance deadline, the project scope, and the consequences of inaction.

Large capital improvements

Not every special assessment funds a crisis. Some fund major improvements that boards and owners believe will strengthen the community over time.

These situations require extra discipline because “nice to have” projects are much harder to defend than “must do now” repairs. If the board wants owner support, it needs a sharper case:

- Why this project now

- Why reserves shouldn’t fund it

- Why the cost allocation is fair

- What direct benefit owners receive

If the board can’t answer those questions cleanly, the project probably isn’t ready.

The Legal Process Boards Must Follow

A special assessment that feels necessary can still be legally defective. That’s the point many boards miss. Good intentions don’t cure bad process.

Start with the governing documents. Before discussing amounts, timelines, or owner messaging, the board must review the declaration, bylaws, rules, and any state-specific requirements that control assessment authority, notice, meeting procedure, and approval thresholds. Some communities allow the board to approve certain assessments on its own. Others require owner approval above a defined limit or for specific categories of spending.

The five legal principles boards should respect

For municipal special assessments, legal validity depends on five tests. The project must provide a unique and special benefit to the assessed properties, the determination of who benefits must be rational and fair, the fee must be proportional to the benefit received or costs imposed, the revenue must be used only for the project at issue, and similarly situated properties must be treated the same, as outlined by the Federal Highway Administration’s summary of special assessment validity standards.

For HOAs and COAs, boards should treat those principles as a practical legal standard even when the exact framework comes from municipal law. They point to the same conclusion: document the benefit, justify the allocation, and don’t use assessment proceeds loosely.

A defensible board process

This is the checklist I’d insist on if I were advising any board:

- Confirm authority in writing: Have counsel or management identify the exact governing document and legal provisions that authorize the assessment.

- Define the project precisely: Scope creep kills owner trust. Tie the assessment to a specific repair, replacement, or obligation.

- Document the funding gap: Show what reserves can cover, what insurance will cover if applicable, and what remains.

- Choose the allocation method carefully: Use the formula required or allowed by the governing documents, then test whether it is fair and supportable.

- Give proper notice: Owners need clear notice of meetings, votes, and payment obligations.

- Record the decision thoroughly: Meeting minutes should reflect the basis for the decision, alternatives considered, and the vote result.

Boards that want a useful reference point for condominium-specific considerations can review this discussion of condominium special assessment issues.

Process protects the board. Documentation protects the community.

When owner approval matters

Boards quickly get into trouble when they assume urgency gives them extra authority. Usually, it doesn’t.

If your documents or state law require owner approval above a threshold, get the vote. If emergency language applies, confirm that it actually applies to the facts in front of you. Don’t stretch an exception just because the regular process is inconvenient.

One example often cited in dispute discussions is California Civil Code §5605, which limits a board’s unilateral ability to levy certain larger assessments and gives owners a basis to challenge improper action in court. Even if your community isn’t in California, the lesson is universal: approval rules matter, and owners will challenge boards that ignore them.

Notice and recordkeeping are not clerical details

Boards sometimes treat notice and minutes as administrative housekeeping. That’s a mistake.

A clear record should show:

- Why the work is necessary

- What alternatives were considered

- How the amount was determined

- Why the allocation method complies with the documents

- What owners were told and when

If a dispute arises months later, memory won’t save you. The record will.

Calculating and Collecting Assessments Fairly

Boards usually spend too much time debating the total amount and too little time debating allocation. Owners notice the opposite. They want to know why their share is what it is.

The right allocation method depends on the governing documents first and fairness second. If your documents require a formula, follow it. If they allow discretion, choose the method that best matches the benefit received, the ownership structure, and the community’s long-term ability to defend the decision.

Common ways to allocate the cost

The verified legal framework for special assessments recognizes several allocation approaches. Costs may be divided by front footage, by the number of properties served, on a per-unit basis, or through a percentage surcharge tied to total property value or land value only, as noted earlier in the federal validity framework. In HOA and condo practice, that translates into a few familiar models.

| Allocation Method | How It Works | Pros | Cons |

|---|---|---|---|

| Per unit | Every unit pays the same amount | Easy to explain and bill | May feel unfair if unit sizes or ownership interests differ significantly |

| Square footage or ownership interest | Owners pay based on size or assigned interest | Often aligns better with shared ownership structure | Harder for owners to understand without a clear worksheet |

| Property value based | Higher-value properties pay more | Can appear equitable in mixed-value communities | More vulnerable to disputes if the project benefit isn’t closely tied to value |

| Front footage or properties served | Cost follows infrastructure exposure or service area | Strong fit for roads, utilities, or localized improvements | Can create sharp owner pushback if project boundaries are disputed |

What fairness looks like in practice

Fair doesn’t mean everyone pays the same. Fair means the board can explain why the method matches the governing documents and the underlying benefit.

Use these questions before finalizing the formula:

- Does the declaration already prescribe the allocation

- Does the project benefit all owners equally or differently

- Will similarly situated owners be treated the same

- Can the board explain the math on one page

If the answer to the last question is no, simplify the communication even if the formula itself must remain complex.

Collection policy matters as much as calculation

Once the assessment is approved, boards need a collection plan that is firm but workable. A vague due date and a generic invoice invite delinquency.

A sound collection structure should cover:

- Payment schedule: Lump sum, installments, or a structured temporary schedule

- Due dates: Specific dates, not open-ended language

- Late consequences: Whatever the governing documents and applicable law permit

- Owner communication: Written notices that explain how to pay, when to ask questions, and what happens if payment is missed

Boards also need accounting discipline. Special assessment income and project expenditures should be tracked cleanly so owners can see that funds are being used for the stated purpose. Associations that want stronger internal financial controls should pay close attention to accounting practices for homeowners associations.

A special assessment shouldn’t disappear into the general ledger like ordinary operating income. Owners deserve a clear financial trail.

Payment plans and enforcement

Offering payment plans can be smart governance when the documents and cash flow allow it. It may increase collections and reduce community friction. But boards shouldn’t confuse flexibility with inconsistency. If plans are available, the terms should be written, uniform, and enforceable.

If owners fail to pay, the board may have collection remedies under the documents and state law. Those can include late fees, liens, and in severe cases foreclosure. Because enforcement rights vary, boards should coordinate closely with counsel before escalating.

The principle is straightforward. Be humane in communication. Be consistent in policy. Be disciplined in enforcement.

How Special Assessments Affect Homeowners

For homeowners, a special assessment is immediate and personal. It competes with mortgage payments, insurance, utilities, school expenses, and everything else in the household budget. Boards that forget that human reality usually communicate badly and collect poorly.

Owners need direct answers. How much is due. When it’s due. Whether installment options exist. What happens if they can’t pay on time. Those are practical questions, not signs of resistance.

Budget pressure and owner behavior

Some owners can absorb an assessment with little disruption. Others can’t. The board has to plan for both.

When homeowners lack the financial capacity to absorb an added charge, delinquency risk rises and the community can face wider instability. Reserve Data Analysis notes that increased special assessments may contribute to delinquencies or even foreclosure when owners can’t manage the resulting payment burden, and that those financial stresses can ripple through property values and neighborhood stability, as explained earlier in that discussion of community impact.

That’s why collection strategy isn’t just an accounting issue. It’s part of asset protection.

Sales, disclosures, and buyer surprises

Special assessments also affect the transfer of property. During a sale, owners and buyers often assume the contract handles everything automatically. It doesn’t.

For municipal special assessments, payment responsibility depends on the contract. The seller may pay installments due before closing while the buyer assumes later installments, or the seller may have to pay the full remaining balance at closing. But those contract clauses do not govern HOA or COA special assessments. Unpaid HOA balances typically transfer to the new owner, which can create a surprise that affects marketability and financing, according to Berlin Patten’s explanation of special assessment responsibility in real estate contracts.

That distinction should change how boards handle disclosures.

What boards should disclose clearly

- Approved assessments: State the amount, due dates, and remaining balance.

- Pending discussions: If the board is actively considering a levy, minutes and resale materials should reflect that accurately.

- Collection status: Any unpaid balance attached to the property needs to be documented accurately.

- Project status: Buyers want to know whether the work is complete, underway, or still out for bid.

Boards should also understand that unpaid assessments can lead to lien activity depending on the documents and state law. Homeowners trying to understand that risk can benefit from a plain-language overview of homeowners association liens.

Property value isn’t a simple equation

Owners often ask whether a special assessment lowers property values. The honest answer is that it can, especially in the short term if buyers see the community as financially unstable or poorly managed. But the opposite can also be true when the assessment funds necessary repairs that preserve safety, appearance, and insurability.

The board’s conduct matters as much as the project itself. A community with a clearly justified assessment, strong disclosures, orderly collections, and visible project progress usually fares better than a community that looks confused, divided, or secretive.

Buyers can tolerate a well-managed capital project. They hesitate when they sense governance problems.

What homeowners should do when one is announced

Homeowners shouldn’t ignore the notice and hope the issue resolves itself. They should:

- Read the full assessment packet: Focus on project scope, payment terms, and legal authority.

- Review meeting minutes and financials: These documents often explain how the board reached the decision.

- Ask direct questions early: Waiting until the account is delinquent helps no one.

- Clarify sale plans immediately: Owners listing their property need to know how the assessment will appear in disclosures and closing discussions.

The most stable communities are the ones where owners get information early and the board answers with specifics instead of generalities.

A Board's Guide to Proactive and Transparent Governance

A special assessment is rarely just about concrete, roofing, drainage, or insurance. It’s a test of governance. Boards either prove they can lead through a difficult financial event, or they confirm every fear owners already have.

My opinion is simple. Most special assessment conflicts are preventable. Not because the cost can always be avoided, but because the distrust can.

Start communicating before the vote

Boards often wait until the amount is final and the notice is ready. That’s too late.

Owners need context before they get a bill. If the community is facing a major project, explain the condition issue, the urgency, the alternatives considered, and the likely funding paths while the board is still evaluating options. That doesn’t weaken the board. It strengthens legitimacy.

A good communication sequence usually includes:

- Early condition notice: Explain the problem and why action is under review.

- Project update: Share bids, professional opinions, or insurance developments.

- Decision notice: State the approval basis, amount, allocation method, and due dates.

- Ongoing progress updates: Show owners how funds are being used and how work is progressing.

Use plain language, not management jargon

Owners don’t need a vague message about “capital funding adjustments.” They need a straightforward explanation.

Bad communication sounds like this: “The board approved a special assessment due to reserve constraints.”

Good communication sounds like this: “The association must replace the failing roof sections this year. Reserves cover part of the cost. The remaining amount will be billed as a special assessment under the authority provided in the declaration.”

That second version answers the question owners ask, which is “Why am I paying this?”

Speak to owners like stakeholders, not obstacles.

Build a dispute process before you need one

Disputes over special assessments are common because owners often focus on perceived inequity, not just total cost. A particularly important point is dispute resolution. In California, Civil Code §5605 gives homeowners legal recourse if an assessment is improperly levied, and nationally 20% to 30% of community association disputes arise from perceived financial inequity. The same discussion notes that proactive transparency and clear communication are the strongest tools for preventing litigation, which can average more than $50,000 in legal fees, according to Pratt & Associates’ overview of California HOA special assessment challenges.

Boards should take that lesson seriously even outside California. You don’t need the same statute to face the same conflict dynamics.

A practical dispute protocol

- Invite written questions: Require owners to submit concerns in writing so the board can answer consistently.

- Centralize the record: One packet should hold the resolution, notice, budget support, project scope, and allocation worksheet.

- Use open meetings wisely: Let owners be heard, but don’t let meetings become rumor factories.

- Correct errors quickly: If a billing mistake or disclosure gap appears, fix it immediately and in writing.

Prepare for climate-related costs now

Boards that still treat climate resilience as a niche topic are behind. Weather exposure, insurance instability, and infrastructure stress are changing the financial profile of many associations. Even communities outside coastal zones are seeing more pressure around drainage, tree loss, exterior water intrusion, and carrier expectations.

The answer isn’t to panic. It’s to govern like these costs are recurring possibilities, because they are.

That means:

- Review reserves with a risk lens: Don’t evaluate only age-based replacements. Evaluate exposure-based repairs.

- Stress-test insurance assumptions: Deductibles and exclusions deserve board-level attention.

- Create owner expectations early: Communities tolerate hard costs better when the board has been candid for years, not days.

- Separate urgent repairs from long-range resilience work: Owners should understand which projects are emergency responses and which are strategic upgrades.

Trust is a financial asset

Boards often think of transparency as a courtesy. It’s not. It’s a collection strategy, a litigation defense, and a property value protection tool.

When owners believe the board has been candid, consistent, and disciplined, they may still dislike the assessment, but they’re more likely to comply with it. When they believe the board acted abruptly or selectively, every invoice becomes a political problem.

The best boards do three things relentlessly:

| Governance focus | What disciplined boards do | Why it matters |

|---|---|---|

| Communication | Share the reason, math, and timeline early | Reduces rumor-driven resistance |

| Documentation | Keep resolutions, bids, notices, and minutes organized | Supports enforcement and legal defense |

| Financial planning | Strengthen reserves after the crisis | Lowers the chance of repeat assessments for predictable work |

Special assessments in real estate are unavoidable in some communities. Chaos is not. Boards that lead with transparency, fairness, and evidence protect more than the balance sheet. They protect confidence in the community itself.

If your board needs experienced guidance on planning, communicating, and administering a special assessment, Access Management Group brings decades of condominium and HOA management expertise focused on protecting homeowners, supporting boards, and preserving community assets. The right partner helps your board stay compliant, stay organized, and make difficult decisions with confidence.