If you’re a homeowner in an HOA or condominium association, you’re familiar with regular dues. But every so often, your board may need to levy a special assessment. So, what exactly is it?

A special assessment is a one-time fee your association charges to cover a significant, unbudgeted expense that your regular dues or reserve funds can’t handle. It's a critical tool for preserving property values and ensuring the long-term financial health of your community.

Understanding the Role of Special Assessments in an HOA

Think of your regular association dues as the community's operating budget. They cover all the predictable, recurring costs—things like landscaping, pool maintenance, security, and insurance premiums. These are the expenses you and your board plan for year in and year out.

A special assessment, on the other hand, is for the big, unexpected financial hits. It’s like your family suddenly needing a brand-new roof after a major storm. It's an urgent, expensive project that your normal savings might not be able to cover on its own.

For your association, this could mean funding emergency repairs after a hurricane, replacing a failing community-wide plumbing system, or undertaking a major capital project that has reached the end of its life. A special assessment is the board's way of addressing large-scale needs that, if ignored, would cause property conditions to deteriorate and your home values to drop.

Differentiating Assessments from Regular Dues

To really grasp what a special assessment is, it helps to understand what it isn't. While both are financial obligations of owning a home in the community, their purpose, frequency, and scope are completely different.

A special assessment should be a rare, well-documented necessity, not a band-aid for routine budget shortfalls. As a board member, its legitimacy comes from addressing a specific, significant capital need that benefits the entire community and protects everyone's investment.

Regular dues fund the day-to-day operations and are collected on a set schedule. Special assessments are levied for a single, defined purpose, usually as a one-time charge (though payment plans are often an option for homeowners). One of the board's most important duties is to keep these two funding streams separate and clearly defined for all homeowners.

Effective leadership means transparently communicating this difference to all homeowners. This builds trust and helps everyone see why the extra fee is vital for protecting their shared investment. Board members carry a great deal of responsibility in these moments, and clear communication is essential. If you're on the board and want to learn more, our guide on HOA board member responsibilities is a great place to start.

Special Assessments vs Regular Dues at a Glance

To make the distinction crystal clear, here’s a simple breakdown of the two types of fees your association collects.

This table highlights how each fee serves a unique and important function in maintaining the community's financial stability and physical condition.

| Attribute | Regular Dues/Fees | Special Assessments |

|---|---|---|

| Purpose | To fund predictable, recurring operating expenses. | To fund a specific, large-scale, and often unexpected project or emergency. |

| Frequency | Collected on a regular schedule (monthly, quarterly, or annually). | Levied as a one-time charge for a defined event. |

| Scope | Covers ongoing services like landscaping, utilities, and management. | Covers capital improvements or major repairs like a new roof or elevator replacement. |

Ultimately, understanding the role of both regular dues and special assessments empowers homeowners and board members alike to make informed decisions for the good of the entire community.

When Special Assessments Become Necessary

In an ideal world, your community’s reserve fund would be a perfect financial shield, ready for any major expense that comes along. But reality has a way of throwing curveballs that even the most meticulous budget can’t predict. That’s when a special assessment may be unavoidable.

Levying a special assessment is a decision no board takes lightly. It's a last resort, triggered when the cost of a crucial project or emergency repair is far more than what’s available in the operating and reserve accounts combined.

Typically, this happens in a few key scenarios: emergencies, major system failures, or unforeseen legal demands. For instance, a hurricane tearing through a coastal community or a fire in a condo building can leave behind repair bills that absolutely dwarf the association's insurance deductible. In those moments, an assessment is often the only way forward to restore the property and keep it safe for everyone.

Identifying Common Triggers for an Assessment

While a natural disaster is a dramatic example, the most frequent reasons for an assessment are often things that build up over time—or fail without warning. We’re talking about the major shared systems that suddenly hit the end of their lifespan, often much sooner than expected.

Some of the most common triggers that force a board's hand include:

- Sudden System Failure: This is the abrupt breakdown of a critical community asset. Think of an elevator in a high-rise going out of service, a central boiler failing in the middle of winter, or a main sewer line collapsing.

- Urgent Structural Repairs: The discovery of major structural decay, serious foundation problems, or widespread water intrusion requires immediate, and often very expensive, work to protect the building's integrity.

- Unbudgeted Legal Costs: An unexpected lawsuit or a legal settlement can create a major financial liability that isn’t covered by the association’s D&O or other insurance policies.

What do all these situations have in common? They are urgent, expensive, and absolutely essential to the community’s well-being. Kicking the can down the road isn't an option, as delays can lead to even more damage, falling property values, or serious safety hazards.

The surest sign of a future special assessment is an underfunded reserve account. When an association's savings don't keep up with the projected aging of its major assets, a financial shortfall isn't a matter of if, but when.

This is exactly why a professional reserve study is one of a board’s most important tools. It acts as a long-term roadmap, giving you a clear picture of the life expectancy and replacement cost of every major community asset. Ignoring its advice is a fast track to a financial crisis.

The Link Between Reserve Funds and Assessments

A healthy reserve fund is your community’s first line of defense against special assessments. It’s a dedicated savings account for the big-ticket items—roofing, paving, siding, and other major capital components. When this fund is neglected, the association is left completely exposed.

For board members, the warning signs of a potential assessment are usually visible in the financials long before a crisis hits. A reserve fund that is consistently below 70% funded is a major red flag. This means the association doesn’t have enough cash on hand to cover the prorated portion of its depreciating assets, and that deficit just keeps growing.

This isn't just a local issue; it's a mechanism used nationwide. In all 50 U.S. states, special assessments are a legally authorized tool that allows property owners to fund localized projects that directly benefit them. These often cover 50% or more of costs for things like street paving, new gutters, and water systems. You can explore the legal framework of special assessments to see the broader context.

As a board member, your fiduciary duty is to keep a close watch on your community’s financial health and the physical state of its assets. By championing adequate reserve funding and taking the advice of reserve study professionals seriously, you can shield your fellow homeowners from the sticker shock of a surprise assessment and guide your community toward long-term stability.

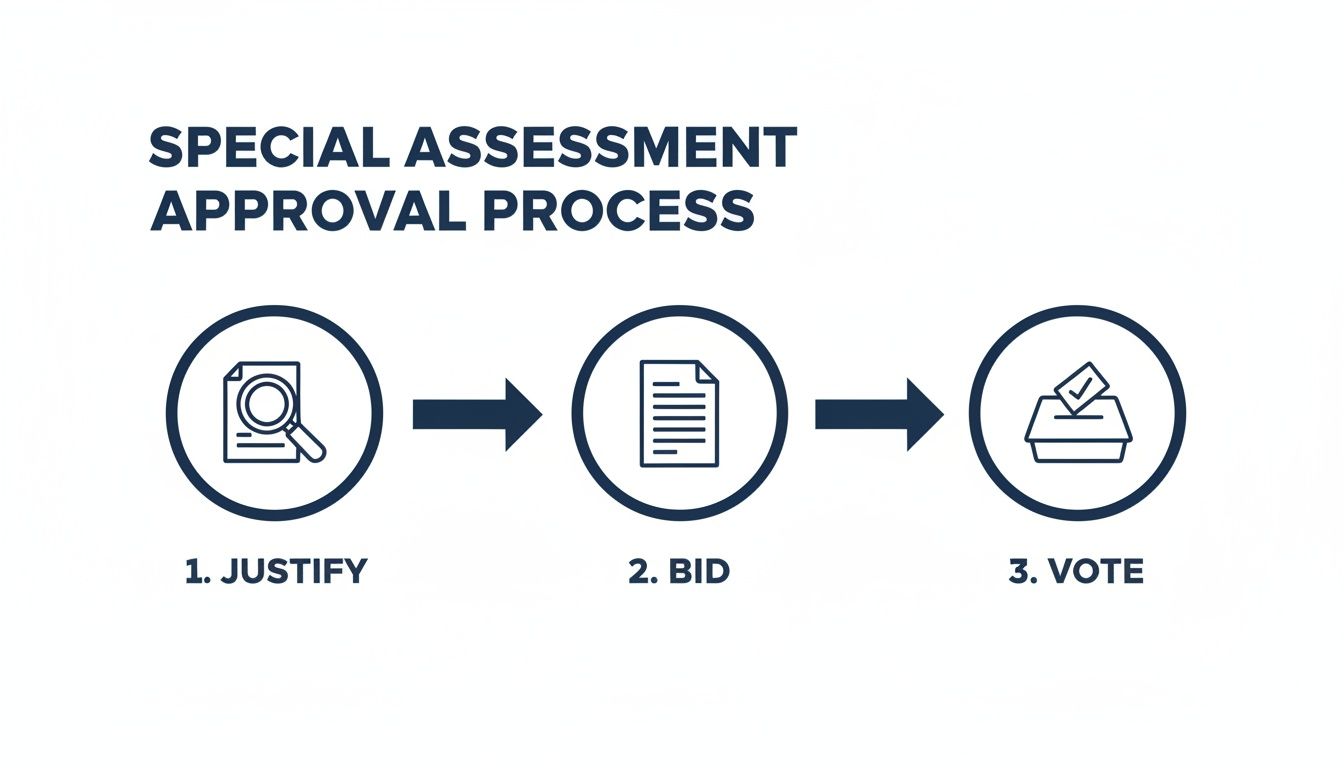

Navigating the Special Assessment Approval Process

Guiding your community through a special assessment is a major undertaking. It demands trust, complete transparency, and a strict commitment to your established procedures.

For any board, this is a high-stakes balancing act. One wrong move can quickly undermine homeowner confidence and open the door to legal headaches. A successful assessment isn’t just about getting a “yes” vote; it's about building a rock-solid, justifiable case that homeowners can actually get behind.

Think of it like you're presenting a critical business case to your shareholders—the homeowners. You have to meticulously document the need, prove you’ve done your homework, and follow every rule to the letter. This isn't just about compliance; it's about reinforcing the board's role as responsible stewards of the community's assets.

Step 1: Start with Your Governing Documents

Before you even think about drafting a notice or calling a meeting, your first stop is always a thorough review of the association’s governing documents. Your Covenants, Conditions, and Restrictions (CC&Rs) and bylaws are the official playbook. They dictate exactly how your association must operate.

These documents will spell out the non-negotiables:

- Voting Thresholds: What specific percentage of homeowner approval is required to pass a special assessment?

- Notice Requirements: How much advance notice do you have to give homeowners before the vote?

- Assessment Limitations: Are there any caps on the amount that can be levied without a homeowner vote? This is a common and critical detail.

- Meeting Procedures: What are the formal rules for calling and conducting a meeting for this purpose?

Ignoring these rules isn't a minor slip-up. It can invalidate the entire assessment, forcing the board to start from scratch and creating serious legal exposure.

Step 2: Build a Justifiable Case

Once you know the rules, your next job is to build an undeniable case for why the money is needed. Transparency is your best friend here.

The board should hold a meeting specifically to get the issue on the record. This is where you review professional opinions—like engineering reports or evaluations from contractors—and formally declare the need for the project.

This is also the time to get multiple, competitive bids from qualified and insured vendors. Showing up with a single bid can look suspicious and suggests the board didn't do its due diligence. Securing at least three competitive bids is a clear signal that the board is working to find the best value for the community, not just the easiest path forward.

The goal is to shift the narrative from, "The board wants more of our money," to, "Our community has a critical infrastructure need, and here is the most responsible plan to fix it." Making this shift is absolutely essential for getting homeowners on board.

Step 3: Prepare and Distribute a Comprehensive Notice Packet

With the need justified and bids in hand, the board must now create a formal notice packet for every single homeowner. This packet is your most important communication tool. It needs to be clear, thorough, and empathetic.

It should include:

- A Clear Explanation: Lay out the problem, the proposed solution, and why it can't wait.

- Total Project Cost: Present the full cost and provide summaries of the competitive bids you received.

- Assessment Calculation: Show homeowners exactly how the total cost breaks down and what their individual share will be.

- Payment Options: Clearly outline all payment methods, whether it's a lump-sum payment or an installment plan.

- Meeting Information: State the date, time, and location (or virtual details) for the vote, making sure you adhere to the notice period required by your bylaws.

Step 4: Comply with Georgia Legal Requirements

For any community in Georgia, following state law is not optional. Many modern HOAs operate under the Georgia Property Owners' Association Act (POAA). Even if your community isn't a POAA community, its rules are considered best practices for fair and effective governance.

The POAA gives associations the authority to levy assessments and provides significant power to enforce them, including placing a lien on a property for non-payment. This legal backing makes procedural correctness even more critical.

By ensuring your notice periods, voting methods, and meeting conduct align perfectly with both your governing documents and state statutes, you protect the board and the entire association from costly legal challenges. This deliberate, transparent process allows your board to confidently lead the community through the tough but necessary work of funding a special assessment.

Calculating and Communicating Assessments with Clarity

How your board calculates and communicates a special assessment is just as critical as the reason behind it. This is where trust is either built or broken. For homeowners, absolute transparency isn't just a nice-to-have; it's a requirement. And for the board, it's your best defense against disputes and legal headaches down the road.

The whole process—from justifying the need, to gathering bids, to holding a vote—has to be handled with care. It's all about building a logical, evidence-based case before ever asking your neighbors to open their wallets.

Following a clear, defensible process like this is fundamental to maintaining community trust and staying on the right side of your governing documents.

Common Calculation Methods

Once you have a firm project cost, the next step is figuring out how to divide that cost among the homeowners. Your community's governing documents will almost always dictate the method you must use.

The two most common approaches you'll see are:

- Pro-Rata (Equal Share): This is the simplest method by far. You take the total cost of the project and divide it equally among all units. It’s a great fit for communities with similar homes or where everyone benefits in the same way, like a new front gate.

- Percentage of Ownership: You'll see this method frequently in condominium buildings where units come in different sizes. The assessment is tied to each owner's percentage interest in the common elements. In short, owners of larger units pay a larger share of the cost.

No matter which method is used, the math needs to be straightforward and easy for any homeowner to double-check.

To see how this works in practice, let's look at a common scenario. Imagine a community needs a $200,000 roof replacement.

Sample Special Assessment Calculation

| Scenario | Total Project Cost | Number of Units | Calculation Method | Assessment Per Unit |

|---|---|---|---|---|

| Equal Share | $200,000 | 100 | Pro-Rata | $2,000 ($200,000 / 100) |

| Percentage of Ownership | $200,000 | 100 | Percentage Interest | Varies (e.g., a 1.2% owner pays $2,400; a 0.8% owner pays $1,600) |

This table shows how a simple pro-rata calculation results in a flat fee for everyone, while a percentage-based approach adjusts the cost based on ownership share.

Communicating with Empathy and Transparency

Announcing a special assessment can create a lot of anxiety for homeowners. A cold, demanding letter is only going to make things worse. The goal should always be to deliver the news with empathy, clarity, and as much detail as possible.

Think of the official notice less like a bill and more like a complete information packet. To ensure everything is accurate and compliant, we often advise boards to work with qualified CPAs when preparing these complex financial communications.

Here’s a good structure for your announcement:

- State the Purpose Clearly: Start by explaining exactly what the project is and why it has to happen now. Reference the professional reports or engineering studies that back up the board's decision.

- Show the Financials: Be upfront with the total project cost. It's also smart to include a summary of the bids you received and explain how the final contractor was chosen. This shows the board has done its due diligence.

- Explain the Calculation: Break down how each homeowner's share was calculated. Show the math, whether it's pro-rata or by percentage. Transparency is key.

- Provide All Payment Options: Give people clear choices. Is it a one-time lump sum? Can they pay in installments? If so, over what period and are there any administrative fees or interest?

- Outline the Timeline: Provide a clear schedule for both the payments and the project itself. Let homeowners know when payments are due and when work is expected to start and finish.

- Explain the Consequences of Non-Payment: This part can be uncomfortable, but it’s necessary. Gently but firmly state the legal process for non-payment as outlined in your governing documents, which may include late fees, interest, or even placing a lien on the property. This protects the association and is fair to all the members who do pay on time.

Getting these calculations and communications right is one of the board's most important duties. If you're looking for tools to make the job easier, you might want to explore the best HOA accounting software available to help manage these financial processes.

By providing clear, honest, and complete information, you empower homeowners to understand the situation and meet their obligations. This allows the board to lead with confidence and protect the community’s shared investment.

Let's face it: nobody likes a special assessment. It can put a real financial squeeze on homeowners, and for board members, it often feels like a last-ditch effort.

But demonstrating that you've looked under every rock for an alternative before levying that assessment? That’s the mark of a truly responsible board. It shows you’re a strategic steward of your community’s finances.

This section is all about those alternatives. We’ll walk through the most effective ways to manage your community’s funds proactively, making special assessments a genuine last resort, not a go-to solution.

The Best Defense is a Strong Reserve Fund

The single most effective way to sidestep a special assessment is to build and maintain a healthy reserve fund. Think of it as your community's dedicated savings account, set aside specifically for the big-ticket items down the road—roofs, paving, elevators, and other major assets.

When this fund is managed properly, surprises are few and far between. A special assessment usually only enters the picture when the reserve fund has been neglected or underfunded for years. The key to avoiding that pitfall is a regular, professional reserve study.

A reserve study isn't just a "best practice"; it's your community's financial roadmap. It gives you a detailed inventory of all major assets, their remaining useful life, and what it will cost to replace them, providing a clear guide for your annual budget contributions.

By following the recommendations of a reserve study and making those consistent contributions, you ensure the money is already there when a major component finally gives out. This proactive approach turns a potential financial crisis into a predictable, manageable expense, shielding homeowners from that sudden, large-scale bill.

Securing an Association Loan or Line of Credit

So what happens when an urgent need pops up before your reserves are fully funded? In this situation, securing a loan or a line of credit from a bank is a common—and often better—alternative to a special assessment.

Instead of hitting every homeowner with a large, one-time payment, the association takes on the debt itself. This allows the project to get started right away, while the cost is spread out over several years through much smaller, more manageable payments.

Just look at the difference from a homeowner’s perspective:

- Special Assessment: A homeowner might get a sudden bill for $5,000, due within 30 to 90 days. For most families, that's a significant financial shock.

- Association Loan: The board could instead increase monthly dues by $50 to $100 for a few years to cover the loan. That's a far more predictable and budget-friendly option for households.

A loan gives the board immediate access to capital while keeping the peace in the community. Of course, you have to factor in the long-term interest costs. But for many communities, the financial stability and reduced stress on homeowners are well worth the trade-off.

Understanding the Role of Assessments in Protecting Investments

While exploring alternatives is crucial, it’s also important to remember why special assessments exist in the first place. Historically, they have been a powerful tool for communities to fund improvements that directly protect and even enhance property values. As a board member, it's helpful to understand this context. A well-timed assessment can be a strategic move to preserve your community's real estate investments, much like the partnerships Access Management Group builds to elevate association assets with expert oversight and top-tier software. To learn more about this, you can read about how special assessments have shaped communities and see their historical impact.

Ultimately, the right path depends on a careful look at your community’s unique financial picture. By prioritizing a strong reserve fund and thoughtfully weighing options like association loans, your board can navigate major expenses with foresight and care, reinforcing your role as a trusted leader.

Navigating Homeowner Rights and Dispute Resolution

The secret to a smooth, legally-sound special assessment isn't just about the numbers—it's about the people. As a board member, being proactive and transparent from the very beginning is your best strategy. It prevents most disputes before they ever have a chance to start.

A successful assessment process is built on respecting homeowner rights. While your governing documents will spell out the specifics, a few rights are just part of fair, effective community governance everywhere.

Homeowners have the right to:

- Proper and Timely Notice: This isn't just a courtesy; it's a requirement. They must receive a complete notice packet well ahead of any meeting or vote, exactly as your bylaws dictate.

- The Right to Vote: If a vote is required for the assessment, every eligible member gets to cast their ballot. No exceptions.

- Review Relevant Records: Homeowners are entitled to see the project bids, contracts, and financial documents behind the assessment's cost. This kind of transparency is what builds trust.

A Proactive Approach to Managing Disputes

Even with the best procedures, disagreements can happen. Homeowner concerns about their finances are completely valid and should be met with respect and open communication, not defensiveness. How your board responds can either de-escalate tension or pour fuel on the fire.

The most effective way to handle potential disputes is to get out in front of them. We always recommend hosting a town hall or an open Q&A session focused only on the proposed special assessment. This gives homeowners a place to voice their concerns, ask tough questions, and hear directly from you. When the board presents a unified, informed front, it shows you've done your homework. For a deeper dive into these situations, you can learn more about condominium special assessments in our detailed article.

Answering questions proactively doesn't just solve one person's issue; it shows the entire membership that the board is listening and respects them. This simple act of open dialogue is your most powerful tool for building consensus.

Addressing Non-Payment with Fairness

Unfortunately, you will likely encounter homeowners who refuse or are unable to pay. It’s a tough situation, but the board has a fiduciary duty to the entire community to collect the funds needed for the project. This isn't about being punitive; it's about fairness to every member who does pay their share.

Your governing documents and Georgia law provide a clear, step-by-step process for collections. This usually starts with formal notices, then applying late fees or interest, and, as a last resort, placing a lien on the property.

A lien is a legal claim filed against the property for the unpaid debt. It ensures the association will get paid when the property is eventually sold or refinanced. By approaching this as a necessary, procedural step—rather than a personal battle—you can maintain a professional and objective tone throughout a difficult process.

Common Questions Boards Ask About Special Assessments

Even the most seasoned board members run into the same handful of tricky questions when a special assessment is on the table. Knowing the right answers isn't just about confidence—it's about making sure every decision your board makes is fair, legal, and defensible.

Here are the direct, no-nonsense answers to the questions we hear most often from the communities we partner with.

Can We Use a Special Assessment for Budget Shortfalls?

In almost all cases, no. A special assessment is a powerful tool, but it's meant for a specific, large-scale capital project or a true emergency. Think of it as the fund for replacing a failing roof, not a way to plug holes in the operating budget.

Using an assessment to cover things like a landscaping overage or higher-than-expected utility bills is usually prohibited by an association’s governing documents. More importantly, it’s a red flag for poor financial planning. The right move for a budget shortfall is to take a hard look at the annual budget, find places to cut costs, or propose an adjustment to regular dues for the next fiscal year.

What Happens if a Home Is Sold During an Assessment?

This comes up all the time, and it’s a critical one. A special assessment is tied to the property, not the owner. When a home with an active assessment is sold, that outstanding balance becomes a major negotiating point.

Typically, it gets handled in one of two ways:

- The seller pays the entire remaining balance of the assessment at the closing table.

- The buyer agrees to assume the rest of the payments after the sale is final.

This has to be clearly spelled out during the sales process and handled by the closing attorneys. Failing to disclose a pending or active special assessment can ignite serious legal fires after the sale. The new owner could rightly sue the seller for that undisclosed cost. Transparency isn’t just good practice here; it's a legal must.

A special assessment is a material fact that directly impacts a property's value. Sellers have a legal duty to disclose it, and savvy buyers are now doing their own homework, often requesting board meeting minutes from the past year to look for any whispers of a potential assessment.

Are Special Assessment Payments Tax-Deductible?

For the average homeowner, the answer is no—at least, not in the year you pay them. If the assessment is for your primary residence, you generally can’t write that payment off on your annual income taxes.

But there can be a tax benefit down the road. You are allowed to add the total amount of the special assessment to your home's cost basis. This officially increases the "cost" of your property, which can lower your capital gains tax bill when you eventually sell.

The rules shift if the property is a rental. In that situation, the assessment might be deductible as a rental expense. Tax laws get complicated fast, so homeowners should always consult a qualified tax professional to get advice for their specific situation.

At Access Management Group, our goal is to empower association boards with the knowledge and tools to lead effectively. We form a partnership with you to protect, preserve, and enhance your community’s real estate investments. Learn more about our approach at https://accessmgt.com.