You probably didn't run for the board because you wanted to spend your evenings reviewing bank reconciliations and vendor invoices. Then the election happened, people looked around the room, and suddenly you became treasurer.

That's common. So is the quiet panic that follows.

Most newly elected treasurers assume the job means personally handling every financial task. It doesn't. If you take that approach, you'll either burn out or start making avoidable mistakes. The role is bigger than bookkeeping and narrower than many volunteers fear. You are the board's financial overseer. Your job is to make sure the association's money is handled correctly, transparently, and in the community's best interest.

That distinction matters to homeowners, to the board, and especially to the president. A treasurer who understands the role creates order. A treasurer who tries to do everything alone usually creates bottlenecks, confusion, and risk.

Your Guide to Becoming an Effective HOA Treasurer

A newly elected treasurer often starts with two competing thoughts. First: “I care about this community, and I want to help.” Second: “Why did I agree to this?”

Both are reasonable.

Most volunteer treasurers step into the position because they're dependable, not because they're accountants. They inherit a stack of reports, passwords, invoices, reserve questions, and homeowner expectations. If the community uses a management company or outside bookkeeper, the treasurer may also wonder where their responsibility begins and ends. That confusion causes more trouble than the workload itself.

The right mindset is simple. You are not there to become the HOA's part-time data entry clerk. You are there to protect the association's assets and help the board make sound financial decisions.

That means asking better questions than “Did we pay this bill?” Ask, “Who approved it, was it within budget, and does the record support it?” Don't ask only, “What's the bank balance?” Ask, “Does this report reflect reality, and are reserves being protected?”

A strong treasurer makes the financial system reliable. They don't try to become the entire system.

If you remember one thing from this guide, remember this: hoa treasurer responsibilities are about oversight first, execution second. Some communities have managers, accountants, or bookkeepers doing the daily work. Fine. The treasurer still owns the responsibility to verify that the work is accurate, timely, and aligned with the board's duties.

That's how you reduce stress and actually lead.

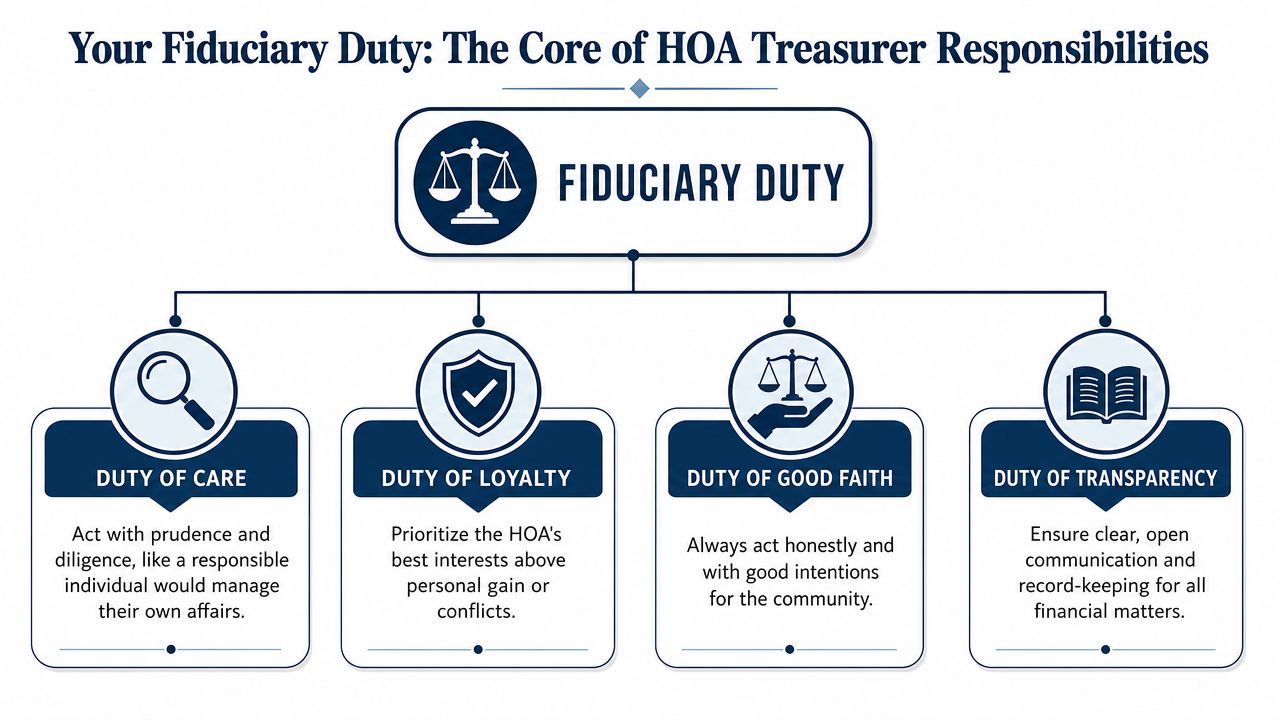

The Foundation Your Fiduciary Duty

The treasurer's authority starts with fiduciary duty. That phrase sounds legal and abstract, but the practical meaning is straightforward. You must act carefully, with integrity, and in the association's best financial interest.

Industry guidance describes the treasurer as the association's financial manager and custodian of funds, securities, and financial records, with responsibilities rooted in nonprofit-style oversight rather than ordinary bookkeeping, including budget preparation, dues collection, invoice payment, reserves oversight, and audit coordination according to Associa's overview of the HOA treasurer role.

Care means you verify

The duty of care means you don't rubber-stamp reports. You review them. You ask follow-up questions. You make sure the board gets complete financial information before it votes.

If a management company prepares the monthly package, your job isn't to thank them and move on. Your job is to read it. If expenses look off, ask why. If reserve transfers didn't happen, ask why. If assessments are lagging, ask what collection steps are in process.

Loyalty means the HOA comes first

The duty of loyalty means you put the association ahead of personal preference, neighbor pressure, and contractor relationships. You don't approve exceptions because someone is persuasive. You don't look the other way because a vendor is a friend. You don't keep quiet when the board is underfunding maintenance to avoid an uncomfortable dues discussion.

That principle is easy to understand outside the HOA world too. Families and trustees wrestle with the same obligation to secure family's trust future by acting for beneficiaries rather than themselves. An HOA treasurer should think the same way. The money is not yours. You are safeguarding it for the community.

Obedience and transparency keep you out of trouble

Use your governing documents, adopted policies, and professional advice as your guardrails. If your documents require board approval for certain expenses, follow that rule every time. If state law or your accountant requires specific records, keep them.

Use this quick check before approving any financial action:

| Question | Why it matters |

|---|---|

| Was it authorized properly | Prevents unilateral decisions |

| Is it documented clearly | Supports audits and owner trust |

| Is it in the HOA's best interest | Keeps loyalty where it belongs |

| Can I explain it at an open meeting | Tests transparency |

Practical rule: If you'd be uncomfortable explaining a transaction to the board or homeowners, stop and review it before it goes through.

Mastering the Financial Workflow

Money moves through an HOA in a cycle. Assessments come in. Bills go out. Accounts are reconciled. Reports are reviewed. Then the cycle starts again. If that workflow is sloppy, every board discussion becomes harder.

Start with the flow of cash

The cleanest way to manage hoa treasurer responsibilities is to follow the money in order.

- Assessments are billed and collected. Homeowners pay dues, late fees may apply under policy, and delinquencies are tracked.

- Deposits are recorded correctly. Payments must land in the right owner account and the right fund.

- Invoices are reviewed and approved. Vendor bills need backup, contract support, and proper authorization.

- Payments are issued. Checks or electronic payments should follow a documented approval path.

- Bank accounts are reconciled. Someone compares the books to the actual bank activity.

- The board reviews the results. Monthly statements should tell the board what happened and what needs action.

That flow sounds basic because it is basic. But basic doesn't mean automatic. Most financial problems in associations come from weak discipline around ordinary steps.

Put controls in place before you need them

A treasurer should insist on internal controls that make fraud and mistakes harder. In this way, oversight becomes real, not theoretical.

Use controls like these:

- Separate approval from processing: The person entering a payment shouldn't be the only person approving it.

- Require dual authorization: For checks or electronic payments, use a process that requires more than one set of eyes when possible.

- Match invoices to contracts: Don't pay from memory. Pay from documentation.

- Review bank reconciliations monthly: Reconciliation is how you catch errors before they become patterns.

- Keep a clear paper trail: Every transaction should have supporting records that another board member can follow.

A practical HOA accounting setup often includes software, standardized reports, and board review protocols. This overview of accounting for homeowners associations is useful because it frames accounting as a board-controlled process, not just a pile of transactions.

Watch the weak points

New treasurers often focus on whether bills got paid. That's too narrow. Focus on failure points.

Look closely at these areas:

- Delinquencies: Small collection issues become budget issues if ignored.

- Manual payments: Any payment process outside the normal workflow deserves scrutiny.

- Old outstanding items: Unresolved checks, credits, or open invoices often signal weak recordkeeping.

- Mid-year vendor increases: When service costs rise unexpectedly, the board needs fast visibility.

If you can't explain how a payment was approved, recorded, and reconciled, you don't have control of the workflow.

The goal isn't to micromanage staff or vendors. The goal is to make sure the system produces reliable financial records the board can trust.

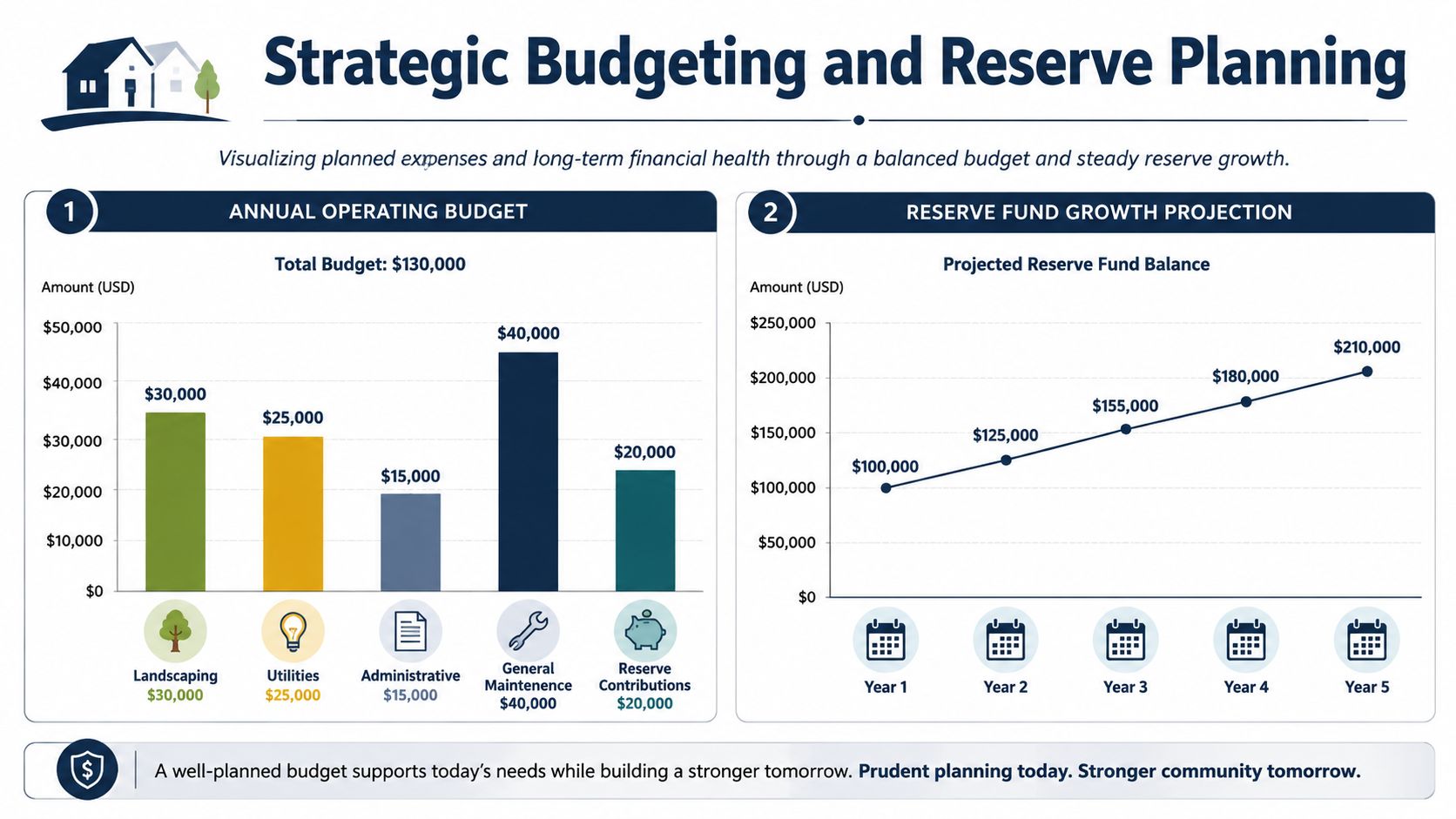

Strategic Budgeting and Reserve Planning

The annual budget matters. Reserve planning matters more.

Many boards spend too much energy debating minor operating line items and not nearly enough energy confronting future repair obligations. That's backwards. The association can survive a modest office supply overrun. It won't glide through a major capital need if reserves are weak and the board delayed reality year after year.

Build the operating budget with discipline

A good operating budget starts with actual obligations, not wishful thinking. Review recurring contracts, utilities, maintenance, administrative costs, insurance, and planned projects. Then ask where costs are likely to strain the budget.

Don't treat the budget as a political document designed to avoid complaints. Treat it as a financial plan designed to keep the association stable.

Use this budgeting lens:

| Budget question | Board-level purpose |

|---|---|

| What must be funded this year | Protects core operations |

| What costs are changing | Prevents surprises |

| What can wait, and what can't | Prioritizes maintenance intelligently |

| Are reserve contributions adequate | Protects long-term financial health |

Reserve funding is where treasurers earn their keep

Reserve planning is not optional. It is one of the clearest ways a treasurer protects property values and reduces owner conflict.

Industry guidance points to reserve funding as central to long-term health, and also notes that modern treasurers must manage rising financial risks such as inflation, higher repair costs, reserve shortfalls, and fraud controls like dual-authorization payments according to FS Residential's discussion of HOA treasurer duties.

If your community hasn't taken reserve planning seriously, the treasurer should push the issue. Politely if possible. Firmly if necessary.

A proper HOA reserve study gives the board a structured way to evaluate major common-area components, expected replacement timing, and funding needs. The exact figures will vary by community. The principle doesn't. If the association owns assets that wear out, the association must prepare financially before they fail.

Don't normalize special assessments

Some boards act as if special assessments are just part of HOA life. They shouldn't be the default answer to predictable deterioration.

When reserves are underfunded, owners get hit twice. First, through deferred maintenance and declining appearance. Second, through sudden financial demands that create anger and mistrust.

Reserve planning is the treasurer's strongest tool for preventing financial panic later.

Push for realistic contributions, regular review of reserve assumptions, and immediate board attention when vendor pricing or repair costs shift mid-year. That's strategic oversight. It protects homeowners from avoidable shocks.

Clear Reporting and Meeting Leadership

Treasurers don't just manage financial information. They translate it.

A board packet full of numbers won't help if nobody in the room understands what those numbers mean. Your job at meetings is to turn reports into a clear narrative about the association's condition, risks, and decisions.

What your monthly report should actually answer

At every regular board meeting, your financial report should answer a handful of practical questions:

- Do we have enough operating cash right now

- Are we performing in line with the budget

- Are assessments being collected consistently

- Are reserves being handled as planned

- Is there anything the board must act on this month

That's more useful than reading line items aloud.

Include the essentials in the board packet, such as the balance sheet, income statement or budget-to-actual report, bank reconciliation status, payables summary, and delinquency summary. Then explain the meaning, not just the mechanics.

For example, don't say, “Utilities are over budget.” Say, “Utilities are running above plan, so the board should watch the next quarter closely before approving any discretionary spending.” That gives the president and other directors something they can act on.

Speak to the board differently than you speak to homeowners

Boards need detail. Homeowners need clarity.

At board meetings, be prepared to answer follow-up questions about variances, collections, and contract expenses. At annual meetings or owner communications, simplify the message. Focus on the association's overall financial position, major priorities, and any upcoming decisions that affect owners.

This is also where transparency pays off. Owners don't expect a perfect year. They do expect honesty and understandable communication. If dues are rising or reserve funding needs attention, explain why plainly.

A related question many owners ask is whether HOA costs have tax implications for them personally. That's not the treasurer's job to answer definitively, but it helps to point people to a practical homeowner's HOA tax guide so they can discuss their own situation with a tax professional.

Run meetings like a financial leader

Use a simple verbal structure when presenting:

- Current position: operating cash, reserve status, major balances.

- What changed: important variances, delinquencies, unusual expenses.

- What needs attention: board approvals, policy decisions, or follow-up.

Homeowners trust boards that explain the numbers in plain English.

Keep the tone calm and direct. Don't hide problems, but don't dramatize them either. The treasurer who communicates clearly gives the entire board more credibility.

Working with Professional Partners and Tools

A volunteer treasurer should not be personally posting every receipt, preparing every reconciliation, chasing every delinquency, and assembling every report. That setup is fragile and unnecessary.

The smarter model is delegation with accountability.

What you should delegate

The treasurer is responsible for oversight. That doesn't mean doing every transaction by hand. In practice, many associations rely on managers, bookkeepers, outside accountants, or a combination of all three. That's often the most responsible choice because it creates continuity and stronger controls.

Here's a practical comparison:

| Task | Treasurer should oversee | Treasurer may personally do |

|---|---|---|

| Monthly financial review | Yes | Sometimes |

| Bank reconciliations | Yes | Sometimes, but not required |

| Vendor payment processing | Yes | Rarely the best use of time |

| Assessment tracking | Yes | Usually delegated |

| Audit and tax coordination | Yes | No |

| Budget and reserve strategy | Yes | Yes, with support |

If your association is still relying on one volunteer to manage everything in spreadsheets, that's not thrift. That's risk.

Choose partners based on role clarity

A CPA helps with tax filings, year-end review, and accounting guidance. A bookkeeper helps keep records current. A reserve professional helps the board plan for long-term capital needs. A community association manager helps coordinate the operational side so the board gets timely information and action items.

If you want a quick definition of that management role, this explanation of what a community association manager does is useful for board members who aren't sure where management ends and board oversight begins.

Here's the key distinction: delegation does not reduce the treasurer's duty. It improves the treasurer's ability to fulfill it.

Boardroom advice: Delegate transactions. Keep control of review, approval standards, and financial questions.

That means you should still review reports, verify controls, confirm account access, and insist on accurate meeting-ready financials. You just shouldn't be the only person capable of producing them.

Use tools that make oversight easier

A modern setup usually includes accounting software, owner payment systems, secure document storage, approval workflows, and recurring financial reporting. Good tools reduce dependence on memory and email chains.

This visual captures the experience many volunteer treasurers face when community finances start to consume more time than expected.

For boards that want management support, one option is Access Management Group, which states that it supports community associations with financial review guidance for board meetings, budget approval processes, and role discipline around board financial oversight. That kind of support can free the treasurer to focus on decision-making instead of transaction handling.

The test is simple. If your current process would collapse when one volunteer steps down, the process needs professional support or stronger systems.

Your HOA Treasurer Action Plan and Checklist

New treasurers need a short list of immediate actions, not another lecture. Start with control, visibility, and continuity.

First 30 days

Focus on handoff and access.

- Get every key record: Prior budgets, recent financial statements, bank information, contracts, reserve documents, audits, tax filings, and governing documents.

- Confirm access and authority: Know who can view accounts, approve payments, and sign on behalf of the association.

- Meet with the manager or accounting partner: Ask how dues are processed, how invoices are approved, and when reports are delivered.

A practical resource for effective nonprofit treasurer handovers can help you make sure nothing gets lost in the transition.

Days 31 through 60

Shift from gathering information to testing the system.

- Review the latest monthly package: Look for unexplained variances, old outstanding items, and missing reconciliations.

- Trace one payment from approval to bank clearance: This tells you more about internal controls than any verbal assurance.

- Review reserve contributions and major upcoming projects: Confirm whether the board is planning ahead or drifting.

Days 61 through 90

Now take your place as the board's financial leader.

- Present a concise monthly report: Explain what matters, what changed, and what needs action.

- Recommend control improvements: Approval workflows, documentation standards, or clearer reporting.

- Flag strategic risks early: Reserve strain, insurance pressure, or spending that doesn't match board priorities.

Your goal in the first few months isn't perfection. It's establishing a system where the board can trust the numbers, homeowners can understand the direction, and no single volunteer carries the whole burden alone.

If your board wants a more reliable financial process without dumping every accounting task on a volunteer, Access Management Group can help your association organize reporting, budgeting, and ongoing financial oversight so the treasurer can focus on protecting the community's assets rather than chasing paperwork.