Your renewal packet just landed in your inbox. The premium is up again. The deductible changed. The broker attached a schedule of buildings you haven't looked at closely in years. A homeowner is already asking whether the HOA covers water damage inside their unit, and your treasurer wants to know whether the budget can absorb another increase.

That's a normal board moment now.

If you're a new board president, HOA insurance begins to seem more significant than just insurance. It becomes a fiduciary duty issue, a budget issue, a homeowner communication issue, and sometimes a sale-approval issue. The mistake many boards make is treating insurance like a once-a-year renewal task. It isn't. It's one of the clearest places where your judgment affects every owner's financial exposure.

Why HOA Insurance Can Feel So Complicated

A new treasurer usually asks the same question first. “What are we required to carry?”

The frustrating answer is that there often isn't one neat rule you can pull off a shelf. In many U.S. states, the obligation for an HOA to carry insurance comes less from a single universal statute and more from the association's own governing documents, along with lender expectations and basic risk management practice, as noted in Goodwin & Company's HOA insurance overview. That's why two communities in the same city can have different insurance obligations.

Why boards get stuck

Most volunteer boards inherit coverage instead of designing it. They renew what the prior board bought, assume it must be correct, and only react when the premium jumps or a claim gets denied. That approach creates blind spots fast.

Complexity comes from four moving parts:

- Your documents: CC&Rs and bylaws often define what the association must insure.

- Your property layout: Roofs, hallways, pools, elevators, clubhouses, gates, and mechanical systems change the risk profile.

- Your ownership model: Condo and townhome communities usually have more shared insurance issues than detached-home HOAs.

- Your market reality: Some carriers are pulling back from certain risks, which means boards can't assume the ideal policy will always be available.

Practical rule: If the association maintains it, owns it, or can be sued over it, you need to know how it's insured.

What homeowners need from the board

Homeowners don't need a lecture on policy forms. They need a board that can answer plain questions clearly.

A strong board should be able to explain:

| Question from owners | What the board should know |

|---|---|

| Who insures the building? | Whether the master policy covers the structure and common areas |

| What do owners insure? | What each owner must carry for unit interiors, personal property, and loss assessment exposure |

| Why did premiums rise? | Whether the increase is tied to claims, market conditions, underwriting changes, or valuation updates |

| Could we face an assessment after a claim? | How deductibles and policy limits affect owner exposure |

If you can't answer those questions, you don't have an insurance problem alone. You have a governance problem.

Understanding The Two Layers of Protection

The cleanest way to understand HOA insurance requirements is to separate the community into two layers. The first is the association's protection for shared property and liability. The second is the owner's protection for what belongs inside the unit and around the owner's personal risk.

The master policy protects the box

Think of the HOA master policy as insurance for the building shell and shared spaces. That usually means the parts of the property the association is obligated to maintain and the places where the association can be held liable.

According to ROWCAL's HOA insurance guide, HOA insurance is a layered structure. The association's master policy covers common property and liability, while unit owners' HO-6 policies cover interior finishes and personal property. If you want a board-level explanation of how that master layer works in practice, this master insurance policy for homeowners association guide is a useful companion.

Typical master-policy territory includes:

- Shared structures: Roof systems, exterior walls, hallways, lobbies, and stairwells

- Amenities: Pools, clubhouses, fitness rooms, mail kiosks, and similar common elements

- Association liability: Incidents tied to common-area maintenance or association operations

The owner policy protects inside the box

The owner's policy is where a lot of confusion starts. Many residents assume the HOA policy covers everything tied to their unit. It doesn't.

Owners typically need their own policy for:

- Interior finishes: Drywall, flooring, cabinets, countertops, and fixtures, depending on the governing coverage form

- Personal property: Furniture, electronics, clothing, and other belongings

- Personal liability and loss assessment exposure: Especially where the HOA deductible or uncovered loss can be allocated back to owners

When a claim happens, most disputes don't start with bad intent. They start with people learning too late where the policy boundary actually sits.

Bare walls, single entity, and all-in

Boards require precision. The line between HOA and owner responsibility is commonly shaped by whether the master coverage is bare walls, single entity, or all-in.

| Coverage form | What it generally means for the HOA | What it means for the owner |

|---|---|---|

| Bare walls | Covers the basic structure and common elements | Owner carries more responsibility for interior components |

| Single entity | Covers the structure and some original fixtures or finishes | Owner still insures personal property and many interior exposures |

| All-in | Extends further into original unit components | Owner still needs coverage for belongings, liability, and possible gaps |

Boards need to stop speaking loosely here. “The HOA covers the building” is not enough. You need to know exactly how your documents and policy define that statement.

Essential Insurance Coverages for Every HOA

A serious board doesn't stop at property insurance. If all you buy is a master property policy, you've covered only part of the association's exposure.

Start with property and liability

Property coverage handles damage to insured common elements and structures. General liability addresses claims when someone alleges injury or damage tied to the association's responsibility. Those two coverages form the backbone of most HOA insurance programs.

Boards should pay close attention to replacement cost discussions here. If your insured values are stale, the community can discover the problem at the worst possible time. A practical way to think about rebuilding exposure is to review valuation assumptions against property-specific reinstatement concepts like those discussed in the Survey Merchant property guide.

Don't skip D and O coverage

Directors and Officers liability is one of the easiest places for a board to make a costly mistake. Volunteer directors can still face claims over elections, architectural decisions, enforcement, records access, or alleged failures to follow the governing documents.

If your board thinks, “We're careful, so we probably won't need it,” you're thinking like homeowners, not fiduciaries. D and O exists because even careful boards get challenged.

Crime coverage protects community money

A surprising number of boards focus on buildings and ignore cash controls. That's backwards. Associations collect assessments, hold reserves, and pay vendors. That makes them vulnerable to theft, fraud, and misuse of funds.

Crime or fidelity coverage matters because one dishonest act can destabilize owner trust just as fast as a property loss. A board that fails to carry it is leaving community funds exposed.

Workers' compensation depends on how the HOA operates

Some communities use only third-party vendors. Others have direct employees, on-site staff, or maintenance personnel. Your answer affects whether workers' compensation is required or functionally unavoidable.

This isn't a place to improvise. If anyone works directly for the association, the board should get a clear coverage determination from qualified insurance and legal advisors.

A practical way to rank coverages

Not every policy sits in the same category. Some are foundational. Others depend on your setup.

| Coverage | Why it matters | Board view |

|---|---|---|

| Master property | Protects shared buildings and common elements | Non-negotiable |

| General liability | Responds to common-area injury and damage claims | Non-negotiable |

| Directors and Officers | Protects governance decisions and legal defense | Non-negotiable in practice |

| Crime or fidelity | Protects association funds and financial integrity | Non-negotiable in practice |

| Workers' compensation | Addresses employee-related risk where applicable | Required based on operations |

Boards often ask which policy they can trim first. My answer is usually the same. Trim ignorance first. Know what each policy does before you cut anything.

Finding Your Insurance Mandates

If you want clarity on HOA insurance requirements, build a simple hierarchy. Start at the community level. Then move to legal requirements. Then confirm mortgage-market rules that can affect financing inside the association.

First check your governing documents

Your CC&Rs and bylaws usually tell you more than people expect. Search for terms like insurance, casualty, reconstruction, board authority, common elements, unit boundaries, and deductible allocation. That language often determines what the HOA must insure and what owners must insure separately.

This is also where boards need discipline. Don't rely on memory, old meeting minutes, or what a prior president said. Pull the documents and read the actual language.

Then identify state-specific obligations

State law may add requirements or shape how the documents are interpreted. Some states are more detailed than others, but even when state law isn't highly prescriptive, it can still affect how the board handles property insurance, liability, and claims responsibility.

The key distinction is this:

- What the association must carry: Coverage the HOA is obligated to maintain

- What the HOA can require from owners: Individual homeowner insurance, loss assessment coverage, or proof of coverage if authorized by documents or law

Boards routinely mix those up. Don't.

Lender rules are not optional if owners need financing

A board can ignore mortgage-market requirements only if it's comfortable hurting mortgage eligibility in the community. That would be reckless.

Fannie Mae requires master property policies for certain project developments to be on a replacement-cost basis and to include ordinance-or-law coverage, with boiler and machinery coverage required when central heating or cooling exists, as stated in the Fannie Mae Selling Guide for master property insurance requirements. Those are hard requirements tied to mortgage eligibility, not nice-to-have suggestions.

If your policy misses a lender-driven requirement, owners may feel the impact when they refinance, sell, or try to buy into the community.

Use a board worksheet

At your next insurance review, answer these questions in writing:

- What do our CC&Rs explicitly require?

- What does state law add or restrict?

- Do our current policies align with mortgage-market requirements for our project type?

- What are we requiring owners to carry, and do we have authority to require it?

That worksheet will do more for your governance than another vague renewal summary.

The Board's Role in Managing Insurance

Insurance oversight is a board job, not a broker job. Your broker advises. Your manager organizes. Your attorney interprets. But the board owns the decision.

Annual review is the minimum

Every year, the board should review the full insurance package, not just the premium page. That means looking at deductibles, named insureds, coverage forms, exclusions, valuation assumptions, schedules of buildings, and any material changes from the prior term.

This belongs on your board calendar alongside reserve planning and budget development. It's part of your core HOA board responsibilities, not an administrative side task.

Deductibles deserve board-level discussion

Too many boards focus on premium and barely discuss deductibles. That's backwards. The deductible is where your community's risk tolerance becomes real.

Ask direct questions:

- Could the association absorb this deductible without destabilizing operations?

- Would a claim trigger a special assessment?

- Do the documents allow allocation in a way the board understands and can defend?

A cheap premium paired with a painful deductible can turn one storm or plumbing event into months of owner conflict.

Vendor insurance controls matter

Every contractor and vendor working on the property should provide proof of insurance before work starts. That includes groundskeepers, pool companies, roofers, janitorial vendors, and maintenance firms. The board or management team should verify certificates and keep them current.

If a vendor causes damage or someone gets hurt, the association shouldn't be finding out after the fact that the paperwork expired.

Budget for reality, not hope

Insurance pricing has changed in many markets. Boards that budget based on optimism create avoidable surprises for homeowners. Build conservative assumptions into the budget and communicate early when market conditions are tightening.

One operational note. Some communities use outside support for claims review and insurance coordination. Access Management Group, for example, offers HOA management services that include insurance claims assistance and review, which can help boards organize documentation and carrier communication when claims become complicated.

The board's duty isn't to buy the cheapest policy. It's to make a defensible decision that protects owners, assets, and the association's financial stability.

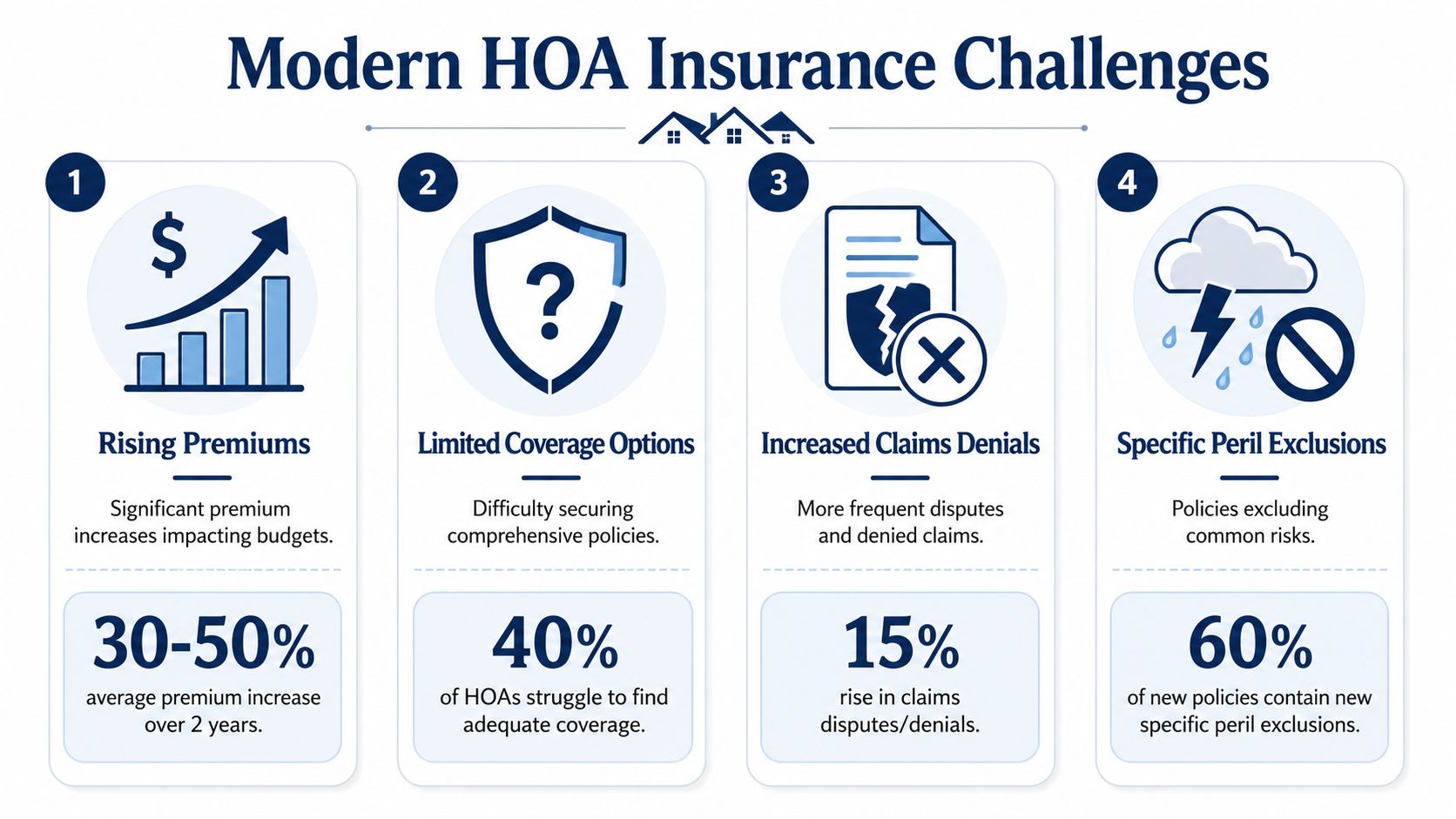

Navigating Modern Insurance Challenges and Pitfalls

A lot of old HOA advice assumes coverage is available if you're willing to pay for it. That assumption is no longer safe.

Availability is now part of the problem

A 2024 Minnesota survey found that HOA master insurance premiums increased sharply over a three-year study period, and that fewer insurers were willing to write HOA policies in the state, forcing some associations into secondary markets or resulting in denials of coverage altogether, according to the Minnesota HOA Insurance Survey Results. That should get every board's attention. This isn't just a pricing issue. It's an availability issue.

The same broader pressure shows up in high-risk markets where insurers tighten underwriting and boards struggle to secure replacement-cost coverage on workable terms.

Last-resort markets are expensive and narrow

When standard coverage becomes hard to place, some communities end up looking at FAIR Plans or similar last-resort options. Colorado's guidance notes that the FAIR Plan exists because traditional insurance is unavailable for some high-risk properties, and that it typically comes with higher premiums and limited coverage, as explained in the Colorado insurance availability advisory.

That means boards may be forced into layered solutions, higher deductibles, and more restrictive forms. The checklist mindset alone won't help you there. You need a financing strategy.

Risk control affects insurability

Boards can't control the market, but they can control preventable losses. Poor maintenance, repeat water intrusion, deferred repairs, and obvious trip hazards make renewals harder and claims uglier. For common-area injury risk, practical maintenance guidance like FMI's fall prevention guide can support day-to-day loss prevention.

If your community is already worried about a post-claim owner chargeback, this special assessment insurance and condo guidance is worth reviewing so the board understands how insurance gaps can become owner costs.

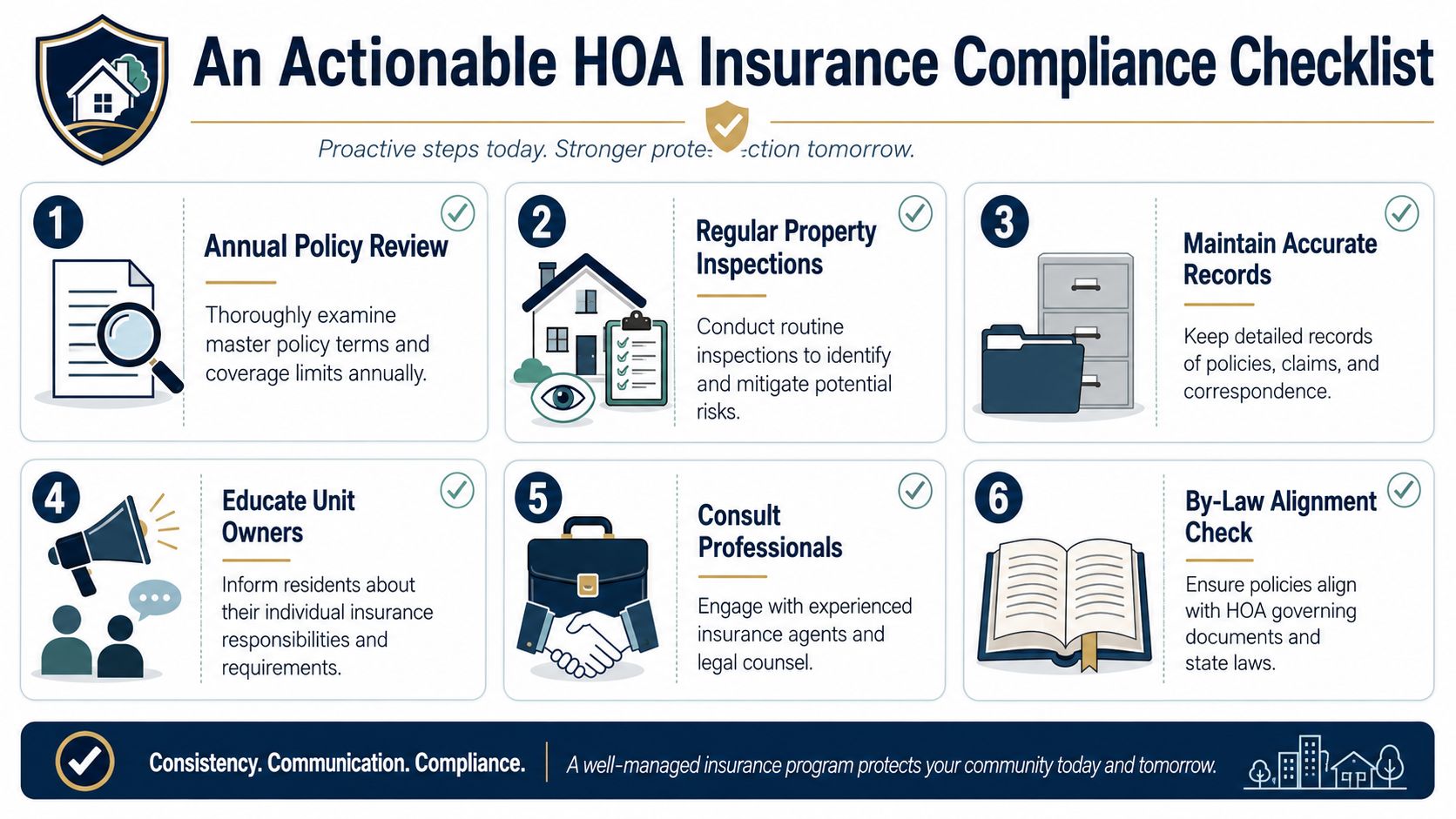

An Actionable HOA Insurance Compliance Checklist

Bring this list to your next board meeting and answer every item with a yes or no. If you can't answer yes, assign an owner and a deadline.

Board checklist

- Reviewed governing documents this year: Confirm the CC&Rs and bylaws still match the insurance program you carry.

- Confirmed policy structure: Know whether your master coverage is bare walls, single entity, or all-in, and make sure owners understand the boundary.

- Checked lender-sensitive requirements: Verify that replacement-cost treatment and any required ordinance-or-law or equipment-related coverage are addressed where applicable.

- Tested deductible exposure: Decide in advance how the community would fund a major deductible and whether owners could face an assessment.

- Verified supporting coverages: Confirm that liability, D and O, crime, and any workers' compensation exposure have been addressed.

- Updated building and asset schedules: Make sure the renewal reflects the property you have today, not the property the insurer listed years ago.

- Collected vendor certificates: Keep current proof of insurance for active contractors and service providers.

- Educated homeowners: Give owners a plain-language explanation of what the HOA insures and what they must insure themselves.

What a good board does next

Don't wait for renewal season. If your answers exposed gaps, fix them while you still have time to compare options, consult counsel, and communicate with owners before a crisis.

Good boards don't try to predict every claim. They make fewer unforced errors. That's what strong insurance governance looks like.

If your board wants help reviewing policies, organizing insurance responsibilities, and managing the operational side of community risk, Access Management Group can support that process with HOA and condominium management guidance designed for boards and homeowners.