A board usually learns about FHA condo approval the hard way. A unit goes under contract. The buyer is qualified. The closing date is on the calendar. Then the lender asks a simple question the association can't answer cleanly: is this project FHA approved right now?

When the answer is no, or worse, “it used to be,” the sale can stall or die. Homeowners feel that immediately. Sellers lose their advantage. Buyers walk. Board members get pulled into a preventable problem that looks like a financing issue but is really a governance issue.

An FHA approved condo isn't just a lending label. It's part of how a community protects marketability, supports resale demand, and shows that the association is managing the property and its finances with discipline.

Why FHA Condo Approval Matters More Than Ever

The practical value of FHA approval is simple. It widens the pool of buyers who can finance a unit in your community. For boards, that matters because buyer access affects how easily owners can sell, how long listings sit, and how much friction shows up during contract review.

That's why I treat FHA approval as an asset the association manages, not paperwork the association tolerates.

Approval lapses happen more often than boards think

Many communities assume that once they've been approved, they're covered. That assumption causes trouble. A 2018 HUD review of condominium approvals found that more than 41,000 projects had ever been approved as of April 2, 2018, but only 9,888 still held active approval, while 33,710 had lapsed. That means roughly 80% of previously approved communities had lost active status, and projects must reapply every 2 years.

That single fact should change how a board thinks about the issue. The question isn't only whether your community can qualify. The question is whether your board has a system to keep the approval from expiring unnoticed.

Practical rule: If your board only talks about FHA when a sale is in trouble, you're already behind.

For homeowners, this ties directly to value. Anything that narrows the buyer pool can affect liquidity. If your association also struggles with reserve planning, insurance renewals, or delinquency control, the problem gets bigger because lenders and buyers start seeing operational risk, not just financing inconvenience.

This is a board-level business decision

A president or treasurer should view FHA status the same way they view major contracts, annual budgets, and reserve planning. It has real operational consequences. It also touches many of the same inputs that shape condo HOA fee planning and owner expectations, because approval maintenance depends on steady financial governance, not last-minute cleanup.

What works is a board that asks early:

- Buyer access: Are we making it easier or harder for future buyers to finance here?

- Compliance discipline: Do we know our current status and expiration date?

- Financial readiness: Can we support the document requests and underwriting scrutiny without scrambling?

- Manager coordination: Does management track the metrics that usually create approval problems?

What doesn't work is assuming a lender, a seller, or a volunteer board member will somehow piece this together during escrow. By then, there's rarely enough time to fix the underlying issue.

Decoding FHA Eligibility Requirements

A board usually learns FHA standards at the worst time. A unit is under contract, the buyer needs FHA financing, and someone asks whether the project still qualifies. By then, the board is not just answering a lender question. It is exposing how well the association has handled occupancy tracking, collections, reserves, insurance, and records over the last few budget cycles.

The key thresholds boards need to know

FHA review focuses on a handful of project-level tests that boards should know before they submit anything. Common benchmarks include at least 50% owner-occupancy, no more than 15% of owners more than 60 days delinquent on assessments, and reserve funding of at least 10% of the budget. Some industry guidance also refers to 51% owner-occupancy for ongoing eligibility, and approvals generally must be renewed every 2 years, as explained in this overview of FHA condo approval benchmarks.

Those numbers matter, but they do not operate independently.

A community can hit the reserve contribution target on paper and still look weak if insurance deductibles are too high, deferred maintenance is obvious, or collections are inconsistent. A project can also meet the occupancy threshold one year and fall out of range the next if rental activity is not tracked carefully. Boards that treat FHA approval as a one-time filing miss the point. HUD approval depends on ongoing financial governance.

Where boards usually misread the risk

Owner-occupancy gets the attention because it is easy to talk about. The harder problems usually sit in the financials.

In practice, I see more approval trouble come from budget discipline than from any single leasing ratio. Rising insurance costs squeeze operating budgets. Reserve contributions get trimmed to avoid fee increases. Delinquencies linger because the board wants to be flexible. Each decision may feel manageable on its own. Together, they create a file that raises concerns for lenders and underwriters.

Review the project the way an underwriter would:

- Occupancy mix: Verify current owner-occupied and tenant-occupied units with actual records, not a stale roster or informal count.

- Delinquency control: Pull an aged receivables report and identify owners who are more than 60 days behind.

- Reserve funding: Confirm the adopted budget meets the reserve contribution standard and aligns with actual repair obligations.

- Insurance details: Check that master policy information, deductibles, and any required flood coverage are current and easy to produce.

- Project records: Organize amendments, policies, and other association records before the application starts. Boards that need to clean this up can start with these HOA governing document basics.

Associations rarely lose FHA eligibility because of one dramatic event. They lose it because small financial and administrative gaps are left in place until they show up in underwriting.

Today's pressure points are insurance and reserves

Insurance and reserves deserve special attention because they are where many boards feel the most pressure right now. Premium increases, higher deductibles, and reserve funding resistance from owners can push a community into short-term budgeting decisions that create longer-term financing problems.

That pressure shows up in several ways. Boards defer exterior work to hold dues flat. They underfund reserves because a special assessment feels politically harder. They renew insurance with narrower coverage because the premium is lower. Those choices may calm the next budget meeting, but they can weaken FHA eligibility and limit future buyers' financing options.

The practical takeaway is simple. If the association is struggling to fund reserves, maintain property condition, or keep insurance aligned with lender expectations, FHA approval is not just an application issue. It is a governance issue, and it needs board attention before a sale forces the question.

The FHA Application Process from Start to Finish

The application becomes manageable once the board treats it like a document project with assigned responsibility. Problems usually start when no one owns the process, deadlines are loose, and key records are scattered among prior board members, attorneys, accountants, and management files.

Start with a complete records pull

FHA review is project-level. The association generally needs to produce governing documents, budgets, insurance declarations, and supporting information about occupancy, delinquencies, litigation, reserves, and project condition. HUD forms are part of that package, including Forms 9991 and 9992. A current reserve study also matters, and guidance says it should be no more than 24 months old and comment favorably on structural integrity and the remaining useful life of major components, as outlined in this FHA condo document guidance.

That reserve study point deserves attention. Boards often think of reserves as an accounting topic. FHA treats them more like evidence that the association understands its physical plant and has a plan to maintain it.

Assign roles before anyone uploads anything

The cleanest applications usually divide the work this way:

- Board president or secretary: Confirms authority to proceed and signs where required.

- Treasurer: Verifies budget, reserve, delinquency, and financial statement accuracy.

- Community manager: Pulls governing records, insurance certificates, questionnaires, and owner occupancy data.

- Association attorney: Reviews legal disclosures, pending litigation issues, and opinion letter needs.

- Reserve specialist or engineer: Provides the current study if the existing one is outdated or inadequate.

If the board is using outside support, that can include a specialized consultant or a management partner that already handles lender questionnaires and association records. For boards comparing options, a condo association management company can help centralize records and coordinate the moving pieces, which is often where volunteer-led efforts bog down.

FHA condo approval document checklist

| Document Category | Specific Item Needed | Board Action/Note |

|---|---|---|

| Governing records | Declaration, bylaws, articles, rules, amendments | Confirm the latest recorded versions are included |

| Financials | Current budget, year-end financials, delinquency reports | Treasurer should verify consistency across reports |

| Reserves | Current reserve study | Replace it if it is older than 24 months or does not address major components clearly |

| Insurance | Master property, liability, and flood coverage if applicable | Ask broker for complete declarations and current evidence of coverage |

| Occupancy data | Owner-occupancy information | Use a current roster, not assumptions |

| Legal | Litigation disclosures, attorney input if needed | Identify active disputes early |

| HUD forms | Forms 9991 and 9992 | Complete carefully and keep backup support for each answer |

| Project condition | Maintenance records or supporting materials | Resolve obvious deferred maintenance before submission |

What makes an application move smoothly

A good package tells a coherent story. The budget supports the reserve contribution. The reserve study supports the maintenance plan. The insurance file is current. Delinquency reporting matches what management and accounting show. The occupancy data is recent enough to defend.

What doesn't work is mixing old and new records, sending incomplete insurance information, or guessing at occupancy numbers. That forces follow-up, and follow-up drags time.

“If the file feels disorganized to your own board, it will feel risky to an underwriter.”

Boards should also expect the application to take attention from multiple parties. Even when the forms themselves aren't complicated, gathering complete and internally consistent support takes discipline. The smoother path is preparation first, submission second.

Avoiding Common Application Rejection Reasons

A board usually learns about a weak spot at the worst time. The application is assembled, owners are asking when buyers can use FHA financing, and then the reviewer starts asking about reserves, insurance, delinquencies, or a lawsuit the board treated as routine. The rejection is not a paperwork surprise. It is an operating problem finally getting examined.

Financial weakness shows up first

The fastest way to lose credibility is to submit a file that says the community is stable while the budget, reserve funding, and insurance program suggest strain. Reviewers look for signs that the association can absorb pressure and still maintain the property. That matters even more now, because rising insurance premiums and reserve funding pressure are forcing boards into harder choices on dues, coverage limits, and repair timing.

I see one mistake over and over. Boards treat reserves, insurance, and collections as separate conversations. FHA review does not. A community with low reserves, premium increases, and growing receivables looks exposed, even if the grounds look good on inspection day.

The common trouble spots are familiar:

- Weak reserves: The board delayed contribution increases and now the funding plan no longer matches the property's repair obligations.

- Insurance gaps: The renewal was expensive, so the association accepted higher deductibles, lower limits, or incomplete supporting documents without measuring the approval risk.

- Collections slippage: Delinquencies grew because enforcement changed from case to case, or because the board avoided difficult owner conversations.

Good reporting helps boards catch these issues before the application exposes them. If your finance process needs work, outside guidance on how to unlock growth through financial reporting can also sharpen the discipline associations need around trend tracking, budget variance review, and decision-making.

Records and property condition can sink an otherwise eligible project

Some applications fail even when the finances are acceptable. The file is incomplete. The legal documents do not match the association's current structure. Insurance certificates are missing pages. Occupancy records are based on assumptions. The property shows deferred maintenance the board has been discussing for two years without acting.

Those issues matter because they raise a simple question for the reviewer. If the board cannot produce clean records or address visible repair needs, what else is being missed?

A few problem areas deserve special attention. Active litigation can create concerns about marketability and future cost. Leasing patterns that were never tracked carefully can create occupancy questions. Old amendments or missing recorded documents can make the submission look unreliable, even when the underlying issue is fixable.

What boards should fix before filing

Use the application as a stress test. If one of these issues is already on the board's agenda, solve as much of it as possible before submitting.

- Reserves below a defensible level: Update the reserve study or funding analysis, revise the budget plan, and prepare owners for higher assessments or dues if needed.

- Insurance program under pressure: Meet with the broker early, review full declarations and exclusions, and ask direct questions about property, liability, fidelity, and flood coverage where applicable.

- Owner-occupancy too close to the threshold: Tighten lease administration, clean up the unit roster, and stop relying on outdated owner questionnaires.

- Missing or inconsistent documents: Rebuild the official records set, including amendments, current budgets, financials, and signed disclosures.

- Deferred maintenance: Address life-safety, structural, water-intrusion, and obvious exterior deterioration first. Those are the items that make a reviewer doubt the board's stewardship.

- Pending litigation: Get association counsel's view on disclosure, financial exposure, and whether the case affects lending marketability.

Board perspective: Rejection usually confirms a management or governance problem that existed long before the application was filed.

The practical rule is simple. Do not submit just to test the file. If the board already knows the insurance renewal cut too much, the reserve study was ignored, or collections are drifting, the application will bring that weakness into full view. Boards protect approval odds, and protect property values, when they correct the underlying issue first.

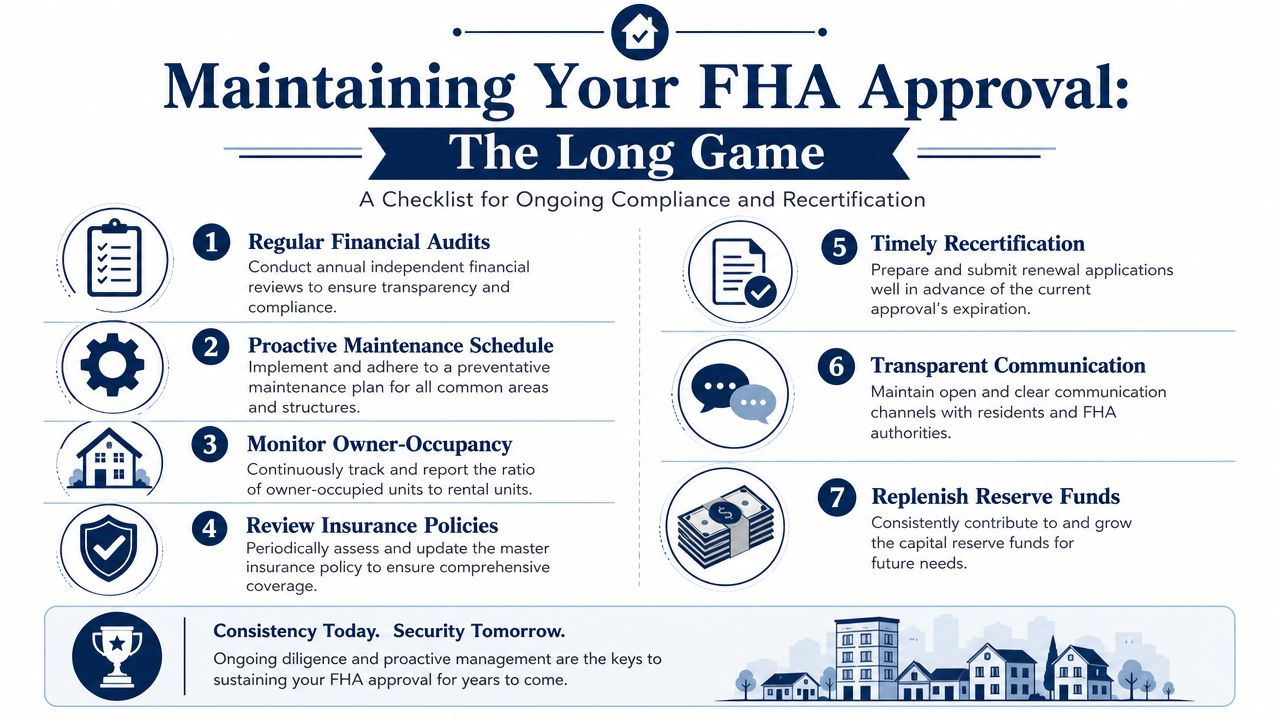

Maintaining Your FHA Approval for the Long Term

Approval is useful. Maintained approval is what protects owners.

Build an annual compliance rhythm

Because FHA approval must be renewed every 2 years, the board shouldn't wait for the expiration window to start asking questions. By then, it's too late for calm decisions. Good boards review the key risk areas during the year so renewal becomes an administrative task, not a crisis response.

A workable annual rhythm looks like this:

- After budget adoption: Confirm reserve contributions still support eligibility.

- After insurance renewal: Review coverage terms for gaps or changed limits.

- Quarterly: Check owner-occupancy tracking and aging reports for dues.

- After major repair planning: Make sure reserve assumptions and project condition still align.

- Before renewal season: Update the application file rather than rebuilding it from scratch.

Treat reporting as part of compliance

Boards maintain FHA readiness the same way they maintain any long-term financial standard. They use reporting, they compare actuals to policy, and they act before a problem becomes visible to outsiders. If your treasurer or finance committee wants a simple framework for how better reporting supports better decisions, this article on how organizations unlock growth through financial reporting is useful because the underlying discipline is the same.

That's the missing piece in many communities. They don't lose compliance because one board was careless. They lose it because the association never built a repeatable governance process around reserves, insurance, collections, and records.

Keep one standing agenda item each quarter for financing-readiness issues. That keeps FHA status tied to governance, where it belongs.

Your Board's Next Steps and FAQs

If your community hasn't checked its FHA status recently, the next board meeting should include a formal review. Start with current approval status, expiration timing, owner-occupancy data, delinquency reporting, reserve funding, insurance records, and the age of the reserve study. That conversation usually makes the path obvious. Either the association is close to ready, or it has cleanup work to do first.

A practical motion your board can use

A simple resolution can sound like this:

“Resolved, that the Board authorizes management and designated association advisors to evaluate project eligibility for FHA condominium approval or renewal, gather required records, identify compliance gaps involving reserves, insurance, delinquency, occupancy, and governing documents, and return to the Board with a recommended action plan and required budget implications.”

That language matters because it authorizes the work before a seller is in trouble.

Questions boards ask most often

Can a buyer get FHA financing if the project isn't approved?

Sometimes, through single-unit approval. But it's more limited than many owners expect. It still requires meaningful HOA cooperation and is constrained by project-level rules, making it less reliable than full project approval for many communities, as explained in this single-unit approval overview.

Should we handle the process in-house or hire help?

If your records are organized, your manager is experienced, and your financials are clean, in-house can work. If documents are fragmented, insurance is complicated, or the board is short on time, outside help is often worth it because coordination is usually the hardest part.

What should we review with our insurance broker first?

Ask for a complete summary of master policy coverage, endorsements, deductibles, liability terms, and flood coverage if relevant. For boards that want a homeowner-friendly explanation of how condo master coverage works, this insurance guide for NY condo residents is a helpful plain-English resource.

What if our reserves are weak right now?

Don't try to paper over it. Update the reserve study, revisit the budget, and decide whether higher dues, a special assessment, or phased capital planning is the honest solution.

How should owners be told about this?

Be direct. Explain that FHA approval supports resale flexibility, but maintaining it may require stronger financial discipline. Owners usually respond better when the board connects the policy choice to property value and saleability.

A board that handles this early does more than help one seller. It protects every owner's future exit options.

If your board wants a practical partner to organize records, coordinate lender and document requests, and help keep financing-readiness tied to everyday operations, Access Management Group can be part of that process. The key is to start before a sale is on the line.