You open the mail, see a notice from the association, and your stomach drops. The board has approved a special assessment, and every owner now owes a share.

That moment is why people search for special assessment insurance condo coverage in the first place. Owners want to know whether their own policy can help. Board members want to know how to reduce the chance of putting owners in that position at all.

Both questions matter because condo risk is shared. The association insures and manages the common property. The owner carries personal condo coverage. When either side leaves a gap, the bill often lands on the homeowner.

The Unexpected Bill Every Condo Owner Dreads

A special assessment is a bill the association charges owners when a major cost can't be paid through normal dues alone. In practical terms, it usually shows up after something expensive happens to the property, the association's reserves, or the association's insurance position.

For owners, the fear is simple. A large mandatory bill can hit with very little time to prepare. For boards, the pressure is different but just as real. They have to fund urgent repairs, protect the community, and make decisions that owners may understandably dislike.

Why this topic matters to both sides

Condo owners often assume their regular condo insurance automatically handles this risk. Often, it doesn't. The coverage owners need is usually loss assessment coverage, an optional add-on to an HO-6 condo policy that multiple insurers describe as protection when the association passes certain insured losses back to owners. One major carrier notes it can often be added for roughly $25 to $50 per year through a condo policy, which is why many owners consider it a practical safeguard in major condo markets, especially when a shared-area loss can trigger a large assessment through no fault of the individual owner. That summary is outlined in Hippo's explanation of condo special assessment coverage.

Practical rule: If you're in a condo, don't think of insurance as only "my walls and my belongings." Part of your exposure lives in the common property too.

The working definition you need

When people say "special assessment insurance," they're usually talking about the owner's loss assessment endorsement. It doesn't stop the board from levying an assessment. It gives the owner a way to transfer some of that financial risk to their insurer when the assessment is tied to a covered insurance loss.

That distinction matters. This isn't a magic shield against every association charge. It's a targeted form of protection for a specific kind of event.

Why Special Assessments Happen in Condominium Communities

Special assessments aren't unusual governance failures by default. They've been a standard tool in condo and HOA communities for decades, used when unexpected costs aren't covered by regular dues, reserve funds, or the association's insurance, as explained in this HOA insurance overview.

The cleanest analogy is a household emergency fund. If a family has enough savings for a broken water heater or a new roof, the expense is painful but manageable. If the savings account is too small, the family has to come up with money another way. Condo associations work the same way, just at building scale.

The three common drivers

Most special assessments come from one of a few practical situations:

- Insurance shortfall after a covered loss: The community suffers damage to common property, the master policy responds, but the policy limit or structure of coverage leaves part of the bill unpaid.

- A large master-policy deductible: The loss itself may be covered, but the deductible still has to be funded somewhere, and boards may allocate that cost to owners.

- Major non-insurance expenses: Capital repairs, infrastructure work, or other obligations can exceed what the reserve account can handle.

Boards don't levy these charges because they enjoy conflict. They levy them because vendors, carriers, and repair deadlines won't wait while the community hopes the problem disappears.

Why reserve planning changes everything

A well-run association treats reserves as the building's long-term repair fund. That means reality-based budgets, annual reserve funding, and regular review of reserve studies and insurance terms. When boards skip that discipline, they increase the odds of reactive billing.

If you want a plain-language explanation of how the board process works, this condominium special assessment guide is useful background for both owners and directors.

Think of reserves as the community's shock absorber. When they're thin, every major hit gets transmitted directly to owners.

What works and what doesn't

What works is boring, which is usually a good sign in property management. Consistent reserve contributions. Current repair planning. A realistic understanding of the master policy's deductibles and limits.

What doesn't work is assuming regular dues will somehow cover extraordinary costs, or assuming insurance will solve a maintenance problem that should have been funded years earlier. Insurance and reserves solve different problems. Communities get in trouble when they treat them as interchangeable.

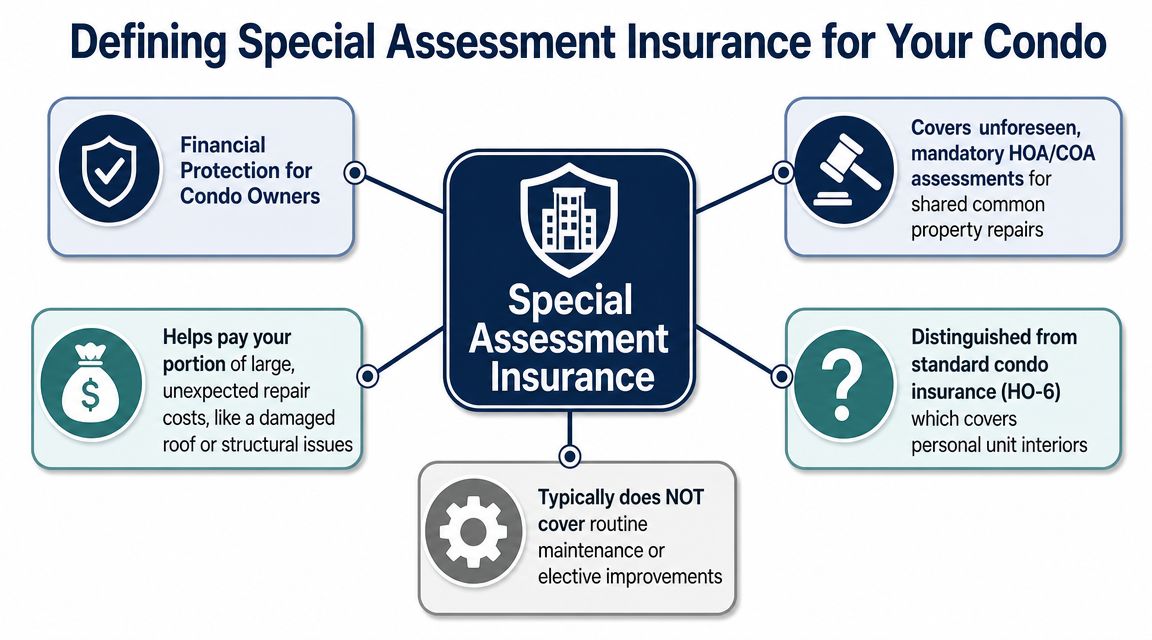

Defining Special Assessment Insurance for Your Condo

A board approves a special assessment after a covered loss, and owners immediately ask the same question: "Does my insurance help with this, or am I writing a check out of pocket?" In most communities, the answer depends on whether the owner added loss assessment coverage to the HO-6 policy.

Special assessment insurance condo coverage is usually not a separate policy. It is typically loss assessment coverage attached to an owner's HO-6 policy. That distinction matters for both sides of the table. Owners need to know what they have. Board members need to understand what owners may be relying on before an assessment notice goes out.

Its purpose is narrow but important. If the association levies an assessment because a covered loss to common property left a shortfall under the master policy, the owner's policy may pay that owner's share, subject to the endorsement's limit, deductible, and exclusions.

How the coverage fits into the bigger insurance picture

The cleanest way to explain it is by role. The association's master policy responds first to covered damage involving common elements and shared property interests. The owner's HO-6 policy handles the unit owner's personal property, interior responsibilities defined by the governing documents, and, if added, certain loss assessments passed through by the association.

That creates an important shared responsibility. Boards choose deductibles, limits, and claim strategy for the community. Owners choose whether to carry enough HO-6 protection to absorb their share if the association's insurance does not pay the full amount. One weak decision on either side can turn a manageable claim into a financial shock.

Condo insurance coverage at a glance

| Expense Area | Master Policy | Owner's HO-6 Policy (Standard) | Owner's HO-6 with Loss Assessment |

|---|---|---|---|

| Common-area building damage | Usually primary | Usually not primary | May help only if the owner's share is assessed after a covered loss |

| Interior unit property and personal belongings | Usually limited or not applicable | Usually the owner's responsibility | Usually the owner's responsibility |

| Association special assessment tied to covered common-area claim | May pay first up to policy terms | Often little or no meaningful protection for the assessment itself | Designed to help with the owner's allocated share, subject to policy terms |

| Routine maintenance or planned improvements | Not the purpose of insurance | Not covered as insurance | Generally not covered as loss assessment |

Where owners and boards get confused

Confusion usually starts when people treat every assessment as insurable. It isn't. Loss assessment coverage generally applies to assessments tied to a covered cause of loss, not to deferred maintenance, reserve shortages, or capital projects the association should fund through budgeting.

Water claims are a common example. Owners often focus on damage inside the unit, while the board is dealing with damage to shared building components and the association's deductible. Those are related problems, but they are not the same insurance claim. If you need to sort out the unit side of that question, this HO-6 policy water damage guide helps separate personal-unit coverage from assessment exposure.

Board members and owners should also read the master policy with the same level of attention they give the monthly budget. Deductible structure, valuation language, and coverage boundaries shape whether an assessment is likely after a claim. For a practical overview, review this guide to the HOA master insurance policy.

A good rule is simple. The master policy protects the community first. Loss assessment coverage helps protect the individual owner when part of that community cost is pushed down to the membership.

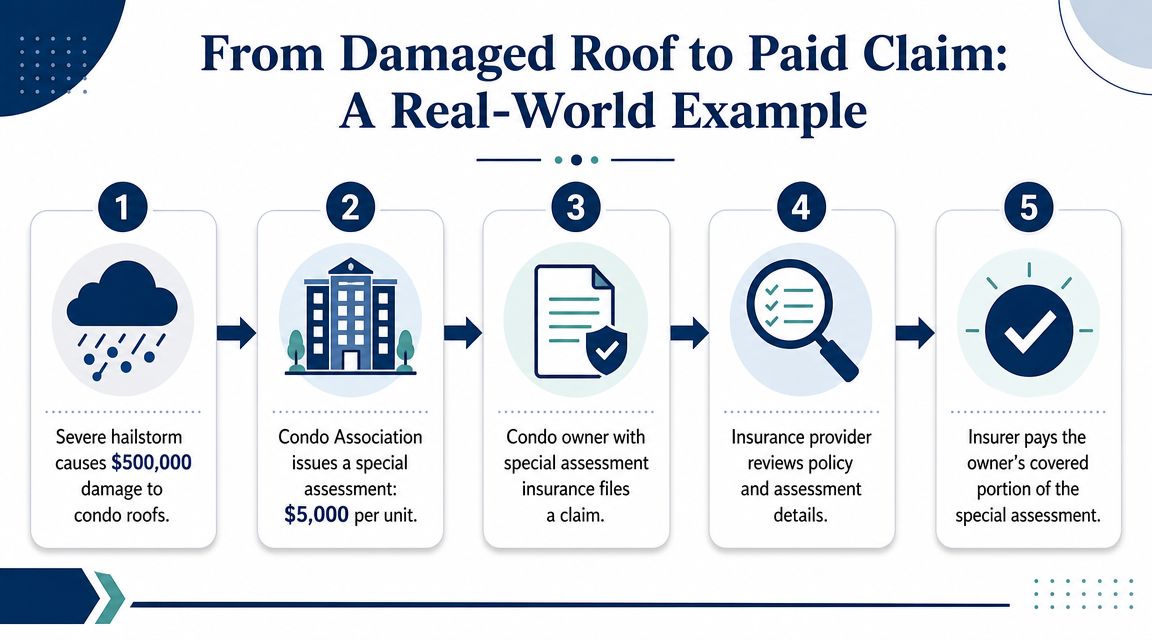

From Damaged Roof to Paid Claim A Real-World Example

A storm hits the community and damages the roofs on multiple buildings. The board reports that repairs will move forward under the association's insurance claim, but the master policy doesn't absorb the whole cost. Part of the funding gap has to be allocated to owners as a special assessment.

That's where theory becomes very real. The owner doesn't care whether the gap came from a deductible problem, a limit problem, or another covered insurance shortfall. The owner's question is, "Do I have coverage for my share?"

How the money path usually works

The sequence is usually predictable:

- A covered event damages common property.

- The association files a claim under the master policy.

- The master policy leaves a shortfall, often because of a deductible or an exhausted limit.

- The board allocates that shortfall to owners under the governing documents.

- An owner with the right endorsement files a loss assessment claim under the HO-6 policy.

The key trigger is coverage. According to GreatFlorida's discussion of special assessment coverage, loss assessment coverage responds when the assessment is tied to a covered peril, standard condo policies may include only a small default amount such as $1,000, and owners may be able to purchase higher limits up to $100,000.

What the owner needs to submit

In practice, the owner's insurer usually wants more than the assessment notice alone. A cleaner file often includes:

- The assessment letter: It should show the amount charged and why the board imposed it.

- Evidence of the master-policy claim: Owners often need confirmation that the assessment flowed from an insured event.

- A copy of the HO-6 declarations and endorsement: This confirms whether loss assessment coverage was purchased and at what limit.

- Board or management contact information: Adjusters often need to verify how the amount was calculated.

A lot of claims slow down because the paperwork comes in piecemeal. Boards can help owners by issuing clear assessment notices that identify the underlying loss and whether insurance was involved.

What can derail the claim

The most common problem is a mismatch between the assessment and the policy trigger. If the board calls something an assessment but it's really a maintenance catch-up or reserve issue, the owner's carrier may decline it. Another problem is low limits. An owner may have the endorsement but still find that the default amount doesn't go far.

That is why I tell owners to read the endorsement, not just the declarations page summary. The existence of loss assessment coverage is only half the question. The limit and the trigger decide whether it will be useful.

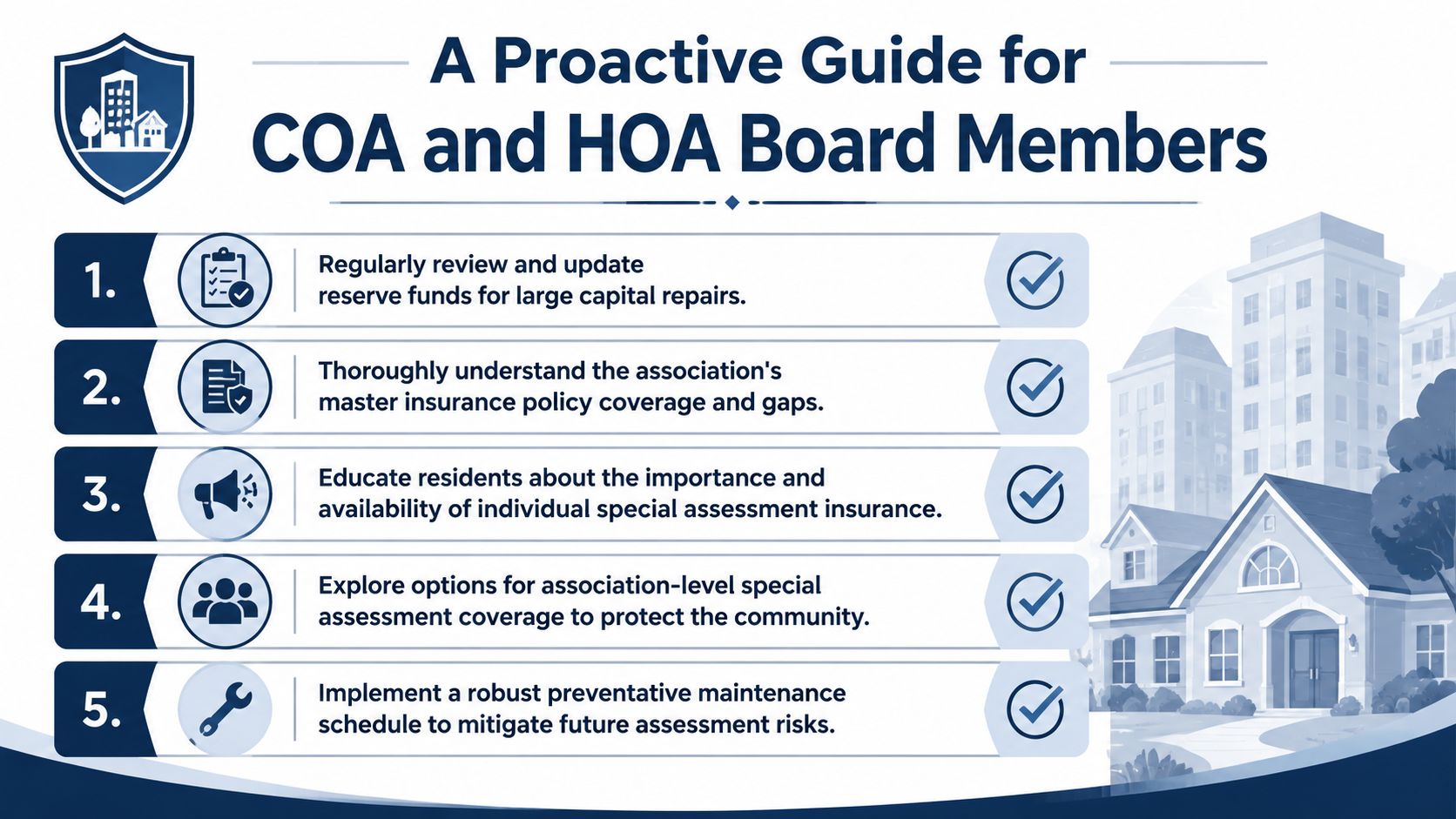

A Proactive Guide for COA and HOA Board Members

Boards have more influence over assessment risk than owners sometimes realize. Owners choose their own HO-6 limits, but the board controls the community's budgeting discipline, reserve posture, maintenance planning, and insurance review process. Those decisions shape whether a future loss becomes a manageable event or a community-wide financial shock.

Start with the real exposure

A board should ask a simple question at budget time. If we had a serious common-area loss tomorrow, where is the funding gap most likely to appear?

That answer usually depends on three inputs identified in Fuller Insurance's explanation of assessment-risk strategy: the master policy deductible, the severity of the loss, and the number of owners across whom that cost would be allocated. The practical takeaway is equally clear. Strong reserves and well-insured owners reduce the odds that a large repair turns into a one-time levy.

Five board actions that actually help

- Review reserves with discipline: Reserve funding isn't an accounting chore. It's the board's primary tool for avoiding surprise owner bills tied to predictable capital needs.

- Study the deductible structure: A master policy can look adequate at first glance and still create major owner pain if deductibles are high in the exact perils your property is most likely to face.

- Communicate in owner language: Don't tell owners only that the association is "properly insured." Explain where the master policy stops and where the owner's HO-6 begins.

- Track deferred projects accurately: When boards delay known repairs without a funding plan, they often turn future maintenance into future conflict.

- Encourage owner-side review: A board can't force every owner to buy more loss assessment coverage in most cases, but it can consistently educate owners about the risk.

Reserve studies are not optional in practice

If a board wants to reduce avoidable assessments, reserve planning has to move from annual ritual to operating discipline. A current reserve study helps directors understand what components are aging, when major expenses are likely to hit, and whether current funding is realistic. For communities that need a primer, this reserve studies resource for condominiums is a solid practical reference.

Good boards don't merely react well. They reduce the number of crises that require reaction in the first place.

What boards often get wrong

Some boards focus almost entirely on dues pressure and keep fees artificially low. Owners may like that in the short run, but the bill often shows up later in a less forgiving form. A community with weak reserves and a poorly understood deductible structure is one storm or one major claim away from a very unpopular assessment.

Other boards communicate too little. They assume owners don't want details. In reality, owners handle bad news better when they understand the numbers, the policy structure, and the alternatives the board considered.

The leadership standard owners remember

Owners don't judge boards only by whether an assessment happens. They judge them by whether the board saw the risk early, funded responsibly, maintained transparently, and explained the situation clearly.

That is fiduciary work in plain English. Protect the property. Protect the financial stability of the association. Give owners enough information to protect themselves too.

Your Action Plan as a Condo Owner

If you own a condo, don't wait for an assessment notice to figure out your coverage. Pull your HO-6 policy and look for the line item that refers to loss assessment. If you can't find it, ask your agent directly whether you have the endorsement or only the base policy.

The four questions to answer this week

Do I have loss assessment coverage?

Many owners assume they do. Some don't.What is my limit?

A low default amount may exist, but that doesn't mean it's enough for your building.What is my association's master-policy deductible?

Ask the board or manager for it in writing. That number gives context to your personal exposure.What kinds of assessments are likely in my community?

A newer property and an aging property can present very different risks.

What to ask your insurance agent

Keep the conversation direct. Ask whether your current endorsement is designed to respond when the association assesses owners because of a covered master-policy claim. Ask whether your current limit is likely to be meaningful given your community's deductible structure. Ask which documents the carrier would need if you ever filed a claim.

Then ask one more thing owners often miss. Ask what kinds of assessments your policy would not cover.

A practical owner checklist

- Get the governing facts: Request the association's master deductible and any owner insurance guidance the board has issued.

- Match your coverage to your building's reality: A generic limit picked years ago may not fit your current risk.

- Read your notices and meeting materials: Boards often disclose financial pressure long before an assessment is voted.

- Understand related board-side protections: If you're serving on the board or considering it, learn how Directors and Officers liability coverage fits into leadership risk. It's a different policy issue, but it matters when owners challenge board decisions.

A prepared owner is easier to protect. You can't control every association expense, but you can control whether your own policy leaves you exposed.

Frequently Asked Questions and Your Next Steps

Is every special assessment covered by my HO-6 policy

No. The most important trigger is whether the assessment is tied to a covered insurance claim. As explained in Progressive's loss assessment coverage guidance, assessments for deferred maintenance, underfunded reserves, or planned capital projects are common examples that are generally not covered.

How much loss assessment coverage should an owner buy

There isn't one universal answer. A sound approach is to compare your limit against the community's real exposure, especially the master deductible and the kind of common-area losses your property could face. If your current limit looks like an afterthought, treat that as a red flag and ask for options.

When owners say, "I have condo insurance, so I'm fine," they're often skipping the exact endorsement that matters for an assessment.

What's the first move for a new board president

Get three items on your desk quickly: the current reserve position, the latest reserve study or reserve planning documents, and the master policy summary with deductibles and limits. Those documents tell you where the next financial surprise is most likely to come from.

What if an owner's claim is denied

Start by comparing the denial reason to the actual basis for the assessment. If the issue is documentation or policy interpretation, the owner may need to challenge the decision through the carrier's review channels. For a practical overview of how that process typically works, this guide to NW Claims Management's appeal process for denied insurance claims can help owners understand the steps.

The next step for both audiences is simple. Owners should review their HO-6 policies and ask direct questions. Boards should review reserves, deductibles, and communication practices before the next loss tests the community.

If your community needs experienced guidance on reserve planning, insurance coordination, budgeting, and day-to-day governance, Access Management Group is a trusted resource for condominium and homeowner associations. Their team has long focused on helping boards protect property values, reduce financial surprises, and serve homeowners with practical, steady management.