You're probably dealing with one of these boardroom moments right now: a proposed rental restriction, a reserve funding debate, a roof responsibility dispute, or a question about whether your documents still make sense for the mix of homes in your community. That's when the usual buyer advice about privacy, yard space, or “investment potential” becomes useless.

For a board, the single family vs multi family home question is really about control, cost, and risk. It affects who maintains what, how insurance is structured, how reserves should be funded, what kind of owners buy into the community, and how quickly small problems turn into expensive association problems.

If you're a board member or president, you shouldn't treat property type as a background detail. You should treat it as an operating system. A detached-home HOA, a townhouse association, and a condominium building may all look like “residential communities,” but they don't function the same way. If you govern them the same way, you'll make bad policy.

Understanding the Stakes for Your Community

Single-family housing still dominates the national housing mix. In the U.S., detached single-family homes represented roughly 64% of all housing units, while multifamily accounted for about one-quarter of the housing stock according to Statista housing stock data. That matters because most boards operate in markets where both forms exist side by side, compete for buyers differently, and place very different demands on associations.

A board doesn't get to stay abstract about this. If your community is evaluating redevelopment nearby, rewriting maintenance standards, or arguing over reserve contributions, property type shapes the answer. It shapes resident expectations too. Owners in detached-home communities usually expect more personal control. Owners in condos and other multifamily settings usually live with more collective decision-making whether they like it or not.

Here's the cleanest way to think about it: the more shared structure a community has, the more operational risk moves from the owner to the association.

| Attribute | Single-Family in an HOA | Multi-Family in a COA |

|---|---|---|

| Primary ownership focus | Home and lot | Interior unit plus shared interest |

| Association role | Common areas and community standards | Building systems, structure, common elements, and standards |

| Typical risk concentration | More individual owner responsibility | More collective responsibility |

| Reserve pressure | Often centered on amenities and site assets | Often centered on major building components |

| Board workload | Architectural control and covenant enforcement | Maintenance planning, insurance, projects, and owner coordination |

Boards that ignore housing type usually end up reacting to crises instead of governing with a plan.

The practical takeaway is simple. Don't ask only what kind of homes you have. Ask what responsibilities the property type pushes onto the association, and whether your governing documents, budget, and management practices match that reality.

Defining the Landscape for Association Governance

The physical appearance of a property doesn't tell the board enough. Governance depends on ownership boundaries, maintenance boundaries, and insurance boundaries.

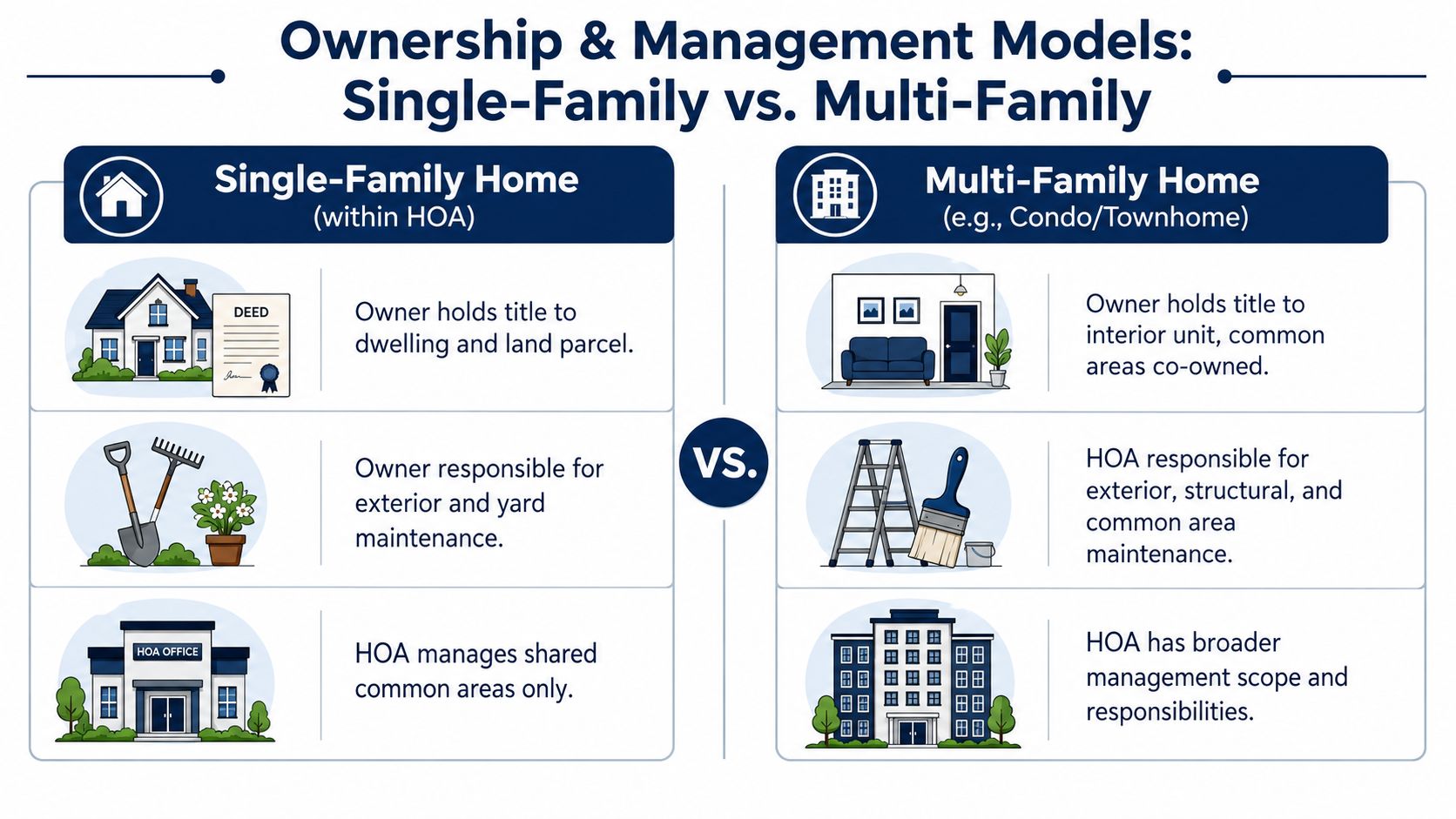

Single-family detached and attached homes

A single-family home is usually one dwelling for one household. In community associations, that can include a detached house on its own lot or an attached home such as a townhouse where the owner may still hold title to the structure and parcel. From the board's perspective, that usually means the owner carries more day-to-day responsibility for the building itself, while the HOA governs common areas, amenities, and use restrictions.

That sounds simple until the documents muddy it. Some attached single-family communities push roof, siding, or landscaping work onto the association. Others leave nearly all exterior work with the owner. Two communities can look almost identical from the street and operate completely differently on paper.

Multifamily and condominium structures

A multifamily building is different because the ownership model often slices up the property. A condominium owner commonly owns the interior unit and shares ownership in common elements such as roofs, exterior walls, hallways, parking areas, and structural systems. That changes everything for the board.

The board in a condo or multifamily setting isn't just enforcing appearance standards. It's helping direct building operations. It has to plan for common systems, coordinate repairs that affect multiple homes at once, and make decisions that directly affect habitability, insurability, and resale friction.

Why legal labels matter more than visual labels

A lot of board confusion starts when people use architecture terms as if they were legal terms.

- Townhouse may describe how a home looks, not who owns the roof or land.

- Condominium usually describes a legal ownership structure, not a building style.

- Duplex or small multi-unit property may still be treated differently depending on ownership structure and program rules.

Practical rule: Never let the board decide responsibility based on appearance. Check the declaration, plat, maintenance exhibits, and insurance provisions first.

When you hear phrases like walls-in or studs-in insurance, that's the warning sign that boundaries matter. Your documents decide where the association's responsibility begins, where the owner's responsibility ends, and where disputes will start if the documents are vague.

Ownership and Management Models Compared

The most important difference in the single family vs multi family home debate isn't aesthetics. It's who controls the risk.

The core governance issue is whether the property sits inside a common-interest structure that shifts maintenance standards, reserve obligations, and operational control to the collective. HUD guidance makes that distinction clear in practice, and it's why boards need to think beyond casual labels when evaluating how a community functions under ownership and program rules, as noted in HUD guidance on property eligibility and structure.

Governance model comparison

| Attribute | Single-Family (in an HOA) | Multi-Family (in a COA) |

|---|---|---|

| Title ownership | Owner often holds title to home and lot | Owner often holds title to unit interior and shared interest in common elements |

| Exterior maintenance | Frequently owner-driven, unless documents assign otherwise | Frequently association-driven |

| Structural responsibility | Often individual owner | Often collective through the association |

| Operational risk | More dispersed among owners | More concentrated at board and association level |

| Dispute pattern | Lot lines, use restrictions, architectural issues | Leaks, noise, insurance, system failures, shared repairs |

What changes for the board

In a single-family HOA, the board's role is narrower. It usually focuses on covenant enforcement, architectural approvals, amenity oversight, and common-area maintenance. That doesn't make the job easy, but it does mean many building-level failures remain the owner's problem first.

In a multifamily condominium or similar setup, the board inherits a broader management burden. A roof problem isn't one owner's headache. A plumbing issue can affect stacked units. Deferred maintenance doesn't stay isolated. It spreads.

That's why boards in multifamily settings need tighter operating discipline. They need stronger work order processes, more explicit maintenance charts, clearer insurance coordination, and managers who understand where the association's authority begins. A qualified community association manager helps translate those legal boundaries into operating procedures the board can use.

My recommendation to boards

Stop using generic terms in meetings. Say exactly what you mean.

- If the owner holds the lot and structure, treat maintenance allocation differently.

- If the association controls shared building elements, budget and govern like an infrastructure operator.

- If your community mixes product types, don't force one policy onto all homes without checking whether that policy shifts costs unfairly.

In detached-home communities, owners often absorb more building risk. In condos, the board often inherits it whether the board planned for it or not.

Many boards get into trouble when they write rules as if everyone owns the same thing. They don't.

A Board's Guide to Financial Implications

Most board conflict that looks like a “policy problem” is really a financial structure problem. Single-family and multifamily communities don't just spend money differently. They accumulate risk differently.

Financing rules affect your buyer pool

Unit count changes financing treatment. One-unit homes are single-family. Properties with 2 to 4 units are generally treated as residential for underwriting. Properties with 5 or more units are typically treated as commercial multifamily, with stricter underwriting and more complex compliance according to Rocket Mortgage's overview of single-family vs multifamily financing.

Boards should care because financing rules shape resale conditions. Stricter lending treatment can narrow the buyer pool. A narrower buyer pool can affect turnover, investor concentration, and owner stability inside the community.

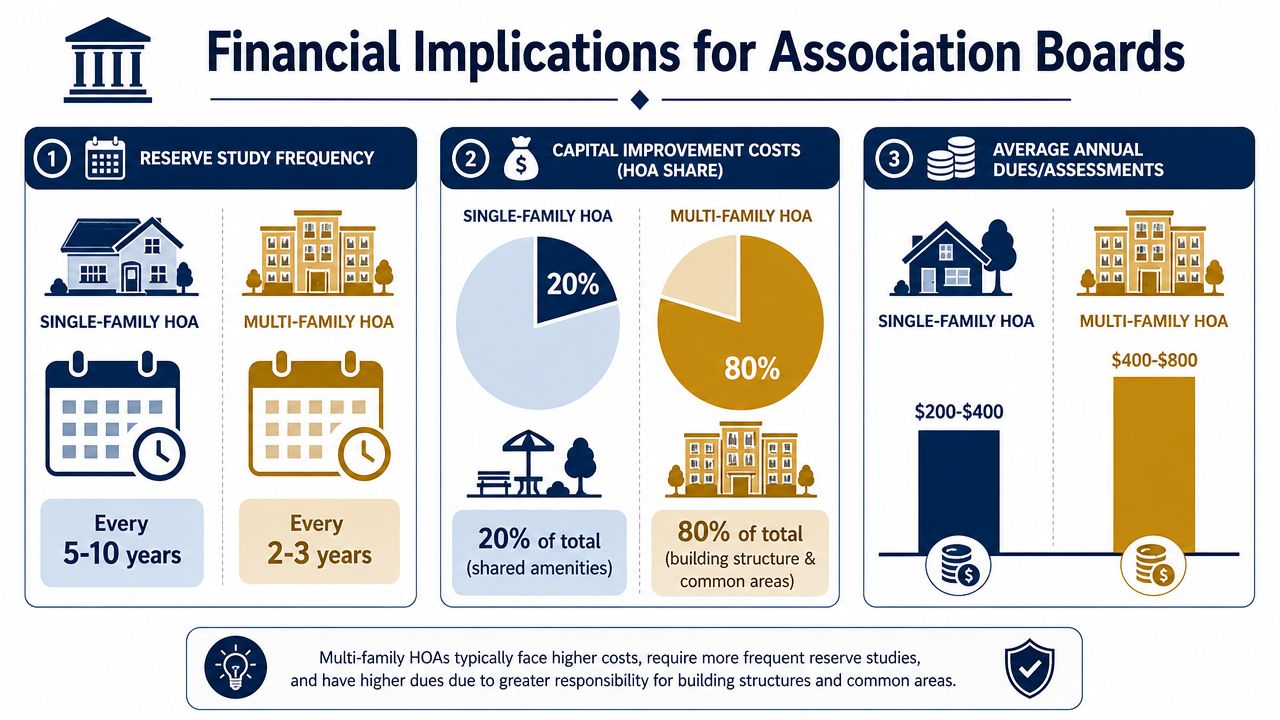

Reserve planning isn't remotely the same

In a detached-home HOA, reserve planning often centers on roads, stormwater systems, clubhouses, monuments, gates, pools, and other shared assets. The association may carry significant obligations, but they're often spread across site infrastructure and amenities rather than stacked building systems.

In multifamily and condo communities, reserve pressure is more concentrated. Roof assemblies, exterior envelopes, elevators where applicable, mechanical systems, and common structural elements create bigger collective obligations. If the board underfunds reserves in that environment, the consequences hit faster and more visibly.

Here's the blunt advice: if your association controls major building components, weak reserve funding is governance malpractice.

Insurance has to match the ownership map

Master insurance only works when it matches maintenance and ownership boundaries. If your declaration says the association maintains the roof, exterior, or shared systems, your insurance review should track that. If the owner is responsible for interior finishes or temporary housing after a covered loss, owners need to understand that too.

When boards discuss claim scenarios, it helps to review practical explanations of homeowners ALE coverage details so owners understand where personal loss-of-use coverage may fit alongside the association's master policy. That conversation reduces anger later, especially after fire, water, or storm losses.

The accounting recommendation

Boards need separate discipline in three areas:

- Reserve allocation: Match reserve components to actual governing-document responsibility.

- Insurance review: Confirm that policy scope aligns with maintenance obligations.

- Financial reporting: Present building obligations clearly enough that owners can see what dues are funding.

If your board needs tighter controls around reserve schedules, assessments, and reporting, use structured HOA accounting practices instead of letting the budget evolve by habit.

Navigating Zoning and Rental Regulations

Zoning and rental pressure can change a community's character faster than most boards expect. Detached-home communities often feel insulated until nearby density changes traffic, parking demand, and amenity use. Multifamily communities feel those pressures sooner because more residents typically share more limited common infrastructure.

The harder issue is rentals. Boards often debate rentals as a values question. They should treat them as an operational question first.

Why multifamily attracts more investor attention

Multifamily has a basic investment advantage: income diversification. In a single-family rental, one vacancy means a 100% loss of rental income until the property is re-leased. In a 10-unit multifamily building, one vacant unit reduces gross scheduled income by about 10%, and a three-month vacancy equates to roughly a 2.5% annual vacancy rate for the property, according to LoopNet's multifamily versus single-family investment analysis.

That stability often attracts more investor owners. Boards need to be ready for that. Investor-heavy communities usually experience more turnover, more leasing questions, and more strain on enforcement consistency.

What boards should regulate

Rental policy has to match the property type and the governing documents. Don't copy another community's rule because it “worked for them.”

Focus on enforceable issues:

- Lease administration: Require lease submissions, occupant registration, and current contact information.

- Standards enforcement: Make owners responsible for tenant compliance, fines, and damage reimbursement where documents allow.

- Occupancy and use limits: Align rules with municipal requirements and your declaration.

- Parking control: In denser settings, parking abuse becomes a governance issue quickly.

- Communication protocols: Tenants need rules access, but owners need accountability.

If your board hasn't reviewed these basics recently, start with your HOA governing documents. Rental restrictions fail when they conflict with the declaration, ignore amendment requirements, or create rules the board can't enforce consistently.

A rental policy that looks strict on paper but collapses in enforcement is worse than a simpler rule the board can actually apply.

My view on rentals

Boards should stop arguing in slogans. “Investors are bad” isn't a policy. Neither is “owners should be free to do what they want.” The central question is whether the community has the administrative structure to handle leasing without damaging compliance, maintenance, and neighbor confidence.

Impact on Long-Term Community Value

Boards often talk about value as if it means sale price alone. That's too narrow. Community value comes from stability, predictable maintenance, insurability, sensible rules, and visible stewardship over time.

Housing trends matter because they change the competitive environment around your association. According to HUD housing start data for 2025, single-family starts fell by 6.9% while multifamily starts grew by 17.4%. Boards should read that as a market signal, not trivia. Demand can shift toward denser and often more rental-oriented housing even while traditional single-family construction cools.

What that means in practice

If your community is mostly single-family, more multifamily supply nearby can change buyer expectations. Prospective owners may compare your amenities, maintenance standards, parking rules, and dues against denser alternatives. If your community is multifamily, additional supply can increase competition and raise the importance of clean common areas, project timing, and visible reserve discipline.

Boards can't control local construction trends. They can control whether the community looks organized, funded, and well maintained.

Value is operational

A community preserves value when the board does these things well:

- Maintains visible assets consistently: Deferred exterior work signals disorder fast.

- Funds reserves credibly: Buyers and lenders pay attention to financial health.

- Enforces standards evenly: Selective enforcement undermines confidence.

- Plans projects before failure: Emergency governance is expensive governance.

Exterior presentation still matters. In detached-home and attached-home communities alike, simple site improvements can reinforce owner confidence and curb appeal. Practical ideas like the landscaping and exterior upkeep tips in this property value advice from Richmond Tree Experts can support the board's broader maintenance strategy when applied within the association's standards.

My recommendation to boards

Don't chase appreciation. Protect function.

Communities hold value when boards manage boring things well: reserves, repairs, rules, records, and expectations.

That's the unglamorous truth. Owners notice it. Buyers notice it. Lenders and insurers notice it too.

A Decision Framework for Association Boards

A board meeting goes sideways fast when the room is arguing about fences, roofs, and parking, but nobody can say with confidence who owns the problem, who pays for it, or whether the rule can be enforced. That is how associations create avoidable conflict, uneven assessments, and expensive cleanup later.

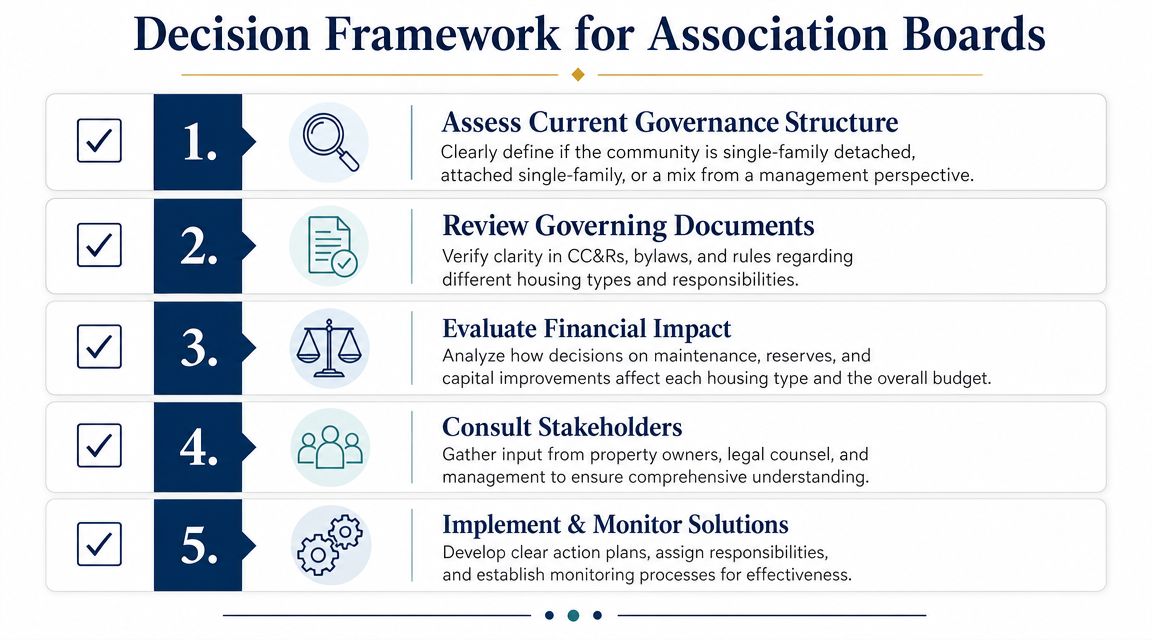

Use a decision framework. Use it every time.

Five questions that keep boards out of trouble

What exactly is the ownership model?

Read the governing documents and confirm what each owner owns. In a detached-home community, that may include the lot and structure. In a condominium, it may stop at the unit boundaries. In a mixed community, the answer can change by building type, which means the board cannot write one rule and assume it applies evenly.Who is responsible for maintenance right now?

Do not rely on board memory or management habit. Check the declaration, plats, maintenance matrix, and insurance language. If your board cannot answer who handles roofs, siding, drainage, stoops, or private drives without debate, you do not have a governance opinion problem. You have a document control problem.Does the decision allocate cost fairly?

Boards often make avoidable mistakes in this area. A policy can look uniform on paper and still push more cost onto one ownership type than another. Before you approve a rule, ask which owners benefit, which owners carry the expense, and whether your documents support that allocation.How does this affect marketability and occupancy patterns?

Board decisions shape who buys, who rents, and how lenders view the community. That matters more in attached and multifamily settings, where underwriting, investor concentration, and rental demand can shift quickly. For outside context on where multifamily demand is concentrating, boards and managers can review BatchData market analysis tools.Can management administer the rule without confusion?

If enforcement depends on exceptions, side agreements, or a longtime volunteer explaining the “usual practice,” the policy is not ready. A workable rule is clear in the documents, easy to explain to owners, and simple to enforce the same way every time.

A board meeting checklist worth using

Before any vote, run through this list:

- Confirm document authority: The board cannot fix a structural ownership issue with a casual policy.

- Identify the insurance effect: Maintenance responsibility and insurance responsibility often track together. If you change one, review the other.

- Price the long-term obligation: If the association takes on repair or replacement responsibility, reserves and annual budgets must reflect it.

- Test enforcement mechanics: Decide who will inspect, what counts as a violation, what notice goes out, and how the record will be kept.

- Write the owner explanation before the vote: If the board cannot explain the rule in plain language, owners will not understand it after adoption.

One more standard matters. Put the decision in writing with the reason for it. Future boards need a record of why the association chose a maintenance boundary, funding method, or use restriction. Without that record, the same argument returns every few years.

The recommendation I give most often

Govern by property structure, document authority, and operating capacity.

That means legal review when ownership lines are unclear, reserve analysis when responsibility shifts, and management input before the board adopts a rule it expects staff to carry out. Access Management Group is one example of a community association management company that supports boards with administration, budgeting, and governance execution, but the larger point is simple. Boards need a repeatable process, not improvised decision-making.

Strong boards make fewer dramatic mistakes because they handle ordinary decisions with discipline. That protects assets, reduces owner conflict, and gives the community a better chance of holding value over time.

If your board is wrestling with maintenance boundaries, reserve planning, insurance responsibilities, or mixed-property governance, Access Management Group can help you turn those questions into clear operating policies. The goal isn't more complexity. It's a community that's easier to govern, easier to explain to owners, and better protected over the long term.