The envelope arrives, or the email notice hits your inbox, and the reaction is usually the same. “What exactly am I paying for?” If the amount increased, the second question comes even faster.

That response is normal. Homeowners association assessments feel personal because they are personal. They affect your monthly budget, and they reflect decisions made by a board made up of your neighbors. But in a well-run community, assessments are not just bills. They are the funding mechanism that keeps the property maintained, the finances stable, and the community marketable.

A new board member needs to understand that quickly. A homeowner needs to understand it just as clearly. When people only see the payment, conflict grows. When they understand the purpose, the conversation changes.

Your Guide to Community Association Funding

If you're new to a community association, start with the big picture. Assessments are the shared contributions that pay for the work no single owner can handle alone. That includes common area maintenance, insurance, professional services, utilities, and long-term repair planning.

Community associations represent a significant portion of the housing market rather than a niche segment. According to the Foundation for Community Association Research's 2025 statistical review, there are 373,000 community associations in the United States with approximately 78.1 million residents, representing more than one-third of all U.S. housing at 35.2%. Homeowners association assessments are part of everyday homeownership for a very large share of the country.

Why the notice in your mailbox matters

When a homeowner receives an assessment notice, it helps to think of it as a stake in the condition of the whole property. Roads, roofs, pools, elevators, gates, landscaping, stormwater systems, and building exteriors don't maintain themselves. If the association doesn't collect enough money to care for them, the cost doesn't disappear. It gets delayed, and delay is usually more expensive.

Board members often make the mistake of treating assessments as a political problem first and a financial obligation second. That approach usually backfires. The better approach is to show owners how the money connects to real obligations and to long-term planning, especially through reserve fund planning for community associations.

Assessments work best when owners can see the link between what they pay today and the condition of the community tomorrow.

A healthier way to frame the conversation

For homeowners, the most useful mindset is this: you are not paying only for today's mowing, cleaning, or gate service. You're helping fund the stability of a shared asset.

For boards, the responsibility is just as important. Set assessments too low, and the community borrows from its future. Set them responsibly, explain them well, and you reduce surprises, protect property values, and lower the temperature around every budget season.

The Three Types of Homeowners Association Assessments

Not all assessments do the same job. A lot of homeowner frustration comes from hearing one word, “assessment,” used to describe three different financial tools.

The easiest way to understand them is to compare the association's finances to a household budget. You need money for monthly bills, money set aside for big planned replacements, and a way to handle a true surprise.

The three buckets

| Assessment Type | Purpose | Frequency |

|---|---|---|

| Regular Assessment | Pays ongoing operating expenses such as landscaping, insurance, utilities, and management | Recurring, usually monthly or another routine schedule set by the association |

| Reserve Contribution | Funds future major repair and replacement costs for common elements | Collected as part of the regular funding structure |

| Special Assessment | Covers unplanned or insufficiently funded expenses that can't be absorbed by the normal budget | Occasional and one-time or limited-duration |

Regular assessments

Regular assessments are the association's checking account money. These funds support day-to-day obligations and routine contract services. If the community has groundskeeping crews, pool service, cleaning vendors, security monitoring, insurance premiums, or management invoices, regular assessments are what keep those bills current.

For a board member, this is the baseline responsibility. If regular assessments are set too low for too long, every other funding problem gets harder.

Reserve contributions

Reserve contributions are the association's savings plan. They are not extra money. They are designated funds for major repair and replacement obligations that the community already knows are coming, even if the exact date is years away.

A roof ages. Asphalt wears down. Exterior surfaces deteriorate. Mechanical equipment reaches the end of its useful life. Smart boards treat reserve funding as a routine obligation, not a luxury.

Special assessments

Special assessments are the community's emergency response when regular operations and reserves aren't enough. Sometimes they arise because a major component failed earlier than expected. Sometimes the board underfunded reserves. Sometimes an external cost lands without warning.

One real example is insurance. A discussion of special assessments and insurance deductibles notes a growing shift toward percentage-based deductibles, and that a major hail event can create an unexpected six-figure deductible that homeowners must fund. At the same time, many owners carry only a standard $1,000 in personal loss assessment coverage. That's a harsh lesson when the board has to levy a special assessment with little lead time.

If you want a deeper look at when boards use this tool, review how special assessments work in community associations.

Practical rule: Regular assessments keep the lights on. Reserve contributions keep predictable projects from becoming crises. Special assessments fill the gap when planning or circumstances fall short.

What doesn't work is pretending all three are interchangeable. They aren't. Each serves a different purpose, and a board that communicates that distinction clearly will have fewer owner disputes.

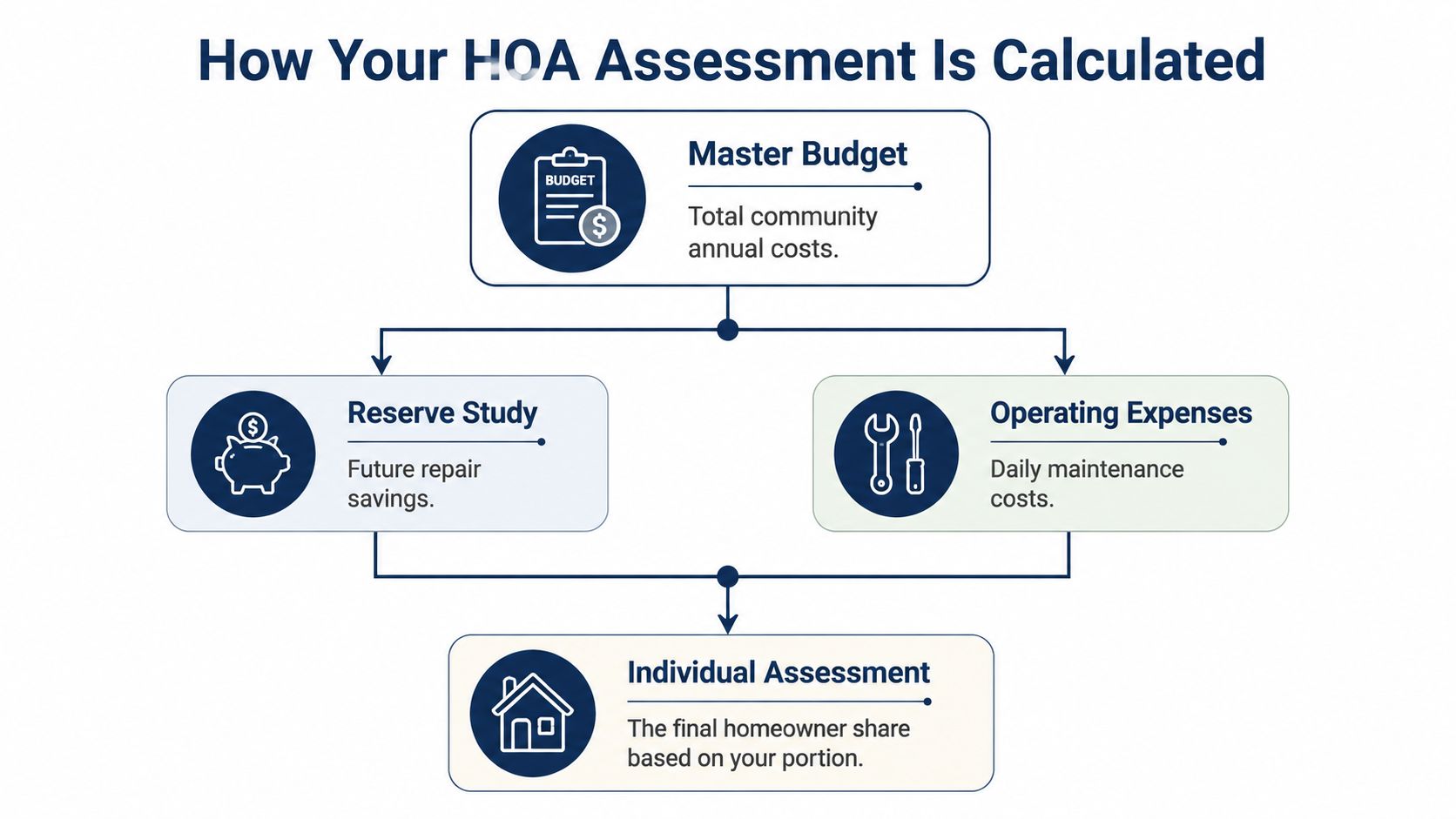

How Your HOA Assessment Is Calculated

A well-prepared assessment amount is not arbitrary. It comes from math, planning, and judgment. The board starts with the association's obligations, then allocates those costs across the ownership base according to the governing documents.

In practical terms, homeowners association assessments are built from two budgets working together. One covers current operations. The other prepares for future replacements. If either side is neglected, the numbers may look comfortable for a while, but the community becomes financially fragile.

In 2024, community associations collected $120.9 billion in member assessments, and that funding is calculated by dividing the total anticipated operational and reserve funding costs by the number of homes, as explained in DoorLoop's HOA statistics summary.

Step one is the operating budget

The operating budget covers current-year expenses. In most Georgia associations, that includes items like:

- Insurance premiums: Property and liability coverage often move faster than owners expect.

- Contract services: Landscaping, janitorial work, pool maintenance, gate service, pest control, and other vendors fall here.

- Utilities and administration: Water for common areas, power for lights and amenities, postage, software, legal, audit, and management support all belong in the operating side.

Boards need realism. A budget should reflect contracts, known increases, and recurring obligations. It should not rely on wishful thinking.

Step two is the reserve study

The second piece is reserve funding. Assessments are mathematically derived by dividing total anticipated operating and reserve needs by the number of lots or homes, but reserve contributions require more than simple arithmetic. They depend on a reserve study that looks at major components, estimated useful life, and projected replacement costs, as described in this guide to HOA collections and assessments.

That same guidance explains why a reserve study should be updated regularly. A reserve plan built years ago may no longer reflect current costs, current wear, or current priorities. A board that ignores that drift usually ends up underfunded.

A reserve study doesn't predict the future perfectly. It gives the board a disciplined way to prepare for costs that are certain to arrive, even if the exact timing changes.

Step three is allocation to each owner

Once the total budget is set, the governing documents determine how costs are assigned. In some communities, every lot pays the same amount. In others, the declaration uses formulas tied to unit type, size, or ownership percentage.

Homeowners often think the number should feel intuitive. It doesn't have to feel intuitive. It has to be consistent with the documents and sufficient for the budget.

Boards get into trouble when they reverse the process. They pick a politically comfortable assessment amount first, then try to squeeze the budget to fit. Sound budgeting works the other way around. Calculate the actual need first. Then communicate it plainly.

The Board's Duty to Collect Assessments

Boards sometimes hesitate to enforce collections because they don't want to seem aggressive. That's understandable, but it's also a mistake. The board has a duty to the entire membership, not only to the owners who are behind.

When one owner doesn't pay, everyone else effectively subsidizes that shortfall unless the board acts. Vendors still expect payment. Insurance carriers still expect premiums. The property still needs maintenance. If enough accounts slide, the board starts deferring work or draining cash needed elsewhere.

Why collections protect paying owners

A useful piece of industry research states that foreclosures are a "significant cause of underfunded HOA budgets" and that non-payment periods can stretch 90+ days, creating a cycle in which unpaid assessments force deferred maintenance and can lower property values for the whole community, according to this report on underfunded homeowners associations.

That is why collection policies matter. Not because boards enjoy enforcement. Because delay spreads the problem.

What a fair collection process looks like

A professional collection process is firm, documented, and consistent. It usually includes steps like these:

- Invoice and due date control: Owners receive clear billing statements and a clear due date.

- Courtesy reminder: Early outreach often resolves simple oversights.

- Late notice and charges allowed by the documents: Once the account is delinquent, the association applies its adopted policy.

- Escalation to legal remedies: If the balance remains unpaid, the board may authorize lien rights or other remedies available under governing documents and applicable law.

- Follow-through: Selective enforcement trains the community not to take deadlines seriously.

Boards should never improvise collections from owner to owner. That invites claims of unfairness and undermines credibility. A written policy, applied consistently, protects the association and gives owners predictable notice.

Collecting assessments is not about punishing a neighbor. It's about preventing the neighbors who do pay from carrying someone else's share.

What doesn't work

Three habits create most collection problems.

- Waiting too long: Early delinquencies are easier to resolve than old balances.

- Making private exceptions without a process: Compassion matters, but undocumented side deals create bigger disputes later.

- Treating collection as optional: Once owners believe the board won't act, delinquency usually spreads.

A board that collects promptly is not being harsh. It's protecting the community's finances with the same discipline owners expect in every other area of operations.

Your Rights and Options as a Homeowner

Homeowners have responsibilities, but they also have rights. If you receive an assessment notice and have questions, the best response is not to ignore it or argue in a parking lot. The best response is to use the association's formal channels.

That starts with records. Owners should review the budget, financial statements available under the governing documents and applicable law, and meeting minutes that reflect board decisions. Those records usually answer more questions than rumors ever will.

If you want to question a charge

Start in writing. Be specific. Identify the charge, the date, and the reason you think it may be incorrect. General complaints such as “my dues are too high” don't give the board or manager anything workable.

A stronger message looks more like this:

- Reference the account detail: Ask for the ledger entry or notice you are disputing.

- Point to the document issue: If you believe the charge conflicts with the declaration, bylaws, rules, or published fee schedule, say so directly.

- Ask for the process: Request the next step for review, hearing, or appeal if one is available.

That approach keeps the conversation productive. It also creates a record.

If you're facing hardship

The worst move is silence. If you know you can't pay on time, contact management or the board early and ask whether a payment arrangement is possible under the association's policy. Not every request can be approved, and boards must stay consistent, but early communication gives everyone more room to solve the problem.

Owners usually have more options before the account reaches legal enforcement than after it does.

If a payment plan is discussed, get the terms in writing. Verbal understandings cause confusion. Written terms help both sides track expectations and avoid later disputes about what was promised.

How homeowners help themselves most

Owners put themselves in the best position when they do four things well:

- Read notices promptly: Many avoidable problems start with unopened mail.

- Keep contact information current: If the association can't reach you, deadlines still keep moving.

- Use formal channels: Questions belong in writing, not in rumor chains.

- Stay engaged before budget season: It's easier to understand assessments when you've followed the decisions behind them.

A board should welcome informed questions. Homeowners should ask them in a way that invites answers instead of escalation.

Best Practices for Financially Sound HOA Boards

Strong boards don't wait for trouble to become obvious. They build habits that make bad surprises less likely and easier to manage when they do happen.

The first habit is transparency. Owners don't need every accounting detail every week, but they do need clear explanations of what the board is doing, why costs are changing, and what the consequences of delay would be. Silence creates suspicion faster than almost anything else in community management.

What good boards do consistently

A financially sound board usually gets these fundamentals right:

- Builds budgets from actual obligations: The board starts with contracts, insurance, maintenance needs, and reserve planning. It doesn't start with a target number designed to avoid complaints.

- Uses outside expertise where needed: Reserve professionals, accountants, attorneys, and managers all have a role. Boards should not guess their way through technical financial decisions.

- Communicates before owners are surprised: Pre-budget town halls, budget notes, and plain-English explanations lower resistance because people can follow the reasoning.

- Tracks delinquencies monthly: Collections are part of financial stewardship, not a side issue.

- Keeps records clean: Board decisions should be documented. Financial reports should be timely. Reconciliations should be routine.

For boards that want more structure on the financial side, accounting support for homeowners associations can include assessment invoicing, payment processing, and delinquency tracking. Access Management Group is one example of a management company that handles those functions within community association operations.

What weakens board credibility

Owners can usually accept difficult news if the board shows discipline. What they don't accept well is inconsistency.

Common failures include underfunding for years, avoiding reserve contributions because they are unpopular, approving increases without a clear explanation, and changing collection practices based on who is asking for leniency. Those choices may feel easier in the moment, but they erode trust.

Boards earn confidence when they explain the trade-offs honestly. “We can delay this” is not the same as “This cost goes away.”

The board president's role

The president doesn't need to be the community's accountant. The president does need to insist on process. That means asking whether the numbers are supportable, whether reserve planning is current, whether owners have been informed, and whether the board is enforcing policy consistently.

The most effective presidents I see are not the loudest people at the table. They are the ones who keep the board focused on long-term property health instead of short-term comfort.

Building a Financially Healthy Community Together

Homeowners association assessments are easy to dislike when they are viewed in isolation. They make more sense when you connect them to what they fund and what they prevent. They pay for current operations, prepare for major replacements, and keep financial stress from spilling into deferred maintenance, conflict, and surprise charges.

For homeowners, the practical takeaway is simple. Read the notices, review the records, ask better questions, and communicate early if there's a problem. That approach gives you more clarity and more options.

For board members, the standard is higher. Budget accurately. Fund reserves responsibly. Collect consistently. Explain decisions before frustration fills in the blanks. Communities do better when boards treat assessments as a stewardship issue instead of a popularity contest.

The healthiest associations are not the ones with the lowest fees on paper. They are the ones with enough discipline to maintain the property, plan ahead, and communicate in a way that homeowners can trust.

If your board needs help with assessment administration, financial processes, or day-to-day community operations, Access Management Group works with Georgia associations to support budgeting, collections, and community management in a structured, homeowner-focused way.